Revisiting Tea.-

Summary

- DavidsTea continues to make progress with its shift towards its e-commerce and wholesale channels growing by 145% in the most recent quarter.

- Substantially leaner organization as a result of the transformation led to back-to-back profitable quarters with the seasonally strongest quarter ahead.

- Introduction of new concepts like the recently launched subscription service is accompanied by a more than necessary change in the management team.

- DavidsTea is confident that it will successfully complete the restructuring process in the near term and emerge as a sustainably profitable company without diluting current shareholders.

Investment thesis

After a substantial increase in DAVIDsTEA Inc.'s (DavidsTea) (

DTEA) share price of more than 150% since my

last bullish article- published exactly 3 months ago - I want to put this price development into perspective. In this previous article, my valuation considerations made me argue that the fair value of the stock at the time was around US$ 5/share. In light of the recent events, however, the risk-reward profile has improved yet again, leading to an even higher valuation based on currently available information. As a result of the strong Q3 earnings and the information regarding the ongoing restructuring proceeding, I have revised the numbers in my financial model upwards and also updated my projection for the probable settlement payments. In addition, the management stated in the last conference call that they plan to successfully complete the restructuring process in the first quarter of 2021 and emerge from the CCAA proceeding as a leaner and more successful company without any dilutive impact for current shareholders. Finally, the fact that the main shareholder and interim CEO

Herschel Segal is stepping down at the age of nearly 90 and handing the reins over to

his daughter should also be received very well by the market. In sum, despite the recent surge in share price, I think the discrepancy between fair value and current market value is greater than ever.

All financial figures presented in this report are in C$ unless otherwise stated.

Review of Q3 figures and update of financial model

With the continued strong momentum in its e-commerce and wholesale channels, DavidsTea

posted another quarter of impressive growthin its two main distribution channels. In the third quarter, sales from e-commerce and wholesale channels increased by 145.5% to $22.1 million from $9.0 million in the prior-year quarter. As part of its formal restructuring process, the company exited all of its unprofitable brick-and-mortar stores except for 18 Canadian stores which were reopened on August 21, 2020. These 18 flagship stores generated $4.1 million in the third quarter, resulting in average sales per store of around $230 thousand over this ten-week period. By comparison, in the third quarter last year, average sales per store over the usual 14-week period have been approx. $130 thousand. Thus, sales per store in 2020 increased by 75% despite a shorter comparison period of 4 weeks. Against the background of the current COVID-19 pandemic, these results from its reopened stores are quite promising.

As a result of the still relatively high delivery and distribution costs, the gross margin for the third quarter came in at 41.3%. In my view, there is some significant potential for cost reductions in the logistics and packaging expenses.

As DavidsTea pivots to a digital-first strategy, it is showing continuous improvements in profitability driven by its focus on the e-commerce and wholesale channels. In the last quarter, adjusted EBITDA was in positive territory for a second consecutive quarter with $3.3 million compared to negative $2.2 million in the third quarter of last year (reported EBITDA even amounted to $15.3 million, mainly due to accounting gains as a result of the restructuring process). This highly attractive EBITDA margin of 12.6% is a consequence of the strong sales traction for both channels as well as the significantly reduced general and administrative infrastructure necessary to support the ongoing business.

