There's another grave possibility. Maybe these insiders know that they will continue to be rewarded with more shares as a part of their compensation packages, so they were quite active with their recent rounds of share sales. Palantir's continuously high stock-based compensation expenses are a red flag

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

GBA's "2021 Stock Phantasma"

- Thread starter stonedinvestor

- Start date

Thank you for getting me out of RAIL, can buy it back $1 cheaper now. Took a short on BIDU $180s paid $1-$2, out at above $5 VIAC, DISCA after buying the $50 puts it imploded $42. You get the feeling they’re tanking the Market on each gap?I know they're expensive, but for a quick trade those $135 calls on $UPST @18.50 could double today.

Unless they flatline it into the close. It looks poised to jump though.

I wouldn't hold them over the weekend however, just a Friday PM trade.

Edit... they jumped as I was typing that.

VIAC taking out $40, excellent short need to sell my puts while IV is nuts. Stoney never mentioned MO, keeps grinding higher with TXN.Thank you for getting me out of RAIL, can buy it back $1 cheaper now. Took a short on BIDU $180s paid $1-$2, out at above $5 VIAC, DISCA after buying the $50 puts it imploded $42. You get the feeling they’re tanking the Market on each gap?

Drive Shack: Worth Another Swing Here Van

Mar. 26, 2021 8:00 AM ETDrive Shack Inc.

Summary

Drive Shack Inc.(NYSE:DS) is a leader in the golf industry with a business of operating 60 golf course properties across the U.S. In recent years, the company has shifted its strategic focus towards innovative golf driving ranges with the "Drive Shack" concept along with announcing a new mini-golf-centered "Puttery" brand. These are modern entertainment venues combining an adult-focused social setting with craft food and beverage options.

Despite disruptions last year due to the pandemic, the company sees a significant growth opportunity supported by market demand and attractive venue-level economics. Drive Shack just reported its lasted quarterly results highlighted by improving financials and a positive outlook. We are bullish and see upside in the year ahead with DS benefiting from accelerating sales momentum as the pandemic ends.

OMG so cheap Van is so lucky

DS Earnings Recap

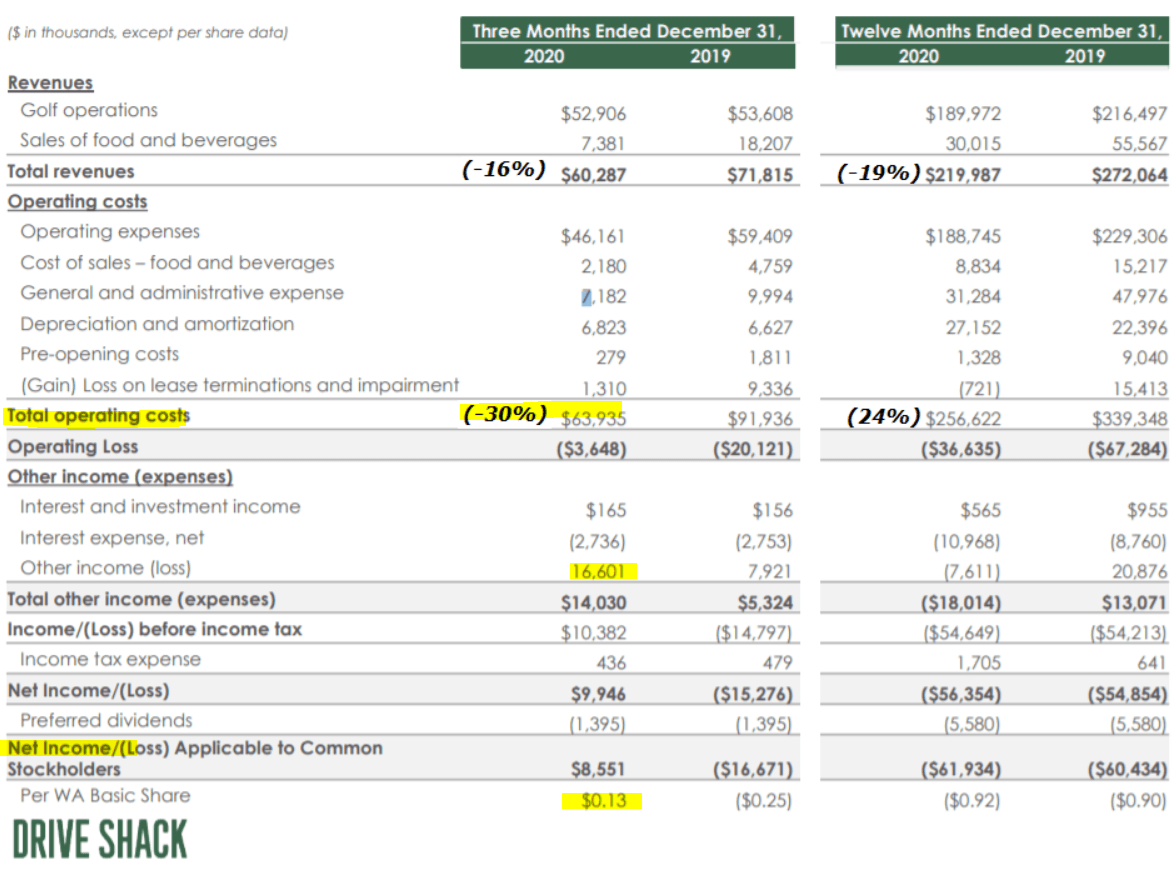

Drive Shack Inc reported its fiscal 2020 Q4 earnings on March 12th with GAAP EPS of $0.13 representing shareholder net income of $8.6 million, reversing a loss of $16.7 million in the period last year. The positive net income was driven in part by a gain of $16.6 million in "other income" related to the sale of a traditional golf course property as it consolidates that part of the business.

Revenue of $60.3 million in the quarter declined by 16.1% year-over-year consistent with lower sales at Drive Shack venue locations due to COVID restrictions in some markets. Nevertheless, efforts at cost control including a 30% decline in total operating expenses helped narrow the operating loss in Q4 to just $3.6 million compared to $20.1 million in Q4 2019. For the full-year 2020, revenues fell by 19% while the negative EPS of $0.92 was approximately flat compared to the $0.90 loss in 2019.

