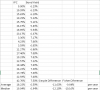

Sidney Homer and Richard Silla in their great book 'A History of Interest Rates' have data on old Brazilian government bonds that existed in the last century. I collected that yield data and put it over the inflation data that I have to see how investors might have fared

The book does not say what were the maturity of the bonds so I cannot estimate returns based on changes on yields. I can, however, average out yields and compare to average inflation. I then subtracted the avg yield from the avg inflation (and called it Simple Difference), I also applied the Fisher Equation to see if there was any big difference (and called it Fisher Diference)

Quotations from the bonds stopped after 1959 and the government stared to index bonds and other fixed income instruments to inflation (presumably because the market had enough of inflation and wasn't going to invest in sucker bonds anymore)

Its quite clear the this Brazilian bond market blew up in the 50's and investors were severely eroded by inflation

The book also talks about the Argentina and Chile experience. In Chile, between 1945 and 1960, the currency lost 95% of its dollar value and the cost of living index rose by 50x. The comes out to a 27.7% compounded inflation rate. Chile bond yields averaged 8.48% in the 40's and 8.33% from 1950 to 1953. On 1953 the bond yield data stops. So, another bond market likely blew up

In Argentina, the currency lost 94% of its dollar value in the 50's. The average yield in the 40's was 3.94% and in the 50's (up to 1953 when the series stopped) the avg yield was 3.26%. So, safe to say, another bond market blew up

In Uruguay, Mexico, Pery and Colombia, they provide yield data but provide no inflation so its hard to estimate bond returns, although it appears that Colombia did well.

Still, with 3 countries out 7 delivering huge real losses to bond holders, its safe to say that duration bonds (bonds with significant maturities) in latin america, historically have been quite risky. It looks very likely that they have produced negative real returns and are a value destroying asset classes. This does not apply to the fixed income asset class as a whole. Certain savings accounts, inflation indexed bonds and other products have proven more resilient to inflation in Brazil than longer maturities bonds (but even them had some pretty awful years, plus the price index was manipulated down). But duration quite clearly is a very risky value destroying 'asset class' in Latin America