Kind of a 2020 Covid play, like ELY was in 2020.Stoney I won the bet.

Driveshack hit $2.99 today.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

GBA's "2021 Stock Phantasma"

- Thread starter stonedinvestor

- Start date

Why?sitting on a volcano here

Affirm Holdings, Inc. (AFRM)

NasdaqGS - NasdaqGS Real Time Price. Currency in USD

69.60+0.93 (+1.35%)

As of 3:09PM EDT. Market open.

Why is it near an all-time low when the indexes are all bouncing off time highs?

People read this thread Stoney.

Newbies.

They'll look at this, and then look at that chart and say "wow, it was $150 a month ago, it must be a buy".

I have not dug into this stock, but from experience my instincts tell me this dog has fleas.

There's a reason why it's trading where its at.

What do they do Stoney? Explain it to me without a cut and paste, in a sentence or two, and make a case as to why it's a buy.

I mean with all due respect, we don't need a blurb from MF or SA.

Those writers are easily in the circle of 'friends of a friend', the one that needs a favor and who's buried in a pos stock.

The financial media on the net is dominated by a select few players. The power these yoyo's yield is amazing. They can move a stock's price.

Not sayin' that's the case.... but I'm not sayin' it's not either.

Let's see some real DD Stoney.

Do not encourage readers to catch a falling knife based on cut&pastes and a low stock price.

-VZ

Last edited:

Opposite of the chart I love, was totally confused about this pick.Why?

Why is it near an all-time low when the indexes are all bouncing off time highs?

People read this thread Stoney.

Newbies.

They'll look at this, and then look at that chart and say "wow, it was $150 a month ago, it must be a buy".

I have not dug into this stock, but from experience my instincts tell me this dog has fleas.

There's a reason why it's trading where its at.

What do they do Stoney? Explain it to me without a cut and paste in a sentence or two, and make a case as to why it's a buy.

I mean with all due respect, we don't need a blurb from MF or SA.

Those writers are easily in the circle of 'friends of a friend' who needs a favor and who's buried in a pos stock.

The financial media on the net is dominated by a select few players. The power these yoyo's yield is amazing. They can move a stock's price.

Not sayin' that's the case.... but I'm not sayin' it's not either.

Let's see some real DD Stoney. Do not encourage readers to catch a falling knife based on cut&pastes and a low stock price.

-VZ

On Twitter is someone who use to be good at Biotech. Now everything he posts just craters. I saw how manipulative SA “Guest Contributed” in three small stocks. DD must be sharp or we lose credibility.Why?

Why is it near an all-time low when the indexes are all bouncing off time highs?

People read this thread Stoney.

Newbies.

They'll look at this, and then look at that chart and say "wow, it was $150 a month ago, it must be a buy".

I have not dug into this stock, but from experience my instincts tell me this dog has fleas.

There's a reason why it's trading where its at.

What do they do Stoney? Explain it to me without a cut and paste in a sentence or two, and make a case as to why it's a buy.

I mean with all due respect, we don't need a blurb from MF or SA.

Those writers are easily in the circle of 'friends of a friend', the one that needs a favor and who's buried in a pos stock.

The financial media on the net is dominated by a select few players. The power these yoyo's yield is amazing. They can move a stock's price.

Not sayin' that's the case.... but I'm not sayin' it's not either.

Let's see some real DD Stoney. Do not encourage readers to catch a falling knife based on cut&pastes and a low stock price.

-VZ

Not all stocks are break outs some are stocks that bottom from a correction. i have spotted a stock I think has bottomed from a correction that's why it has a higher print.

When looking for stocks that are bottoming you look for different clues..

Had You read carefully Van you would of learned the reasons.

- It started with the European stk I told you about that is the No 1 Fintech stk in all of Europe. private. They do.. Ta Da What AfRM does! <---

- Trends. I always am a trend user/follower and analyzer-- In Credit cards and auto pay now the younger generation is gravitating towards buy now pay later.

" Buy Now Pay later " remember that phrase.

- Stock lock up periods can work to to your advantage if you are nimble.

- You and Ted would do well to remember Buy Now part and you can pay me later.- Si

When looking for stocks that are bottoming you look for different clues..

Had You read carefully Van you would of learned the reasons.

- It started with the European stk I told you about that is the No 1 Fintech stk in all of Europe. private. They do.. Ta Da What AfRM does! <---

- Trends. I always am a trend user/follower and analyzer-- In Credit cards and auto pay now the younger generation is gravitating towards buy now pay later.