(Source:Company IR/annotation by BOOX Research)

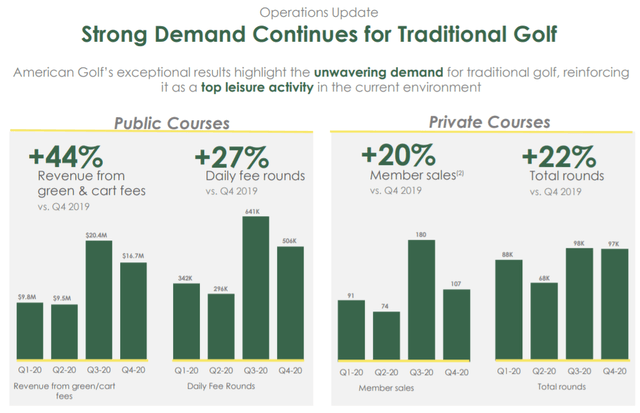

For some context behind the numbers, the traditional golf course operations through the American Golf "AGC" segment still represents about 88% of total company revenues at $53.1 million in Q4. Drive Shack saw a 27% y/y increase to daily fees revenues at the public courses in its portfolio while private courses saw 20% growth in member sales. On the other hand, since the company has been divesting from this segment with sales of company-owned properties in recent years, total AGC revenues declined by 23% in 2020 adding to the top-line revenue decline.

(source:Company IR)

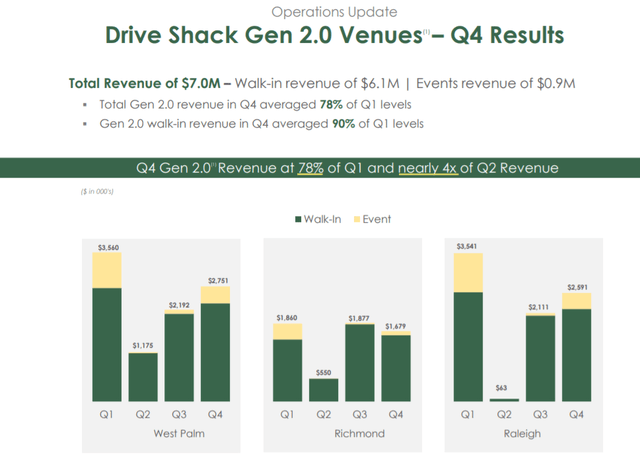

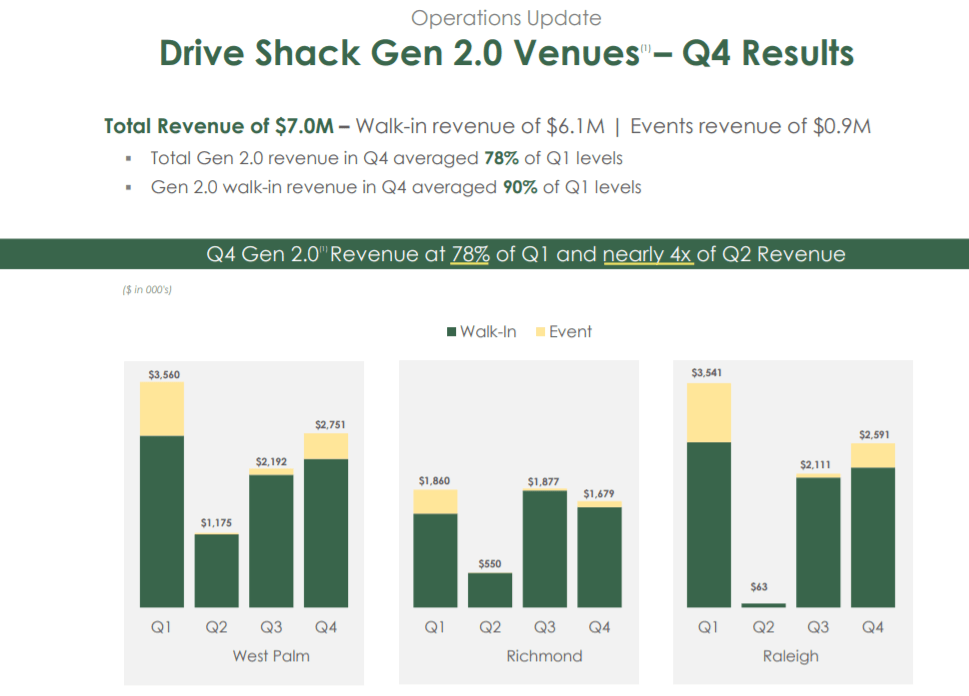

As mentioned, the focus for Drive Shack and its long-term growth opportunity is in the "Gen 2.0 Venues" across 4 current Drive Shack locations. Q4 revenue from Drive Shake Gen 2.0 venues was down 44% year over year at $7.2 million considering still challenged traffic levels and lower corporate events at the venues amid the ongoing pandemic. Favorably, management is highlighting the recovery over the last two quarters compared to Q2 at the height of the pandemic when locations were temporarily shut down. Q4 segment revenues reached 78% of Q1 and up sequentially from Q3. Fewer companies holding corporate events along with limited large-group parties have also pressured the results considering the circumstances.

(Source:Company IR)

Puttery as the Near-Term Growth Opportunity- Ya think!

