If a rolling 30d ATM IV is enough, there is a ton of data available out there MC, ORATS, ivolatility, quantcha, Quandl, Finpricing, yada yada.

HOWEVER!:

Data quality in options heavily erodes the less volume an individual chain has. At least I started using option book data and calculate the simple metrics from bid/ask midpoint for that reason.

Also the question is how the average is calculated and which maturities and deltas you want to be included. Do you want to have a VIX style calculation that includes the entire chain or do you want the 50 delta call?

In the long run it is always the best to set up your own database and collect bid/offer prices. Mongo DB and jupyter notebook is sufficient. For me all the cursing and "wasted time" was totally worth it.

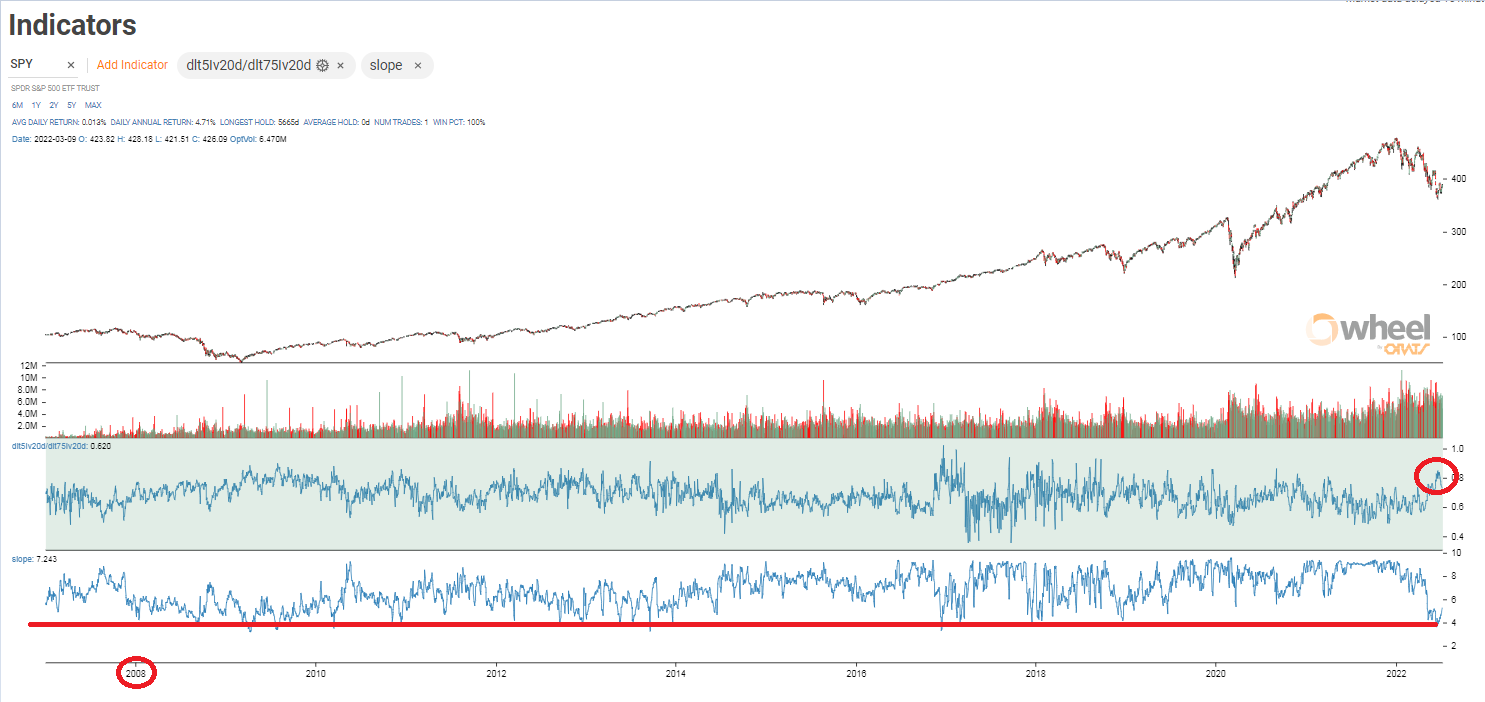

Good points. We work hard to utilize historical data, score bid-ask quality, and smooth the volatility surface in order to get quality constant maturity, constant delta IV readings.

https://docs.orats.io/datav2-api-guide/core-research.html#the-smile

Below are a smattering of SMV Summary data definitions.

