I have to say that I am enjoying the witty repartee almost as much, if not more...

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Global Macro Trading Journal

- Thread starter Daal

- Start date

I'm buying Sep 2012 FSIN 2.5 put options. MWR has made a strong case the company is a total fraud and will get delisted like RINO(Now trading at 6c on the PinkSheets)

http://vimeo.com/40098291

Stock is a $6. If it goes to $0 I make more than 10x my money. But it won't go to $0 so fast. I might exercise my options at $1 or so. I bought them for 20c, so I make 6.5 times my money if my math is correct

Seems pretty clear case of positive expectation trade to make. What these options MMrs are doing is beyond me

http://vimeo.com/40098291

Stock is a $6. If it goes to $0 I make more than 10x my money. But it won't go to $0 so fast. I might exercise my options at $1 or so. I bought them for 20c, so I make 6.5 times my money if my math is correct

Seems pretty clear case of positive expectation trade to make. What these options MMrs are doing is beyond me

Kashkari on profits

http://www.pimco.com/EN/Insights/Pages/Equity-Focus-Newtonian-Profits-April-2012.aspx

I disagree with him in the likelihood of a recession, I believe its higher than he thinks, plus if it happens it will be combined with USD strength as risk aversion takes place. This would hit profits quite hard

But he DOES make a good point with regards to profits and government deficits. Since profits are strongly linked to NGDP, a fall in government deficits might decrease margins but not nominal profits. S&P500 nominal profits would keep increasing even though as a % of GDP they would decline

This seems a possibility given that the Fed seems to have a pseudo 3-5% NGDP target that they try to achieve in the absence of large shocks(When there are large shocks they mess it up and let it go negative like in 2008)

The fact that PE ratios are "low" might be just a reflection that the market knows the rate of growth in profits is slowing(I posted a chart a while back) and therefore the premium to be put in stocks should be smaller

Anyone can calculate this themselves using a modified Dividend Growth Model(I did this a few months ago in this journal). Or just use common sense, if the underlying income stream grows less, you pay a smaller multiple for it

http://www.pimco.com/EN/Insights/Pages/Equity-Focus-Newtonian-Profits-April-2012.aspx

I disagree with him in the likelihood of a recession, I believe its higher than he thinks, plus if it happens it will be combined with USD strength as risk aversion takes place. This would hit profits quite hard

But he DOES make a good point with regards to profits and government deficits. Since profits are strongly linked to NGDP, a fall in government deficits might decrease margins but not nominal profits. S&P500 nominal profits would keep increasing even though as a % of GDP they would decline

This seems a possibility given that the Fed seems to have a pseudo 3-5% NGDP target that they try to achieve in the absence of large shocks(When there are large shocks they mess it up and let it go negative like in 2008)

The fact that PE ratios are "low" might be just a reflection that the market knows the rate of growth in profits is slowing(I posted a chart a while back) and therefore the premium to be put in stocks should be smaller

Anyone can calculate this themselves using a modified Dividend Growth Model(I did this a few months ago in this journal). Or just use common sense, if the underlying income stream grows less, you pay a smaller multiple for it

In order for profits to keep growing AND margins to contract, if I'm looking at this correctly, profits will have to grow a bit less than NGDP. Perhaps at a 1-3% clip a year(With NGDP at 3-5%)

So I would highly disagree with that people who call this market 'cheap', due low price to trailing earnings ratios. This is simply a rational way to price an asset that is growing less

Of course, that growth % assumes no recession or significant impact from Fiscal austerity.

The S&P500 seems to be fairly valued IF everything goes fine, if it doesn't, then its overvalued

So I would highly disagree with that people who call this market 'cheap', due low price to trailing earnings ratios. This is simply a rational way to price an asset that is growing less

Of course, that growth % assumes no recession or significant impact from Fiscal austerity.

The S&P500 seems to be fairly valued IF everything goes fine, if it doesn't, then its overvalued

Perhaps I should have built a small position on Fed futures back when they were crashing

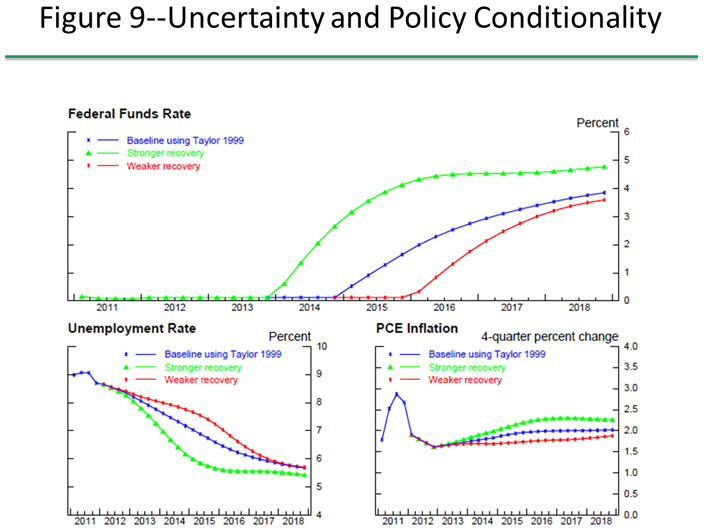

http://federalreserve.gov/newsevents/speech/yellen20120411a.htm#f17

This Taylor 99 model seem to be a decent guide to what the doves at the FOMC would do. Under the 'strong recovery' they would raise rates in late 2013, the contracts were predicting that but I would have a free shot at the Baseline scenario and weaker recovery scenario.