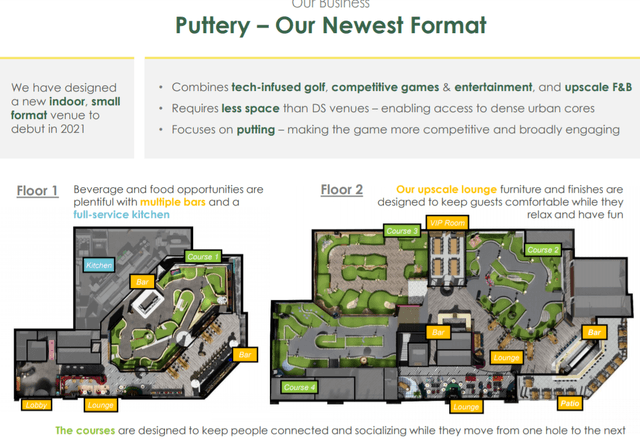

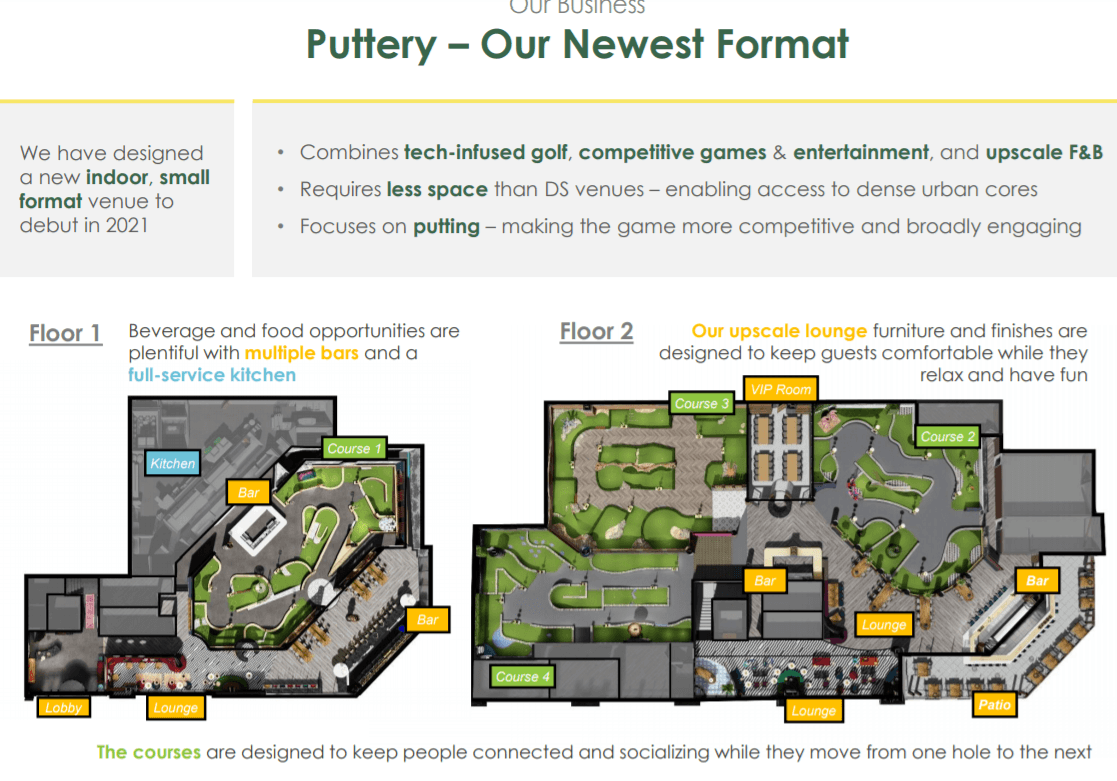

One development for the company is the upcoming launch of its newest format called "Puttery." In contrast to the Drive Shack concept centered around the "driving range", think of Puttery as a sports-bar/ lounge for adults with a mini-golf putting course and other tech-based golf games.

(Source:Company IR)

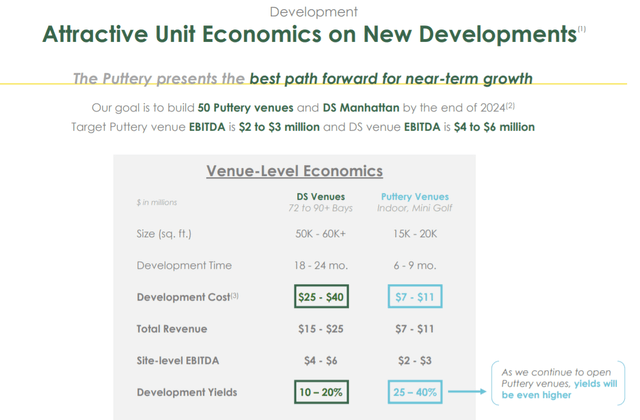

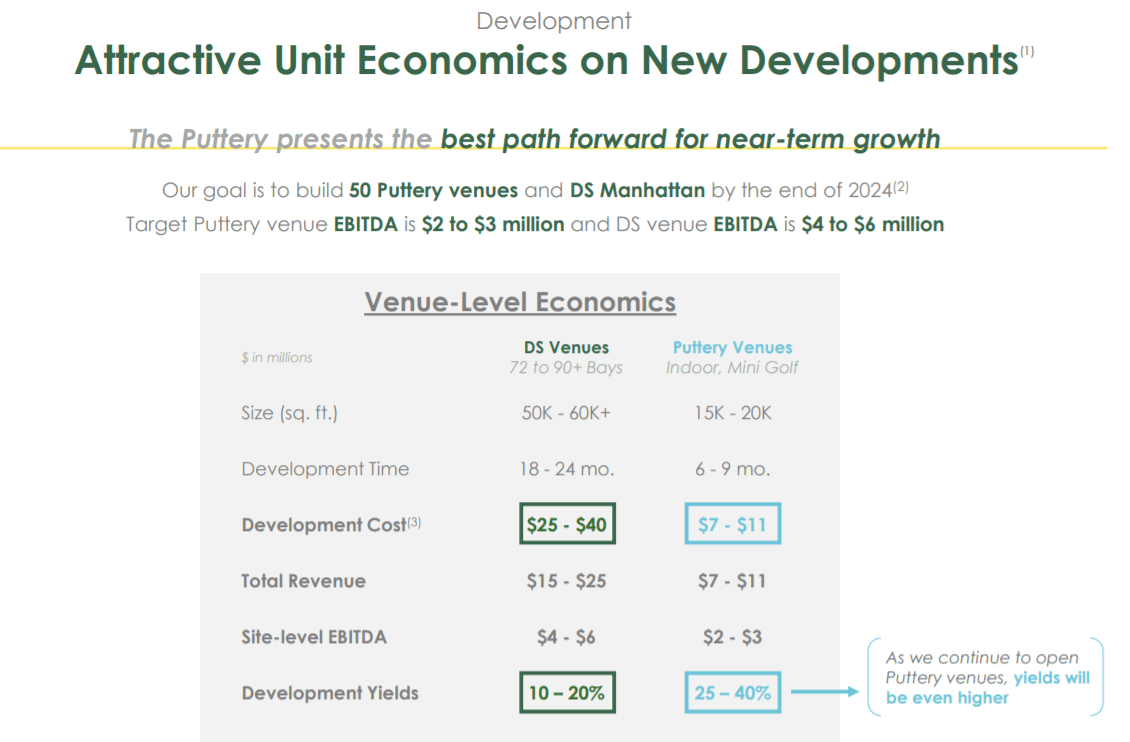

The advantage of focusing Puttery locations over building more Drive Shacks is that the format requires less space with lower development costs. Management expects each Puttery venue to deliver site-level EBITDA between $2 and $3 million per year. While this is half the expected amount of the larger Drive Shack concept, with a site-level EBITDA between $4 and $6 million, the venue-level economics of the smaller Puttery locations can represent a higher project yield and return on investment potential. The company is on track to open 7 Puttery locations just this year with a pipeline for locations in 24 markets beyond 2022 as a major growth driver going forward.

(Source:Company IR)

In January, Drive Shack announced it was partnering with professional golferRory McIlroy, recognized as one of the top players in the world, to promote the Puttery brand as an ambassador. The first two locations are set to open between Q2 and Q3 in Dallas and Charlotte this year.

