Quote from lurefo:It seems we pretty much agree on all that layering/quote stuffing thingy. Although until I'm proven otherwise I still think quote stuffing is a serious threat to the market stucture as shown by the nanex guys.

Iâm not sure I follow. Layering is bad I agree but the way you say âall that layering/quote stuffing thingyâ seems like you are still lumping them both in together and donât understand the difference. I donât think Quote Stuffing is a legit complaint â I think itâs just a complaint made up by people with outdated or inferior hardware who canât handle true market data feeds. Furthermore I think that Quote Stuffing is next to impossible to prove and that itâs a very slippery slope in terms of regulating who can place orders, how many orders and what types of orders. As I said earlier, Quote Stuffing is described similarly to a DOS Attack and therefore I agree that in concept it is a serious threat to the market â only in that it is vulnerable.

I personally think the âNanex guysâ love all the attention they are getting from uninformed market watchers/participants. After all, they do sell market data feeds. The pretty pictures they put out are interesting to look at but donât really show anything other than the dayâs historical price action. Iâm going to call Nanex today and Iâve requested a trial/demo of their product via email. Iâd love to be proven wrong but they flat out admit on their website that they introduce latency into their data feeds at the origination and destination points. Iâve said all along that they have a bias against HFT and ultra-low latency and now its much more clear. Their product INTRODUCES latency therefore it has no traction (IMHO introducing latency has no business being in the markets at all). By hating on the low-latency players in the market they can distract the uninformed into thinking that their âcompressedâ data feed is an OK product because you get everything the big boys get in a smaller package blah blah blah⦠Only problem is that by introducing latency to compress/decompress the data they are essentially selling you HISTORICAL data and passing it off as real-time market data. To me, thatâs fraud, but Iâll wait and talk to them before I start alleging things like that.

Quote from lurefo: I would have to read the articles again to see if they mentioned which stock was quote stuffed 5000/s

Iâll make a point to ask. They have not responded to my emails (and I donât expect them to) but Iâd imagine that based on their apparent bias and the products they offer â they probably cherry picked for marketing purposes and donât want to disclose that because it will further discredit them. (again just a hunch/opinion)

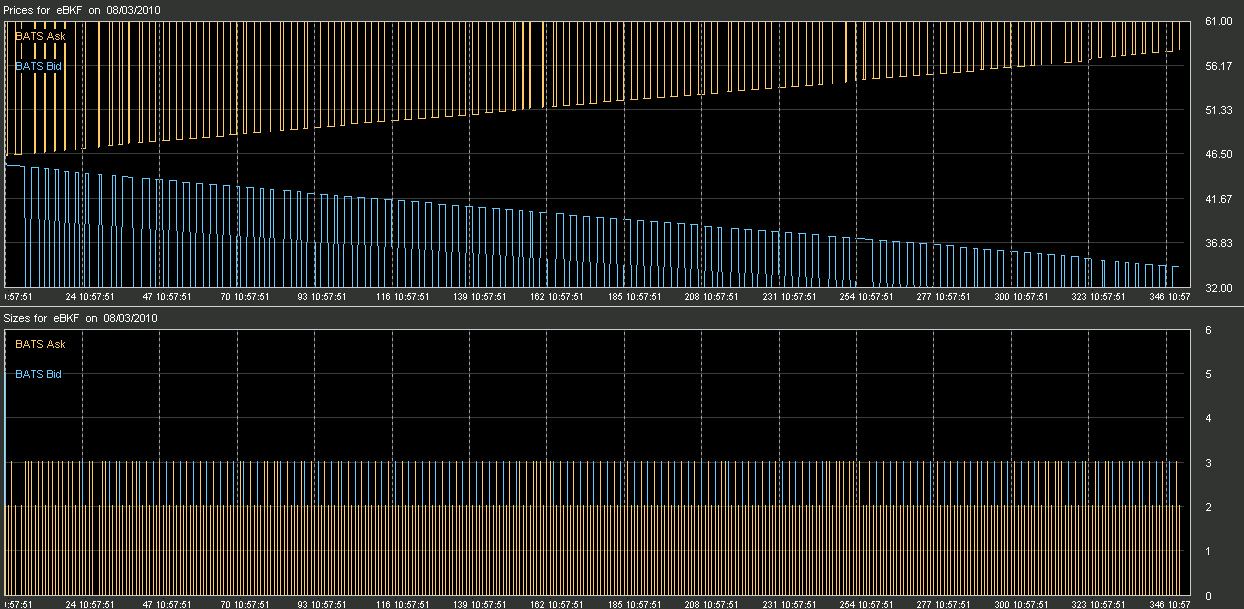

Quote from lurefo:but have a look at this page where they collect on a daily basis evidences of quote stuffing algos in different stocks stocks:http://www.nanex.net/FlashCrash/CCircleDay.html