I still maintain that the edge was not huge though, under a stronger recovery its possible the total hikes would be more than 25bps by the time of settlement or even worse, the market would think that(as the Fed removes the forward guidance from the statement and people panic), giving me a huge capital loss in the meantime and totally complicating the trading of the contracts while trying to maintain adequate risk control

Anyway, its not all over yet. Under the baseline and weaker recovery the current pricing in the contracts is incorrect

http://federalreserve.gov/newsevents/speech/yellen20120411a.htm#f17

This Taylor 99 model seem to be a decent guide to what the doves at the FOMC would do. Under the 'strong recovery' they would raise rates in late 2013, the contracts were predicting that but I would have a free shot at the Baseline scenario and weaker recovery scenario.

I still maintain that the edge was not huge though, under a stronger recovery its possible the total hikes would be more than 25bps by the time of settlement or even worse, the market would think that(as the Fed removes the forward guidance from the statement and people panic), giving me a huge capital loss in the meantime and totally complicating the trading of the contracts while trying to maintain adequate risk control

Anyway, its not all over yet. Under the baseline and weaker recovery the current pricing in the contracts is incorrect

David Rosenberg on corporate profits -- something of a permabear whose lack of respect for price action has cost his followers a fortune, but still makes some solid points:

~~~

Second, there is the U.S. economy -- not just the disappointing jobs data on Friday but the reality that 70% of the releases in the past month have come in below expectations. While the chain stores did report what seemed on the surface to be a solid +3.9% YoY sales gain in March, keep in mind that yet again we had very mild weather and we also had an early Easter effect.

Third, there is the rapid slowing in corporate earnings. In Q4, we had the YoY trend in S&P 500 operating earnings slip into single-digits (+9.2%) for the first time in two years, and absent Apple, the pace would have been 6.2% (see the front page of the Investor's Business Daily). Only 62% of companies beat their estimates, which is far below average. As for Q1, the consensus is all the way down to +3.2% on a YoY basis -- well off the +5.5% expectation at the turn of the year and the +12.8% forecast in the mid-part of 2011. Strip Apple out of the numbers, and you are talking about earnings growth of practically nothing -- +1.8%.

Not only has earnings growth basically evaporated, but the ratio of negative to positive guidance has risen to levels we last saw two years ago, margins are poised to shrink to a two-year low as well, and only three S&P 500 sectors are actually seen raising their earnings from year-ago levels. Now the question is whether or not the market can move up with earnings contracting and the answer is -- of course! We have seen that in the past, as rare as it may be. Just go back to 1998, when the Asian meltdown and strong U.S. dollar severely pinched U.S. corporate earnings, yet the S&P 500 rallied more than 20% that year. But what else happened? Well, we had the Fed cut rates three times as a super-strong antidote, and did so at a time when there was no evident slack in the labor market. Plus, we were in the early stages of an internet-led productivity spree, which underpinned profit margins. In addition, we had a Democratic president working with Congress to pass legislation that reduced red tape, labour rigidities and taxation -- with no budget deficit! Please, tell me if we currently have these as antidotes for a weakening trend in corporate profits.

~~~

Second, there is the U.S. economy -- not just the disappointing jobs data on Friday but the reality that 70% of the releases in the past month have come in below expectations. While the chain stores did report what seemed on the surface to be a solid +3.9% YoY sales gain in March, keep in mind that yet again we had very mild weather and we also had an early Easter effect.

Third, there is the rapid slowing in corporate earnings. In Q4, we had the YoY trend in S&P 500 operating earnings slip into single-digits (+9.2%) for the first time in two years, and absent Apple, the pace would have been 6.2% (see the front page of the Investor's Business Daily). Only 62% of companies beat their estimates, which is far below average. As for Q1, the consensus is all the way down to +3.2% on a YoY basis -- well off the +5.5% expectation at the turn of the year and the +12.8% forecast in the mid-part of 2011. Strip Apple out of the numbers, and you are talking about earnings growth of practically nothing -- +1.8%.

Not only has earnings growth basically evaporated, but the ratio of negative to positive guidance has risen to levels we last saw two years ago, margins are poised to shrink to a two-year low as well, and only three S&P 500 sectors are actually seen raising their earnings from year-ago levels. Now the question is whether or not the market can move up with earnings contracting and the answer is -- of course! We have seen that in the past, as rare as it may be. Just go back to 1998, when the Asian meltdown and strong U.S. dollar severely pinched U.S. corporate earnings, yet the S&P 500 rallied more than 20% that year. But what else happened? Well, we had the Fed cut rates three times as a super-strong antidote, and did so at a time when there was no evident slack in the labor market. Plus, we were in the early stages of an internet-led productivity spree, which underpinned profit margins. In addition, we had a Democratic president working with Congress to pass legislation that reduced red tape, labour rigidities and taxation -- with no budget deficit! Please, tell me if we currently have these as antidotes for a weakening trend in corporate profits.

I have to wonder if the fact that under the baseline scenario and weaker recovery scenario the pricing of Fed futures is incorrect, if that is not the old 'hike fear' edge creeping back on the Fed futures contract that I took advantage over the last few years.

Economic consensus is bullish but not THAT bullish, yet the contracts trade as if hikes could happen soon.

If its the old edge creeping back in I will have no problem taking positions there and being aggressive(Cuz I know how nuts these expectations usually are). But if its more rational I will have to be careful

Economic consensus is bullish but not THAT bullish, yet the contracts trade as if hikes could happen soon.

If its the old edge creeping back in I will have no problem taking positions there and being aggressive(Cuz I know how nuts these expectations usually are). But if its more rational I will have to be careful