Drive Shack reported a balance sheet cash position of $86 million as of February 28th, 2021 which includes approximately $50 million raised through anequity offeringcompleted in January. The company believes that current liquidity is sufficient to fund its development costs for 2021 while signaling an intention to tap debt markets later this year to fund 2022 construction costs. While management is not offering earnings or sales guidance for 2021, comments in the press release and conference call projected optimism in the year ahead with an expectation that operations normalize. From thepress release:

As we look ahead into 2021, our focus remains on strategic priorities to drive growth and profitability, including the launch and expansion of Puttery, capturing market share using data and analytics, growing brand awareness and advancing technology and innovation to remain at the forefront in our space. With our currently liquidity position and relatively unlevered balance sheet, we can maintain flexibility and optimize our capital stricture to be better positioned to react to future business needs. We believe 2021 will be a momentous year for us that is carried by a team that sets us apart and will drive us forward.

Analysis and Forward-Looking Commentary

The title of our article here alludes to the last time we covered Drive Shack in May of 2020 when the stock was trading under $1.50 and we said it was "worth a swing" for the upside potential. Our take is that while shares have rallied significantly already, the outlook for both the company and at the macro level has progressed better than expected. We reaffirm our bullish view on the stock and think it can climb higher from here.

One of the surprises last year following the early stages of the pandemic was thisindustry-wide boomof interest towards golf with people looking for outdoor socially-distanced recreational activities. Even the data from Drive Shack regarding the increase in comparable daily rounds fees at its traditional public courses and higher membership at the private facilities collaborate these trends. In many ways, the alternative Drive Shack driving ranges and Puttery mini-golf concepts can benefit from these same dynamics combining another opportunity for people to participate in the sport in a social setting.

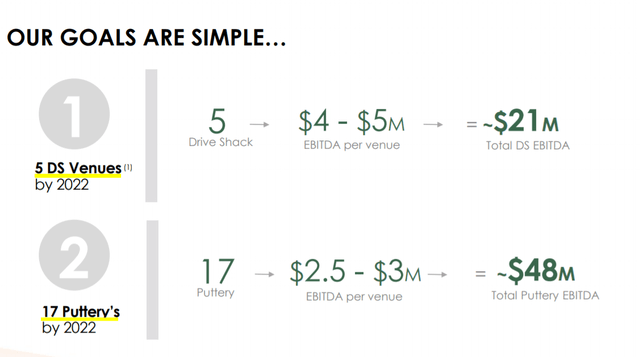

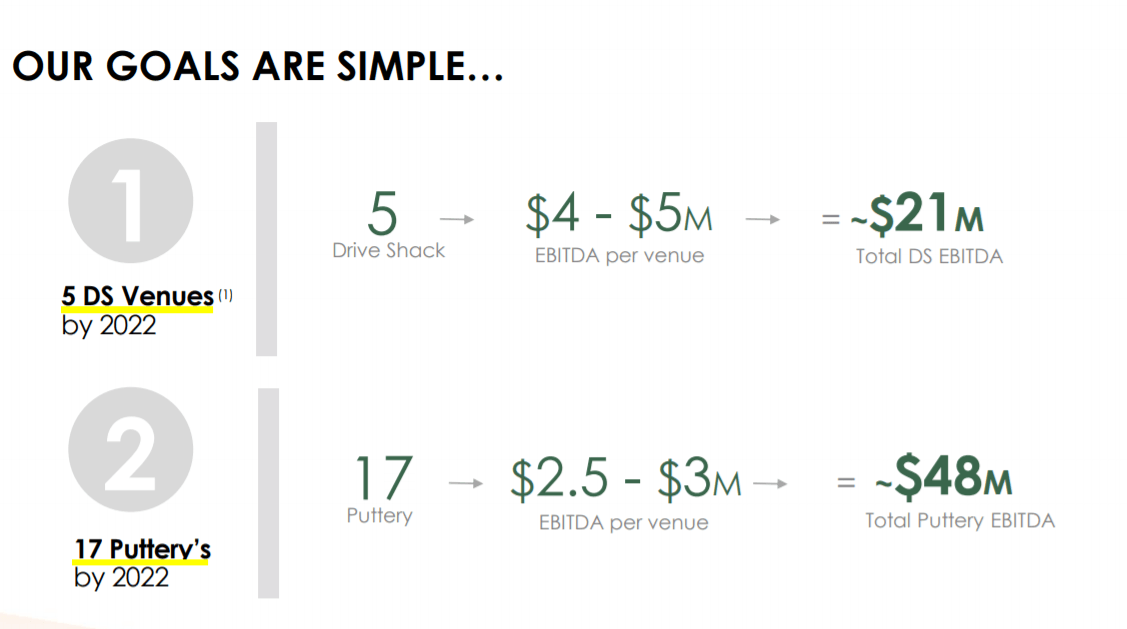

We believe that as the pandemic ends, Drive Shack facilities will be in high-demand setting up a strong launch of the new Puttery venues that can be successful in each new market. Taking the management guidance for venue-level EBITDA forecasts, the 10 new Puttery locations set to open in 2021 can together contribute an EBITDA run-rate between $20 to $30 million by the end of the year in addition to the existing operation. Looking ahead towards 2022 when Drive Shack expects to have 17 Puttery locations and 5 DS venues, there is visibility for an EBITDA run-rate above $80 million across all properties including the traditional golf courses.

(Source:Company IR)

In the context of the company's current market cap at $275 million or $335 million in enterprise value, we view the current stock valuation as compelling given the growth opportunity. The EBITDA estimates imply shares of DS are trading at a forward EV to EBITDA multiple under 4.5x considering the potential run-rate by the end of 2022. Depending on the timing of each venue launch, firm-wide revenues could double by 2023 from the current level as each facility ramps up towards normalized capacity and benefits from brand awareness.

The attraction of the Puttery is that it is relatively unique compared to the driving range "Drive Shack" model that faces some competition in the market including names like "Top Golf" owned by Callaway Golf Co. (ELY). Puttery will benefit from a novelty aspect and keep customers coming back for the atmosphere in the hip sports-bar setting. Dave & Buster's Entertainment Inc. (PLAY) as a sports-bar arcade for adults comes to mind as comparable to Puttery. Notably, PLAY has traded with an average EV to EBITDA multiple closer to 10x over the past 5 years highlighting a potential upside of over 100% for shares of Drive Shack if it can execute on its growth strategy.

Final Thoughts

We are bullish and rate shares of DS as a buy with a year-ahead price target of $4.00 representing 30% upside and a 6x EV to EBITDA against the estimated 2022 EBITDA run-rate potential. Investors can look forward to the upcoming launch of the first Puttery location to give insight into the brand momentum and response by consumers. We also believe existing Drive Shack locations will perform well with strong demand as the pandemic ends.

Mar. 26, 2021 8:00 AM ETDrive Shack Inc.

Summary

- Drive Shack is benefiting from renewed interest in golf as the industry got a boost during the pandemic.

- The company expects to open 7 "Puttery" locations this year and 10 in 2022 as a new adult-focused mini-golf entertainment venue concept.

