Lets say someone is worth $100,000 and its July 2008. This person thinks global stock markets are getting quite cheap and wants to invest all of those assets in a global stock market ETF. After investing, markets fell apart and went even lower.

Thing is, that person also happens to own a car worth about $35,000. Then the person decides 'why don't I sell this car that I don't even use much and buy more global stock markets? This stock market selling is getting out of hand'. But he/she doesn't want to just liquidate the car fast and not get full value for it, the person wants to be resonably patient. At the same time, the person doesn't want to miss the current prices that the stock markets are trading at. They might bounce back at anytime. A decent solution is to buy more stocks using futures or margin leverage (up to $35,000) and when the car is finally sold (say 1 or 2 months later) use those proceeds to deleverage (repay the margin loan or to use it to provide more collateral against the futures position)

Pretty simple case of someone doing responsible/smart leverage. You have your cake and eat it took in both sides of the equation, with tiny risks given that the leverage ratio is very much under control

Now why cant this be extended to savings arising from salary income? Lets say someone has a quite stable job (say a doctor/dentist/psychologist with a large client base in a major city), why can't this person count on the next 12-24 month worth of savings as part of future proceeds that can be used to repay margin loans or to collaterize leveraged futures positions? If such logic is applied, that person can run a modestly leveraged growth portfolio and still be fine since those salary savings are in effect 'delevering' the portfolio as they come in

Another case of smart leverage. Can that be misapplied? Yes but so can just about any investment/trading concept.

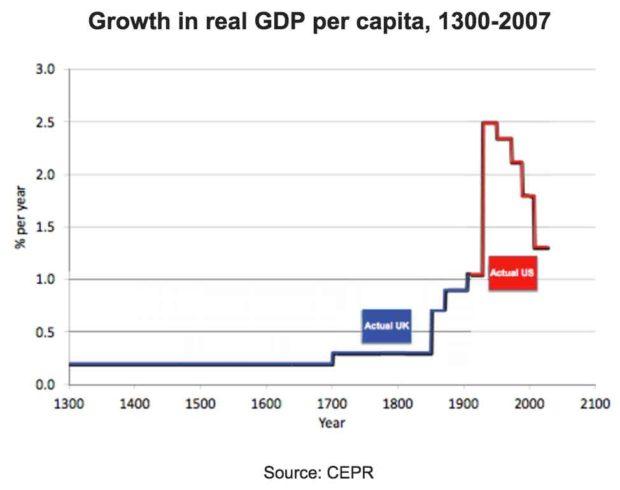

Reason why I bring this up is two fold. First is this chart I posted a while back

So real per capita GDP has had a giant secular rise that was unlike the world has ever seen, I do no think its a suprise to see the world being deep into debt (Both governments and private debts). I suspect its a similar logic to the 2 examples I gave, people are using future income/wealth as a form of 'reason' to lever up. There is future real income gains, future savings, future capital gains from home prices, stocks, etc, all giving 'reasons' for people to borrow . Usually they do it with consumption intead of investments, which brings less benefits in terms of expected value but it might bring better quality of life today.

I'm not saying that it is smart leverage like those previous examples, this could be smart, it could be dumb, the jury is out on this one. It will depend on how sustainable the progress arising from technological discoveries is. Since the industrial revolutions, new technologies have produced gigantic economic gains. People saw that and leveraged up because they felt confident it was safe. I don't think this leverage has much to do with central banks/bubbles or Austrian theories or anything like that. You can't force people to do things, they will only do if they want to. People decided that with rising incomes and rising asset prices it was ok to increase leverage. And this whole thing created a self reinforcing cycle

One day this could all go bad but this whole thing (the antecipation of future money) helps explain what is going on

And the second reason is, if there are some simple smart ways to employ leverage conservatively (like those 2 examples) and boost returns, how many other ways is there that most people haven't thought about because they are not trying to?

Leverage gets a bad rap as a result people don't think about it but I bet brainstorming safe leverage methods can lead to some interesting discoveries

Thing is, that person also happens to own a car worth about $35,000. Then the person decides 'why don't I sell this car that I don't even use much and buy more global stock markets? This stock market selling is getting out of hand'. But he/she doesn't want to just liquidate the car fast and not get full value for it, the person wants to be resonably patient. At the same time, the person doesn't want to miss the current prices that the stock markets are trading at. They might bounce back at anytime. A decent solution is to buy more stocks using futures or margin leverage (up to $35,000) and when the car is finally sold (say 1 or 2 months later) use those proceeds to deleverage (repay the margin loan or to use it to provide more collateral against the futures position)

Pretty simple case of someone doing responsible/smart leverage. You have your cake and eat it took in both sides of the equation, with tiny risks given that the leverage ratio is very much under control

Now why cant this be extended to savings arising from salary income? Lets say someone has a quite stable job (say a doctor/dentist/psychologist with a large client base in a major city), why can't this person count on the next 12-24 month worth of savings as part of future proceeds that can be used to repay margin loans or to collaterize leveraged futures positions? If such logic is applied, that person can run a modestly leveraged growth portfolio and still be fine since those salary savings are in effect 'delevering' the portfolio as they come in

Another case of smart leverage. Can that be misapplied? Yes but so can just about any investment/trading concept.

Reason why I bring this up is two fold. First is this chart I posted a while back

So real per capita GDP has had a giant secular rise that was unlike the world has ever seen, I do no think its a suprise to see the world being deep into debt (Both governments and private debts). I suspect its a similar logic to the 2 examples I gave, people are using future income/wealth as a form of 'reason' to lever up. There is future real income gains, future savings, future capital gains from home prices, stocks, etc, all giving 'reasons' for people to borrow . Usually they do it with consumption intead of investments, which brings less benefits in terms of expected value but it might bring better quality of life today.

I'm not saying that it is smart leverage like those previous examples, this could be smart, it could be dumb, the jury is out on this one. It will depend on how sustainable the progress arising from technological discoveries is. Since the industrial revolutions, new technologies have produced gigantic economic gains. People saw that and leveraged up because they felt confident it was safe. I don't think this leverage has much to do with central banks/bubbles or Austrian theories or anything like that. You can't force people to do things, they will only do if they want to. People decided that with rising incomes and rising asset prices it was ok to increase leverage. And this whole thing created a self reinforcing cycle

One day this could all go bad but this whole thing (the antecipation of future money) helps explain what is going on

And the second reason is, if there are some simple smart ways to employ leverage conservatively (like those 2 examples) and boost returns, how many other ways is there that most people haven't thought about because they are not trying to?

Leverage gets a bad rap as a result people don't think about it but I bet brainstorming safe leverage methods can lead to some interesting discoveries