These pages have been all over the internet since some clown at Zero Hedge misinterpreted them and posted them on a blog. Again, all those pretty pictures show is historical tick data, charted to look pretty. They use straight/jagged lines and right angles to make it seem like someone is manipulating the markets, etc. when in actuality itâs just traders doing what they have always done. One of the programmers I work with did the same thing for the historical data in the S&P pit 15 years ago and he made it look worse â and that was well before the times of HFT and all manual/voice trading. Also, those pretty pictures donât demonstrate Quote Stuffing or Layering, they may show someone walking up/down the price of a stock but there is nothing provided to show any type of Quote Stuffing or Layering.

Quote from lurefo: Anoter flash crash is the last thing we want, right?

It canât really be avoided â Telling a market participant that they have to be in/stay in the markets is just as bad/dangerous as telling someone that they canât be in the market or canât place orders (reference to Quote Stuffing). If you were to tell MMs and Liquidity providers that they are not legally allowed to step away when the market plummets then they would just introduce wider spreads as âinsuranceâ against something happening again. All that does is hurt the little guy. You cannot tell a market participant when they can be in/out of the markets, it is solely their choice and should never be regulated. (but yes, itâs a bad thing and no one needs another day like that)

Quote from lurefo:edit : not sure what you mean by By adding time stamps you are going to be sending quotes out of order due to latency issues, etc. AND the quote messages will now contain MORE data. I thought the order was times stamped at the time it is disseminated and the recommendation was to time stamp it as it enters the queue... so how could that change the size of the message? thanks for clarifying what you meant.

Iâm going to be honest and say that I donât fully understand exactly where timestamps are assigned to events, nor do I know if there is an exchange-wide standard, or of exchanges can assign timestamps wherever they want and however best suits them. Iâm going to take my best shot at it but know that this is just how I understand it so if someone knows better please correct me or fill in the blanks.

There are two parts to quote/data delivery: Execution/Matching Engine and the Data/Quote Dissemination Engine/Server. An order hits the execution/matching engine, is processed and then sent to the data/quote dissemination engine/server where it is then forwarded to all subscribers of that exchange. Most of the top exchanges are in the nanosecond space so assume for the time being that there is zero latency between the matching engines and the dissemination servers â for all I know some exchanges might have one computer doing both tasks which truly would put the latency at zero.

What I do know is that due to latency, outside prints, errors, bad trades, busted trades, market makers/specialists adding executions late â or backdating a trade to âaboutâ when it happened, etc. the matching engines donât always send data to the quote dissemination engines in the exact order that they happened. Since the data coming out of the matching engine is not in the exact order that it happened, I donât know if the matching engines assign CORRECT timestamps to the data (meaning that as the dissemination servers receive the data the timestamps are out of order) or if the dissemination servers receive raw non-time stamped data and apply INCORRECT times to the quotes because the quote dissemination server would be applying sequential timestamps to the data as it receives it â except the data is out of order.

If I understand it correctly, I think that the matching engines apply the correct timestamp to the data as it sends over to the quote dissemination servers. This means that the quote dissemination servers are receiving the CORRECT data with the CORRECT timestamps â just out of order. I think that this is the bone of contention that people are bitching about⦠the data is out of order, therefore its bad, if timestamps arenât in correct order then how can we parse the data, blah blah⦠(I pay for raw market data and âscrubbedâ historical data where things are put into order for me after the fact so my back tests are more accurate, so I donât really know and it does not affect me.) I *think* that what people want is to have the quote dissemination servers timestamp the data as it receives it, giving the market participants a more âtrue pictureâ of the data flow and when it actually happens. If I understand all of this correctly, my gripe with time stamps at the quote servers is that they will be incorrectly time stamping the trades. Even though the quote servers would be time stamping as they receive the data, it is known that the data is out of order, therefore, in my opinion, the argument for quote servers applying timestamps is also an argument for degradation of data. With regards to the size of the message, I assume that somewhere in there they will need to add a tracer as to when the print actually occurred vs. when it was disseminated. I could be all wrong about this â but thatâs how I understand it.

Quote from stock777:I don't accuse you of being hft, I accuse you of trying to justify every possible manipulation as a shill.

LOL well when you say things like âheâs one of themâ it doesnât seem like it. Accuse me of whatever you want â Iâll keep accusing you of being an ignorant troll and not understanding the markets enough to comment in your own thread.