- We are bullish on the stock and see upside in 2021 as the company executes its growth strategy and benefits from normalizing operations as the pandemic ends.

Drive Shack Inc.(NYSE:DS) is a leader in the golf industry with a business of operating 60 golf course properties across the U.S. In recent years, the company has shifted its strategic focus towards innovative golf driving ranges with the "Drive Shack" concept along with announcing a new mini-golf-centered "Puttery" brand. These are modern entertainment venues combining an adult-focused social setting with craft food and beverage options.

Despite disruptions last year due to the pandemic, the company sees a significant growth opportunity supported by market demand and attractive venue-level economics. Drive Shack just reported its lasted quarterly results highlighted by improving financials and a positive outlook. We are bullish and see upside in the year ahead with DS benefiting from accelerating sales momentum as the pandemic ends.

OMG so cheap Van is so lucky

DS Earnings Recap

Drive Shack Inc reported its fiscal 2020 Q4 earnings on March 12th with GAAP EPS of $0.13 representing shareholder net income of $8.6 million, reversing a loss of $16.7 million in the period last year. The positive net income was driven in part by a gain of $16.6 million in "other income" related to the sale of a traditional golf course property as it consolidates that part of the business.

Revenue of $60.3 million in the quarter declined by 16.1% year-over-year consistent with lower sales at Drive Shack venue locations due to COVID restrictions in some markets. Nevertheless, efforts at cost control including a 30% decline in total operating expenses helped narrow the operating loss in Q4 to just $3.6 million compared to $20.1 million in Q4 2019. For the full-year 2020, revenues fell by 19% while the negative EPS of $0.92 was approximately flat compared to the $0.90 loss in 2019.

(Source:Company IR/annotation by BOOX Research)

For some context behind the numbers, the traditional golf course operations through the American Golf "AGC" segment still represents about 88% of total company revenues at $53.1 million in Q4. Drive Shack saw a 27% y/y increase to daily fees revenues at the public courses in its portfolio while private courses saw 20% growth in member sales. On the other hand, since the company has been divesting from this segment with sales of company-owned properties in recent years, total AGC revenues declined by 23% in 2020 adding to the top-line revenue decline.

(source:Company IR)

As mentioned, the focus for Drive Shack and its long-term growth opportunity is in the "Gen 2.0 Venues" across 4 current Drive Shack locations. Q4 revenue from Drive Shake Gen 2.0 venues was down 44% year over year at $7.2 million considering still challenged traffic levels and lower corporate events at the venues amid the ongoing pandemic. Favorably, management is highlighting the recovery over the last two quarters compared to Q2 at the height of the pandemic when locations were temporarily shut down. Q4 segment revenues reached 78% of Q1 and up sequentially from Q3. Fewer companies holding corporate events along with limited large-group parties have also pressured the results considering the circumstances.

(Source:Company IR)

Puttery as the Near-Term Growth Opportunity- Ya think!

One development for the company is the upcoming launch of its newest format called "Puttery." In contrast to the Drive Shack concept centered around the "driving range", think of Puttery as a sports-bar/ lounge for adults with a mini-golf putting course and other tech-based golf games.

(Source:Company IR)

The advantage of focusing Puttery locations over building more Drive Shacks is that the format requires less space with lower development costs. Management expects each Puttery venue to deliver site-level EBITDA between $2 and $3 million per year. While this is half the expected amount of the larger Drive Shack concept, with a site-level EBITDA between $4 and $6 million, the venue-level economics of the smaller Puttery locations can represent a higher project yield and return on investment potential. The company is on track to open 7 Puttery locations just this year with a pipeline for locations in 24 markets beyond 2022 as a major growth driver going forward.

(Source:Company IR)

In January, Drive Shack announced it was partnering with professional golferRory McIlroy, recognized as one of the top players in the world, to promote the Puttery brand as an ambassador. The first two locations are set to open between Q2 and Q3 in Dallas and Charlotte this year.

Drive Shack reported a balance sheet cash position of $86 million as of February 28th, 2021 which includes approximately $50 million raised through anequity offeringcompleted in January. The company believes that current liquidity is sufficient to fund its development costs for 2021 while signaling an intention to tap debt markets later this year to fund 2022 construction costs. While management is not offering earnings or sales guidance for 2021, comments in the press release and conference call projected optimism in the year ahead with an expectation that operations normalize. From thepress release:

As we look ahead into 2021, our focus remains on strategic priorities to drive growth and profitability, including the launch and expansion of Puttery, capturing market share using data and analytics, growing brand awareness and advancing technology and innovation to remain at the forefront in our space. With our currently liquidity position and relatively unlevered balance sheet, we can maintain flexibility and optimize our capital stricture to be better positioned to react to future business needs. We believe 2021 will be a momentous year for us that is carried by a team that sets us apart and will drive us forward.

Analysis and Forward-Looking Commentary

The title of our article here alludes to the last time we covered Drive Shack in May of 2020 when the stock was trading under $1.50 and we said it was "worth a swing" for the upside potential. Our take is that while shares have rallied significantly already, the outlook for both the company and at the macro level has progressed better than expected. We reaffirm our bullish view on the stock and think it can climb higher from here.

One of the surprises last year following the early stages of the pandemic was thisindustry-wide boomof interest towards golf with people looking for outdoor socially-distanced recreational activities. Even the data from Drive Shack regarding the increase in comparable daily rounds fees at its traditional public courses and higher membership at the private facilities collaborate these trends. In many ways, the alternative Drive Shack driving ranges and Puttery mini-golf concepts can benefit from these same dynamics combining another opportunity for people to participate in the sport in a social setting.

We believe that as the pandemic ends, Drive Shack facilities will be in high-demand setting up a strong launch of the new Puttery venues that can be successful in each new market. Taking the management guidance for venue-level EBITDA forecasts, the 10 new Puttery locations set to open in 2021 can together contribute an EBITDA run-rate between $20 to $30 million by the end of the year in addition to the existing operation. Looking ahead towards 2022 when Drive Shack expects to have 17 Puttery locations and 5 DS venues, there is visibility for an EBITDA run-rate above $80 million across all properties including the traditional golf courses.

(Source:Company IR)

In the context of the company's current market cap at $275 million or $335 million in enterprise value, we view the current stock valuation as compelling given the growth opportunity. The EBITDA estimates imply shares of DS are trading at a forward EV to EBITDA multiple under 4.5x considering the potential run-rate by the end of 2022. Depending on the timing of each venue launch, firm-wide revenues could double by 2023 from the current level as each facility ramps up towards normalized capacity and benefits from brand awareness.