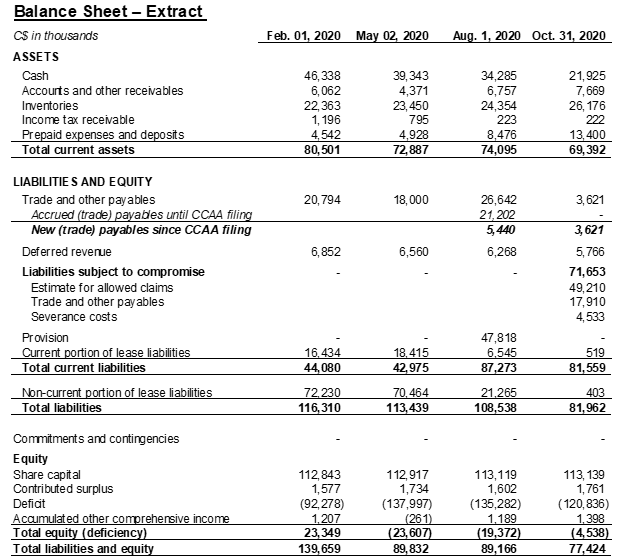

As there seems to be a wrong understanding about DavidsTea’s current cash position and its recent operating cash flow, I want to shed some light on its major balance sheet items.

Source:Quarterly reportsin 2020 of DavidsTea

As shown in the table above, the decrease in the cash balance of $12.3 million in the third quarter mainly results from an intentional increase in net working capital to be in a good position to meet the high demand in the seasonally strong fourth quarter. It is worth noting that the significant increase in “Prepaid expenses and deposits” over the last 6 months stems from the fact that DavidsTea had to make vendor deposits for both services and inventory-related purchases during the CCAA proceeding. By comparing this figure with the respective amount in the first quarter, it becomes clear that approx. $9 million of additional cash is currently sitting in this balance sheet item.

As of October 31, 2020, DavidsTea recorded lease liabilities for its headquarters, warehouse and reopened 18 stores of $0.9 million. In my view, this clearly demonstrates the substantially more favorable lease terms for its real estate as a result of the renegotiation with its landlords.

...

This leaves us with an annual EBITDA after lease payments of approx. $18.6 million - an upward revision of around $6 million compared to my last forecast - with an EBITDA margin of 14.9% in DavidsTea’s transition year. This significant upward revision mainly results from the first-time recognition of the new brick-and-mortar business in my updated financial model. Its recent financials suggest that I have significantly underestimated the sales and EBITDA potential of these 18 stores and overestimated the cannibalization effect on the e-commerce and wholesale sales channels.

One concluding remark as I think it went unnoticed by most shareholders: Pursuant to the provisions of the CCAA proceedings, DavidsTea's management - with the assistance of its monitor PricewaterhouseCoopers (PwC) - must prepare cash flow projections on a weekly basis.

According to the last monitor’s report, the company topped its cash flow

target by $6 million for the 14-week period that ended December 5, 2020, as retail, e-commerce, and wholesale demand was higher than anticipated. As a third of this period falls in the fourth quarter, we can be quite confident that DavidsTea can achieve my EBITDA forecast for the last quarter.

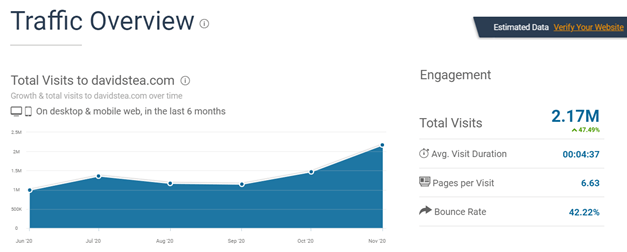

Source: Screenshot fromSimilarWeb

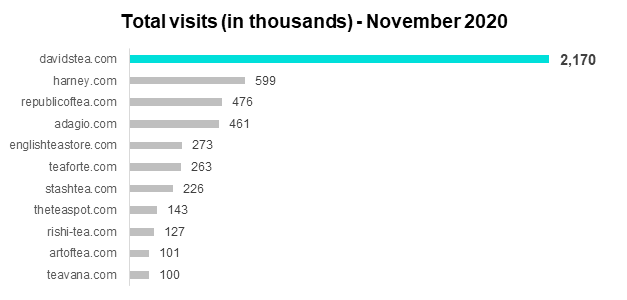

In addition, DavidsTea was ranked the fourth most visited grocery website in Canada in the month of November. Addressing the competitive landscape, SimilarWeb also lists its main online competitors selling all sorts of tea varieties and tea accessories. Based on my analysis of the respective monthly site visits, it’s fair to say that DavidsTea is doing quite well compared to these niche online tea vendors.