" Buy Now Pay later " remember that phrase.

- Stock lock up periods can work to to your advantage if you are nimble.

- You and Ted would do well to remember Buy Now part and you can pay me later.- Si

As well the company had 3 negative reports from analysts like this one--

BofA says don't buy Affirm Holdings stock yet!

I like that especially when Barons went the other way and said it was a very good idea.

- Another aspct I like of the co is they tend to be used for big ticket items! That's the kind we like to pay later for!

- Another aspect is the fact that Affirm exclusively powers Shopify’s Shop Pay Installments.

This is a leg into a huge market and most likely Affirm will become the dominant option for all Shopify-powered websites.

- I was ready to invest in AFRM even if they were not nice. But..

Affirm’s mission is to help customers “spend responsibly”. The company has payment options that break up large purchases over a period of time. Unlike Credit Cards though, the company does this by fixing a set payment without hidden fees, or penalties. Having fixed payments and simple interest rates means that the company’s loans do not compound. This helps consumers avoid the “debt trap” caused by credit cards and compounding interest (i.e. when you need to pay interest on your interest).

I still think they are more mercurial than the European Company we talked about.

But those high interest rates kill the kids! So we are helping out the country.

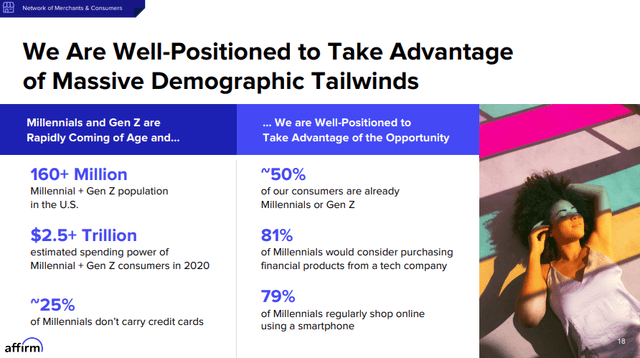

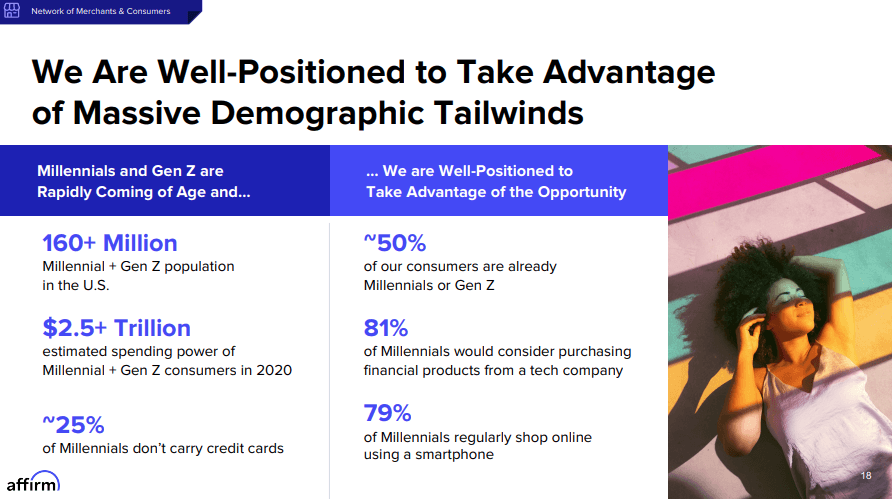

Trend- * TD Bank’s survey claiming that approximately 25% of Millennials do not carry credit cards. This is also corroborated by a Deloitte study that shows 52% of Gen Z and 41% of millennials prefer to use debit cards.

-- Harris Poll in 2020, indicating that 64% of Americans (81% for those between 18 -34 years old) would prefer financial products from a technology company’s platform instead of a traditional financial services provider.

Jamie Dimon is in his nice speech called out the dangers companies like AFRM present top major banks-- the $100 billion credit card industry is ripe for disruption.

Yup 50% of customers are millennials or Gen Z.

There are competitors in the space fighting for small clothing sales.

AFRM has Walmart<---- & Affirm already has multiple partnerships in place with major e-commerce players such as Peloton (PTON), Purple (PRPL), Expedia (EXPE), etc.