The attraction of the Puttery is that it is relatively unique compared to the driving range "Drive Shack" model that faces some competition in the market including names like "Top Golf" owned by Callaway Golf Co. (ELY). Puttery will benefit from a novelty aspect and keep customers coming back for the atmosphere in the hip sports-bar setting. Dave & Buster's Entertainment Inc. (PLAY) as a sports-bar arcade for adults comes to mind as comparable to Puttery. Notably, PLAY has traded with an average EV to EBITDA multiple closer to 10x over the past 5 years highlighting a potential upside of over 100% for shares of Drive Shack if it can execute on its growth strategy.

Final Thoughts

We are bullish and rate shares of DS as a buy with a year-ahead price target of $4.00 representing 30% upside and a 6x EV to EBITDA against the estimated 2022 EBITDA run-rate potential. Investors can look forward to the upcoming launch of the first Puttery location to give insight into the brand momentum and response by consumers. We also believe existing Drive Shack locations will perform well with strong demand as the pandemic ends.

URI

A look at United

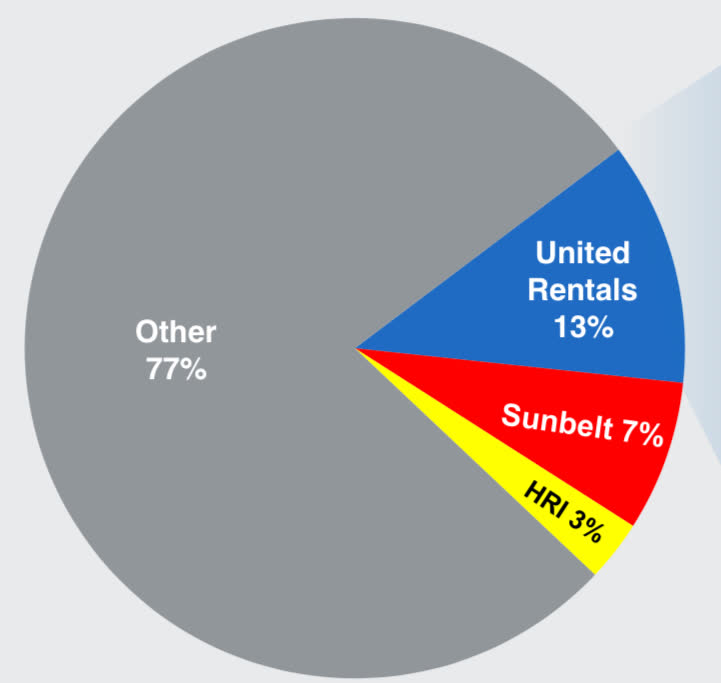

United has a rather simple business model. In short, the company rents out machinery and equipment. According to their estimate, they are the largest player in the space with a 13% market share. The next largest, by revenue, is a firm called Sunbelt. Its market share is a little more than half of this at 7%.

What is really impressive is just how fragmented the industry is. Despite the top two largest players in the space controlling 20% of the market, the top 10 players account for just 36% of the market. That means that the next eight largest players combined average just 2% of the industry. Another interesting thing is just how much more concentrated, and less fragmented, the space has become. Back in 2010, the top 10 players accounted for just 20% of the industry.

This means a considerable consolidation is taking place, and that trend is likely to continue. Given United’s dominance in the market, this should give them a great chance to grow further. In fact, the company has been a huge beneficiary of this trend so far. From 2012 through 2020, really ending in 2018 since it made no real acquisitions since then, it had allocated over $10 billion toward buying up its competitors.

$324.34 +10.10(+3.21%)

2:31 PM

A look at United

United has a rather simple business model. In short, the company rents out machinery and equipment. According to their estimate, they are the largest player in the space with a 13% market share. The next largest, by revenue, is a firm called Sunbelt. Its market share is a little more than half of this at 7%.

What is really impressive is just how fragmented the industry is. Despite the top two largest players in the space controlling 20% of the market, the top 10 players account for just 36% of the market. That means that the next eight largest players combined average just 2% of the industry. Another interesting thing is just how much more concentrated, and less fragmented, the space has become. Back in 2010, the top 10 players accounted for just 20% of the industry.

This means a considerable consolidation is taking place, and that trend is likely to continue. Given United’s dominance in the market, this should give them a great chance to grow further. In fact, the company has been a huge beneficiary of this trend so far. From 2012 through 2020, really ending in 2018 since it made no real acquisitions since then, it had allocated over $10 billion toward buying up its competitors.

$324.34 +10.10(+3.21%)

2:31 PM

MGM Resorts International: Room For Further Upside As BetMGM Rolls Out

Summary

MGM Resorts International (NYSE:MGM) is swiftly recovering from the corona-crisis and has shown encouraging revenue and EBITDA growth in the latest quarters, which is set to be increased for the remainder of 2021 as vaccinations accelerate in the U.S., leading to herd immunity.

The company is also aggressively focusing on its expansion of BetMGM, an online gambling platform currently online in a few states, with a significantly increased presence in the rest of the U.S. by the end of 2021.

Online gambling is currently experiencing an upswing in the U.S. as states roll back regulations to fight budget deficits and increase tax-collection from gambling businesses.

A target price of $50-$60 seems reasonable over the 24 months.

The company is currently focused on increasing its BetMGM division, which is focused on online gambling. A timely initiative as online gambling restrictions across states is set to be loosened as states seek new ways to increase tax-collectiont o battle soaring budget deficits.

Expansion into online gambling is significant as the U.S. is slowly recovering from the corona crisis, with a population accustomed to online-gambling due to the forced switch induced by the corona crisis during 2020. In other words, adults will have an increased familiarity and increased propensity to online gambling in the post-Covid world, which will benefit BetMGM.