Field Definition

ticker underlying symbol

annActDiv annual dividend from the next year of expected dividends

annIdiv annual implied dividend given options prices put call parity

borrow30 implied hard-to-borrow interest rate at 30 days to expiration given options prices put call parity

borrow2y implied hard-to-borrow interest rate at two years to expiration given options prices put call parity

confidence total weighted confidence from the monthly implied volatilities derived from each month’s number of options and bid ask width of the options markets

exErnIv10d implied 10 calendar day interpolated implied volatility with earnings effect out

exErnIv20d implied 20 calendar day interpolated implied volatility with earnings effect out

exErnIv30d implied 30 calendar day interpolated implied volatility with earnings effect out

exErnIv60d implied 60 calendar day interpolated implied volatility with earnings effect out

exErnIv90d implied 90 calendar day interpolated implied volatility with earnings effect out

exErnIv6m implied 6 month interpolated implied volatility with earnings effect out

exErnIv1y implied one year interpolated implied volatility with earnings effect out

ieeEarnEffect implied earnings effect (percentage of expected normal move) to make the best-fit term structure of the month implied volatilities

impliedMove percentage stock move in the implied earnings effect to make the best-fit term structure of the month implied volatilities

impliedNextDiv next implied dividend given options prices put call parity

iv10d 10 calendar day interpolated implied volatility

iv20d 20 calendar day interpolated implied volatility

iv30d 30 calendar day interpolated implied volatility

iv60d 60 calendar day interpolated implied volatility

iv90d 90 calendar day interpolated implied volatility

iv6m 6 month interpolated implied volatility

iv1y one year interpolated implied volatility

mwAdj30 ATM weighted market width in implied volatility terms interpolated to 30 calendar days to expiration

mwAdj2y ATM weighted market width in implied volatility terms interpolated to 2 years to expiration

nextDiv next dividend amount

rDrv30 derivative or curvature of the monthly strikes at 30 day interpolated. The derivative is the change in the slope for every 10 delta increase in the call delta

rDrv2y derivative infinite implied

rSlp30 best-fit regression line through the strike volatilities adjusted to the tangent slope at the 50 delta. The slope is the change in the implied volatility for every 10 delta increase in the call delta

rSlp2y implied infinite slope

rVol30 implied volatility at 30 days interpolated

rVol2y implied volatility at 2 year interpolated

rip dollar amount of options to start ignoring in delta calculation

riskFree30 continuous interest (risk-free) rate interpolated to 30 calendar days to expiration

riskFree2y continuous interest (risk-free) rate interpolated to 2 years to expiration

skewing Skewing is the difference between rVol30 and adjusted rVol2y where sqrtMinDays is 45 * 0.5. ((rVol30 - rVol2y * (1 - 1/sqrtMinDays)) * sqrtMinDays)

contango short-term contango of at-the-money implied volatilities ex-earnings

totalErrorConf total weighted squared error times the confidence in the monthly implied volatility

dlt5Iv10d 10 calendar day interpolated implied volatility at the 5 delta

dlt5Iv20d 20 calendar day interpolated implied volatility at the 5 delta

dlt5Iv30d 30 calendar day interpolated implied volatility at the 5 delta

dlt5Iv60d 60 calendar day interpolated implied volatility at the 5 delta

dlt5Iv90d 90 calendar day interpolated implied volatility at the 5 delta

dlt5Iv6m 180 calendar day interpolated implied volatility at the 5 delta

dlt5Iv1y 365 calendar day interpolated implied volatility at the 5 delta

exErnDlt5Iv10d 10 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

exErnDlt5Iv20d 20 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

exErnDlt5Iv30d 30 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

exErnDlt5Iv60d 60 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

exErnDlt5Iv90d 90 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

exErnDlt5Iv6m 180 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

exErnDlt5Iv1y 365 calendar day interpolated implied volatility at the 5 delta with earnings effects removed

dlt25Iv10d 10 calendar day interpolated implied volatility at the 25 delta

dlt25Iv20d 20 calendar day interpolated implied volatility at the 25 delta

dlt25Iv30d 30 calendar day interpolated implied volatility at the 25 delta

dlt25Iv60d 60 calendar day interpolated implied volatility at the 25 delta

dlt25Iv90d 90 calendar day interpolated implied volatility at the 25 delta

dlt25Iv6m 180 calendar day interpolated implied volatility at the 25 delta

dlt25Iv1y 365 calendar day interpolated implied volatility at the 25 delta

exErnDlt25Iv10d 10 calendar day interpolated implied volatility at the 25 delta with earnings effects removed

exErnDlt25Iv20d 20 calendar day interpolated implied volatility at the 25 delta with earnings effects removed...