Source: Data provided by SimilarWeb

DavidsTea should be in a good position to settle all its claims of its former landlords and other creditors over the next two years without any dilutive measures for current shareholders. Thus, I think shareholders’ fears of a potential significant dilution as a result of the CCAA proceeding are largely unfounded (as management stated a couple of times before).

In the most recent monitor’s report, we also received a first indication regarding the envisaged timeline for the remaining steps in the restructuring proceeding:

Against the background of a potential settlement payment in the first quarter of 2021, the

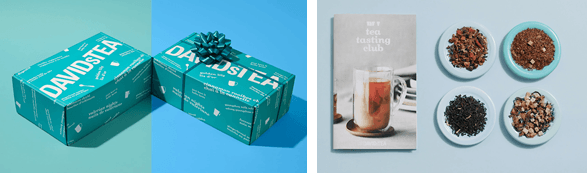

recent launch of its first seasonal subscription box called the “Tea Tasting Club” received too little attention. For a single purchase of

US$140, subscribers receive four boxes (each featuring up to eight exclusive blends of seasonal teas), gain access to curated content, and can participate in an online member-only community. This new initiative provides a couple of benefits but first and foremost, I expect significant incremental cash inflows in the months leading up to the potential settlement deal with its landlords. This should substantially strengthen DavidsTea’s negotiation position vis-à-vis its creditors as it gives room for a higher initial down payment of the total settlement amount. The appeal of a subscription service lies in the fact that the company receives the full annual cash amount before it has to deliver even a single product to its customers (the resulting deferred revenue will be recognized proportionally as revenue on the income statement over the four quarters of the fiscal year).

Source: WebsiteDavidsTea

The recently launched subscription box is apparently very well received as it has already been featured as the

winner of the category“Best in Tea” by the well-known magazine Food & Wine.

Valuation update

Assuming no significant change in net working capital and minor future CapEx requirements as a result of the new business model, my financial model projects a pro-forma adjusted annual free cash flow (FCF) of $18.5 million for the current financial year. Given the strong growth trajectory of its e-commerce and wholesale channels, DavidsTea should be granted a FCF multiple of at least 15 times (same as in my previous article), resulting in an enterprise value of $278 million. Based on the company's current cash balance (incl. cash equivalents) and my assumed payments as a result of the current restructuring proceeding, my price target has been lifted from 4.60 US$/share

to around 7.60 US$/share,

In addition, the recently announced

change in the management team should also be viewed favorably by the market. I think the fact that the company was run by a nearly 90-year-old interim CEO for more than two years was a major drag on the stock performance, even though the fatal decision of a massive store expansion was made by his predecessor. In addition, the current CFO Frank Zitella will step down from his position once his successor has been found and focus only on the company’s operations as COO in the future. I welcome the decision to promote his daughter

Sarah Segal to the new CEO for two reasons. First, as a former head of product development and founding manager of an e-commerce candy shop, she may combine her in-depth knowledge of DavidsTea’s product portfolio with a new leadership style and innovative fresh ideas (for example, I give her substantial credit for the launch of the seasonal subscription box). Secondly, in my opinion, the decision to appoint the daughter of the former CEO still owning around 46% of the company again demonstrates their confidence to come to terms with its creditors and emerge from the present restructuring proceeding relatively unscathed without much inherited burdens.

Conclusion

Despite the recent rally in DavidsTea’s share price, the two main catalysts are still in place that have the potential to drive its valuation substantially higher: so far, the market still questions its arguably significant earnings potential after the restructuring process as well as the fact that it can exit the CCAA procedure without any dilutive impact for current shareholders. If these doubts can be resolved, we should see a significant revaluation of the stock price over the coming months.

Whole art here-

https://seekingalpha.com/article/4401213-davidstea-dont-to-read-tea-leaves-anymore