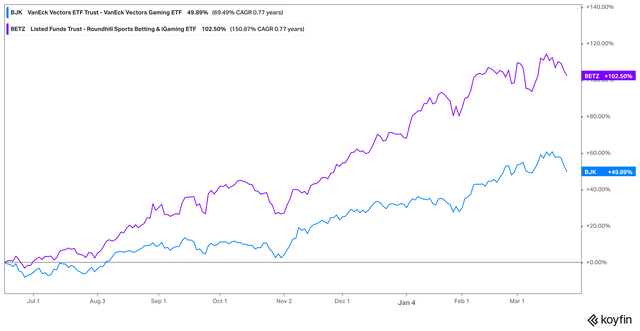

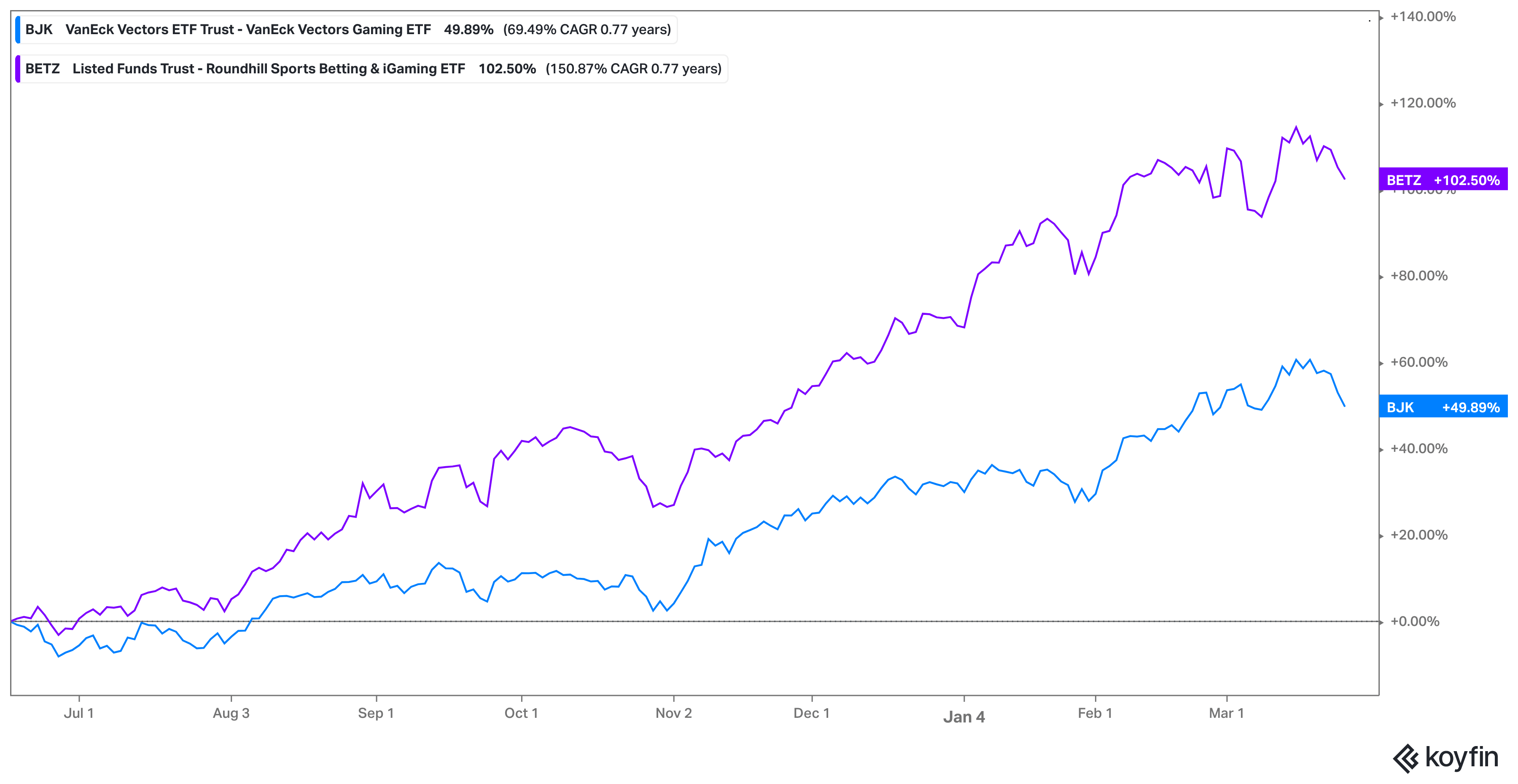

If we analyze these developments from a broader-market perspective of online gambling, we can clearly see that market participants have not missed out on this opportunity as two sports betting ETFs; Roundhill Sports Betting & iGaming(NYSEARCA:BETZ)and VanEck Vectors Gaming ETF(NASDAQ:BJK)have risen tremendously over the past year, suggesting future belief in online gambling.