Of the US co's in the space AFRM is lead dog the biggest. And as such they can afford to->

have longer loans!!!<----Affirm has the longest loan term length from 3 months to 3 years. Compare that to Afterpay or Klarna’s loan term length of 6 weeks and 2 months respectively.

Summing up-- Yea it's not cheap but it's not cheap for a reason.

I think Affirm’s revenues could hit $6 Billion in five years.

Looking at the underlying metrics, we can see that Affirm is firing on all cylinders. The company has a high average annual spend by repeat customers of $2,200 and high loyalty to the platform with 64% of transactions being driven by repeat users. On the merchant side as well the company has a 100% Dollar-Based merchant retention.

That Is Why I cornered this high flyer suffering from Lockup expiration of shares.....~si

BofA says don't buy Affirm Holdings stock yet!

I like that especially when Barons went the other way and said it was a very good idea.

- Another aspct I like of the co is they tend to be used for big ticket items! That's the kind we like to pay later for!

- Another aspect is the fact that Affirm exclusively powers Shopify’s Shop Pay Installments.

This is a leg into a huge market and most likely Affirm will become the dominant option for all Shopify-powered websites.

- I was ready to invest in AFRM even if they were not nice. But..

Affirm’s mission is to help customers “spend responsibly”. The company has payment options that break up large purchases over a period of time. Unlike Credit Cards though, the company does this by fixing a set payment without hidden fees, or penalties. Having fixed payments and simple interest rates means that the company’s loans do not compound. This helps consumers avoid the “debt trap” caused by credit cards and compounding interest (i.e. when you need to pay interest on your interest).

I still think they are more mercurial than the European Company we talked about.

But those high interest rates kill the kids! So we are helping out the country.

Trend- * TD Bank’s survey claiming that approximately 25% of Millennials do not carry credit cards. This is also corroborated by a Deloitte study that shows 52% of Gen Z and 41% of millennials prefer to use debit cards.

-- Harris Poll in 2020, indicating that 64% of Americans (81% for those between 18 -34 years old) would prefer financial products from a technology company’s platform instead of a traditional financial services provider.

Jamie Dimon is in his nice speech called out the dangers companies like AFRM present top major banks-- the $100 billion credit card industry is ripe for disruption.

Yup 50% of customers are millennials or Gen Z.

There are competitors in the space fighting for small clothing sales.

AFRM has Walmart<---- & Affirm already has multiple partnerships in place with major e-commerce players such as Peloton (PTON), Purple (PRPL), Expedia (EXPE), etc.

Of the US co's in the space AFRM is lead dog the biggest. And as such they can afford to->

have longer loans!!!<----Affirm has the longest loan term length from 3 months to 3 years. Compare that to Afterpay or Klarna’s loan term length of 6 weeks and 2 months respectively.

Summing up-- Yea it's not cheap but it's not cheap for a reason.

I think Affirm’s revenues could hit $6 Billion in five years.

Looking at the underlying metrics, we can see that Affirm is firing on all cylinders. The company has a high average annual spend by repeat customers of $2,200 and high loyalty to the platform with 64% of transactions being driven by repeat users. On the merchant side as well the company has a 100% Dollar-Based merchant retention.

That Is Why I cornered this high flyer suffering from Lockup expiration of shares.....~si

Why?

Why is it near an all-time low when the indexes are all bouncing off time highs?

Maybe the question is why are the indexes bouncing off highs?

Stick a Pin in Granny's Shorts Van! wake her up!

Pinterest sees worst drop in weeks as Cleveland hints at weak end to quarter

Apr. 16, 2021 10:57 AM ETPinterest, Inc. (PINS)

Why is it near an all-time low when the indexes are all bouncing off time highs?

Maybe the question is why are the indexes bouncing off highs?

Stick a Pin in Granny's Shorts Van! wake her up!

Pinterest sees worst drop in weeks as Cleveland hints at weak end to quarter

Apr. 16, 2021 10:57 AM ETPinterest, Inc. (PINS)

- Pinterest(NYSE:PINS)is7.3% lowerin the stock's worst one-day decline in weeks, alongside some inklings that the quarter mayhave fizzed at bit toward the end.

Van are you in--

GMVHY

57 followers + Van + Stoney = 59 followers- Entain Plc

$22.92

0.69(+3.10%)-->

GMVHY

57 followers + Van + Stoney = 59 followers- Entain Plc

$22.92

0.69(+3.10%)-->

Grocery stores run up against tough pantry-loading comparable.