Source: Koyfin

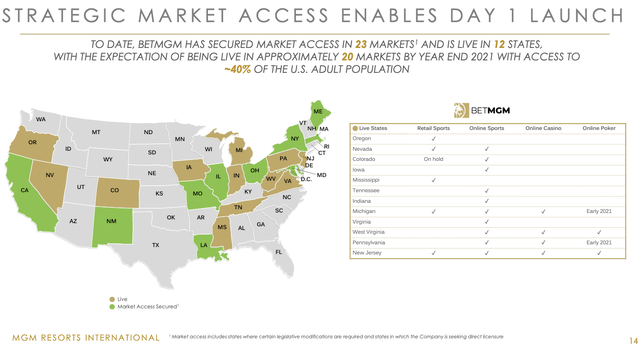

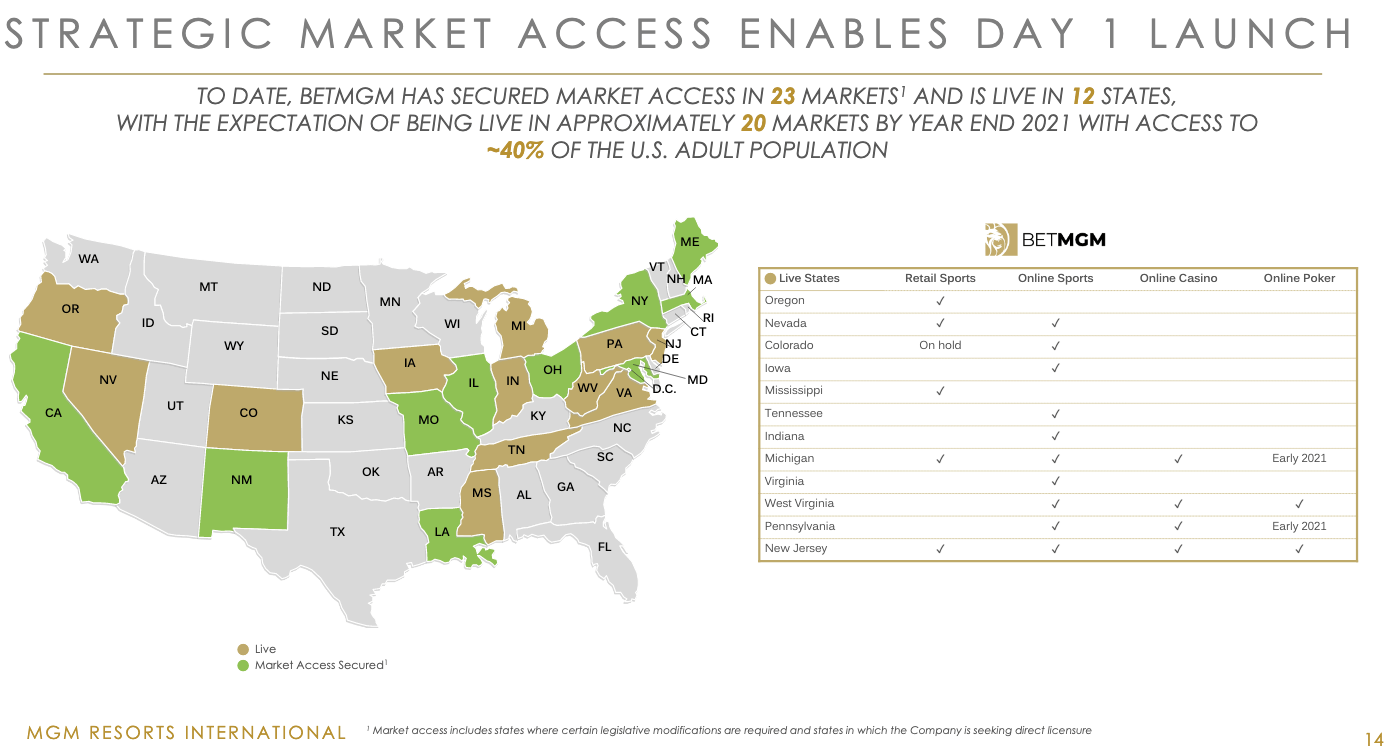

If we now analyze the current presence of BETMGM in the U.S. and plans for additional state online expansion, we can clearly see that there is a lot of future potential for upside in terms of increased revenue streams once online-presence is established in these jurisdictions.

BETMGM is rapidly expanding into additional jurisdictions.

To understand the potential of BETMGM, it is important to provide some context as to the revenue growth experienced in the early months of 2021 compared to 2020.

"Preliminary estimates of January's net gaming revenues associated with BetMGM operations was $44m," he explained. "On Super Bowl Sunday, the number of online bets placed, BetMGM was 11 times last year's online bets, and the online handle was 17 times last year's handle. That's why we remain aligned on investing aggressively to fund the growth of this business. And we expect to continue doing so this year in pursuit of this market opportunity."

Furthermore, the rollout of BETMGM so far in specific states has resulted in the company swiftly acquiring a large and sizable market share in online-gambling.

In two of its newest markets, Colorado and Tennessee, BetMGM had market shares of 31 percent and 34 percent, respectively in the fourth quarter. These share gains led to $178m of net gaming revenues associated with BetMGM in 2020 well above its target of $150m.

Mr. Hornbuckle added: "As each state rolls out, BetMGM is securing a leading market share position in the fourth quarter, BetMGM's market share was 17 percent and its retail and online markets, and 19 percent if you exclude Pennsylvania, which were only open for a part of December. This is a testament to BetMGM's successful execution and strong management teams as it continues to enter new states on a day one in game share and its existing markets."

So, basically stoney was right.

MGM

$36.72-1.21

but the market has voted against me.

I will be buying MORE MGM and MORE DS next week>>>>

Summary

- MGM has shown increasingly positive revenue and EBITDA trends as it is recovering from the Corona-induced slump in 2020.

- States loosening restrictions in online gambling is benefitting the entire industry and the expansion of BetMGM.

- A target price of $50 to $60 over the next 24 months is realistic.

- Potential conflict between state and federal gambling laws could pose a risk to the stock and gambling-related ETFs.

MGM Resorts International (NYSE:MGM) is swiftly recovering from the corona-crisis and has shown encouraging revenue and EBITDA growth in the latest quarters, which is set to be increased for the remainder of 2021 as vaccinations accelerate in the U.S., leading to herd immunity.

The company is also aggressively focusing on its expansion of BetMGM, an online gambling platform currently online in a few states, with a significantly increased presence in the rest of the U.S. by the end of 2021.

Online gambling is currently experiencing an upswing in the U.S. as states roll back regulations to fight budget deficits and increase tax-collection from gambling businesses.

A target price of $50-$60 seems reasonable over the 24 months.

The company is currently focused on increasing its BetMGM division, which is focused on online gambling. A timely initiative as online gambling restrictions across states is set to be loosened as states seek new ways to increase tax-collectiont o battle soaring budget deficits.

Expansion into online gambling is significant as the U.S. is slowly recovering from the corona crisis, with a population accustomed to online-gambling due to the forced switch induced by the corona crisis during 2020. In other words, adults will have an increased familiarity and increased propensity to online gambling in the post-Covid world, which will benefit BetMGM.

If we analyze these developments from a broader-market perspective of online gambling, we can clearly see that market participants have not missed out on this opportunity as two sports betting ETFs; Roundhill Sports Betting & iGaming(NYSEARCA:BETZ)and VanEck Vectors Gaming ETF(NASDAQ:BJK)have risen tremendously over the past year, suggesting future belief in online gambling.

Source: Koyfin

If we now analyze the current presence of BETMGM in the U.S. and plans for additional state online expansion, we can clearly see that there is a lot of future potential for upside in terms of increased revenue streams once online-presence is established in these jurisdictions.

BETMGM is rapidly expanding into additional jurisdictions.

To understand the potential of BETMGM, it is important to provide some context as to the revenue growth experienced in the early months of 2021 compared to 2020.

"Preliminary estimates of January's net gaming revenues associated with BetMGM operations was $44m," he explained. "On Super Bowl Sunday, the number of online bets placed, BetMGM was 11 times last year's online bets, and the online handle was 17 times last year's handle. That's why we remain aligned on investing aggressively to fund the growth of this business. And we expect to continue doing so this year in pursuit of this market opportunity."

Furthermore, the rollout of BETMGM so far in specific states has resulted in the company swiftly acquiring a large and sizable market share in online-gambling.

In two of its newest markets, Colorado and Tennessee, BetMGM had market shares of 31 percent and 34 percent, respectively in the fourth quarter. These share gains led to $178m of net gaming revenues associated with BetMGM in 2020 well above its target of $150m.

Mr. Hornbuckle added: "As each state rolls out, BetMGM is securing a leading market share position in the fourth quarter, BetMGM's market share was 17 percent and its retail and online markets, and 19 percent if you exclude Pennsylvania, which were only open for a part of December. This is a testament to BetMGM's successful execution and strong management teams as it continues to enter new states on a day one in game share and its existing markets."

So, basically stoney was right.

MGM

$36.72-1.21

but the market has voted against me.

I will be buying MORE MGM and MORE DS next week>>>>

Bought DISCA because I love Dr. Now and Guy Fierri $36.7 average and VIAC closed puts, bought at $42-$44(Old saying “If you liked the stock at $100, you’re going to love it at $40!). Bought FOXA average of $37 because I like adding to losing positions(Breaking Stoney and Van’s rules).

Where do I buy it back? $4.80 again and hold as dead money until earnings?See how the bottom fell out.

It's $5.22 now.

I hope you didn't buy any.