This sentiment is going to play out in a variety of sectors. The stuff that was hoarded in the beginning of the break out now face troubling comparisons. My work has shown that Sprouts Farmers Market is NOT GOING TO HAVE THAT PROBLEM for a variety of reasons.. mostly new openings! <-- we are catching this co in a build out phase of smaller stores that will pack the same financial punch in a smaller store format! We are lucky vs a Krogers that will have a static store base and very hard comparisons... This gives Sprouts a big leg up.

Eating healthier. Farmers market mentality.. yes and Yes! SFM right pace right time.

This sentiment is going to play out in a variety of sectors. The stuff that was hoarded in the beginning of the break out now face troubling comparisons. My work has shown that Sprouts Farmers Market is NOT GOING TO HAVE THAT PROBLEM for a variety of reasons.. mostly new openings! <-- we are catching this co in a build out phase of smaller stores that will pack the same financial punch in a smaller store format! We are lucky vs a Krogers that will have a static store base and very hard comparisons... This gives Sprouts a big leg up.

Eating healthier. Farmers market mentality.. yes and Yes! SFM right pace right time.

A guy gives out three great buys on a sleepy Friday when no one else had an idea at all, I was thinking there would be more Thank you's here... well after next week, they'll start to roll in I guess. Not that it matters.

I even gave out CureVac.... Nothing. Maybe it's time for ole' stoney to pack up his bag of tricks and move on to summer activities.

On the financial side, we closed 2020 with a favorable cash position of EUR 1.32 billion. Since then, we were able to raise an additional USD 517 million issuing new shares in a successful follow-on to our IPO in August last year. Pierre will later walk you through the financial details.

I'm now on Slide 5 of the presentation to briefly highlight the fundamental corporate transformation that has taken the company to a new level in 2020 and is continuing in 2021. Since initiation of our COVID-19 vaccine program at the beginning of 2020, our business has evolved as a clinical development of the lead vaccine candidates, CVnCoV accelerated. We are going to -- we are growing the talent base in every area of the company and are rapidly building our commercial infrastructure and expertise under the leadership of Antony Blanc, who joined us as chief business and commercial officer in December 2020. In 2020, we secured a commercial commitment from the European Commission for 225 million doses of CVnCoV with the option of an additional 180 million dosages to be delivered.

We are executing on our financial strategy. And in 2020, we're able to secure significant funds through a private financing round directly followed by our NASDAQ listing, as well as, a grant from the German government. In addition, we received a EUR 450 million upfront payment from the European Commission as part of the order for the 225 million vaccine dosages. Since then, we were able to add another USD 517 million through a successful IPO follow-on financing.

CVAC UP $13 from purchase already!!! /// Important FDA news coming May /June<-- looking more like May!

CureVac N.V. (CVAC)-

$109.29+5.24 (+5.04%)<---------

At close: April 16 4:00PM EDT

I even gave out CureVac.... Nothing. Maybe it's time for ole' stoney to pack up his bag of tricks and move on to summer activities.

On the financial side, we closed 2020 with a favorable cash position of EUR 1.32 billion. Since then, we were able to raise an additional USD 517 million issuing new shares in a successful follow-on to our IPO in August last year. Pierre will later walk you through the financial details.

I'm now on Slide 5 of the presentation to briefly highlight the fundamental corporate transformation that has taken the company to a new level in 2020 and is continuing in 2021. Since initiation of our COVID-19 vaccine program at the beginning of 2020, our business has evolved as a clinical development of the lead vaccine candidates, CVnCoV accelerated. We are going to -- we are growing the talent base in every area of the company and are rapidly building our commercial infrastructure and expertise under the leadership of Antony Blanc, who joined us as chief business and commercial officer in December 2020. In 2020, we secured a commercial commitment from the European Commission for 225 million doses of CVnCoV with the option of an additional 180 million dosages to be delivered.

We are executing on our financial strategy. And in 2020, we're able to secure significant funds through a private financing round directly followed by our NASDAQ listing, as well as, a grant from the German government. In addition, we received a EUR 450 million upfront payment from the European Commission as part of the order for the 225 million vaccine dosages. Since then, we were able to add another USD 517 million through a successful IPO follow-on financing.

CVAC UP $13 from purchase already!!! /// Important FDA news coming May /June<-- looking more like May!

CureVac N.V. (CVAC)-

$109.29+5.24 (+5.04%)<---------

At close: April 16 4:00PM EDT