I did my sneaky trick (using Chrome) and managed to grab this idea from Seeking Alpha-

First Julian Assange... now Stoney.

Negative Enterprise Value: Is Wall Street Paying You To Buy Perion Network?

Negative Enterprise Value: Is Wall Street Paying You To Buy Perion Network?

Sep. 01, 2024 9:32 AM ET

Perion Network Ltd. (PERI) StockMSFT,

MSFT:CA5 Comments

Paul Franke

Paul Franke

24.53K Followers

Summary

- Perion Network is very undervalued, trading near its net cash level of $400 million, offering significant upside in a business turnaround.

- Despite recent operational challenges and -70% share selloff, the company runs several units growing at a fast clip.

- Technical trading indicators suggest a potential price bounce, with targets between $12 and $22 if sales stabilize and cash levels increase.

- Risks include the potential for an expansion in operating losses and/or poor cash management, but the risk-reward setup currently favors bulls.

Van accepts Stoney into his stock and option training program. © Getty Images 2021

One of the worst stocks to own over the last 12 months (still earning a profit) traded in the U.S. has been

Perion Network Ltd. (NASDAQ:

PERI), based in Israel. The company focuses on digital marketing initiatives, alongside other operations matching supply/demand for the online world.

Unfortunately for existing shareholders, the company has been bombarded by a number of operating issues, with one unit forced to close and others suffering from a list of reasons.

Sentiment has gotten so bad on Wall Street, Perion is now priced at roughly the level of net cash held of $400 million. With an equity market capitalization hovering just below this number, you can now theoretically buy the business and all future profits for FREE. In effect, you are exchanging cash in your brokerage account for cash on Perion's balance sheet when you buy shares.

So, depending on how, when, and if the operating business begins to grow again, or what is done with the large cash stash to increase shareholder worth, the quote could quickly reverse higher the remainder of 2024 or languish under $10 over the next 12 months.

Since a similar pricing/valuation relationship has occurred two other times over the last 20 years, with one terrific buy opportunity and the other a nothingburger, readers will have to decide for themselves whether buying a position makes sense for their individual portfolio goals and risk tolerances.

I personally find enough positives to put a

Buy rating on the stock, anticipating some sort of rebound in price to $12 or even $15 could be approaching (good for a sizable percentage gain from $8 presently). With massive sell trading volume and logical excuses to run away from this name, today's existing shareholder base is likely of the very strongest kind. What this means is any good news or better-than-expected operating gains by the company could support a large imbalance of share demand vs. supply. Simple economic theory teaches us if buyers outnumber sellers 2:1 or 3:1, price will have to jump to find new supply for transactions.

Let's review some of the pro and con arguments for Perion ownership.

The Problem Child

Initially, the stock was hit hard by the decision by

Microsoft (

MSFT) to change how it pays Perion as a function of

Bing search revenue. Then, a decision was made to eliminate all identifiable MFAs from searches (clickbait-type websites nicknamed

Made For Advertising), which included a unit of Perion accounting for 5% of revenues, according to management. With the bad press and insinuation of shady practices, Perion immediately shut down this unit. You can read more on the situation in an excellent article by analyst

Henrik Alex here.

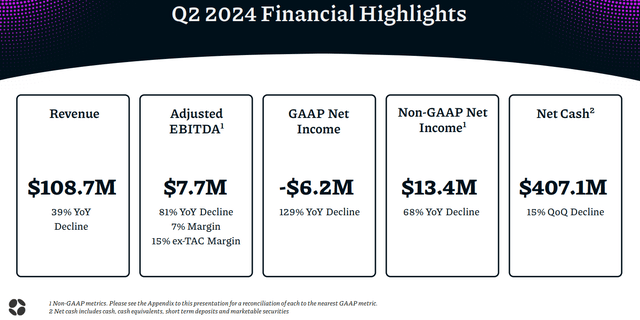

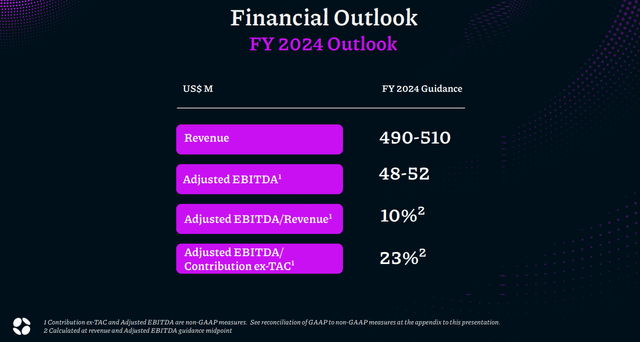

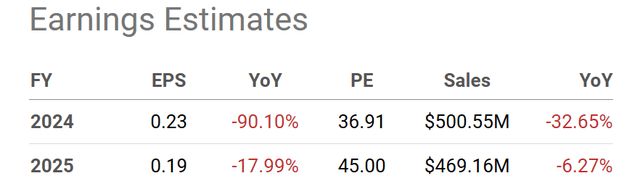

Combined with a slowdown in its AdTech business overall, the hit to the company's reputation has led to a large downgrade in guidance by management for the rest of 2024 and 2025, alongside a monster -70% share selloff from August 2023.

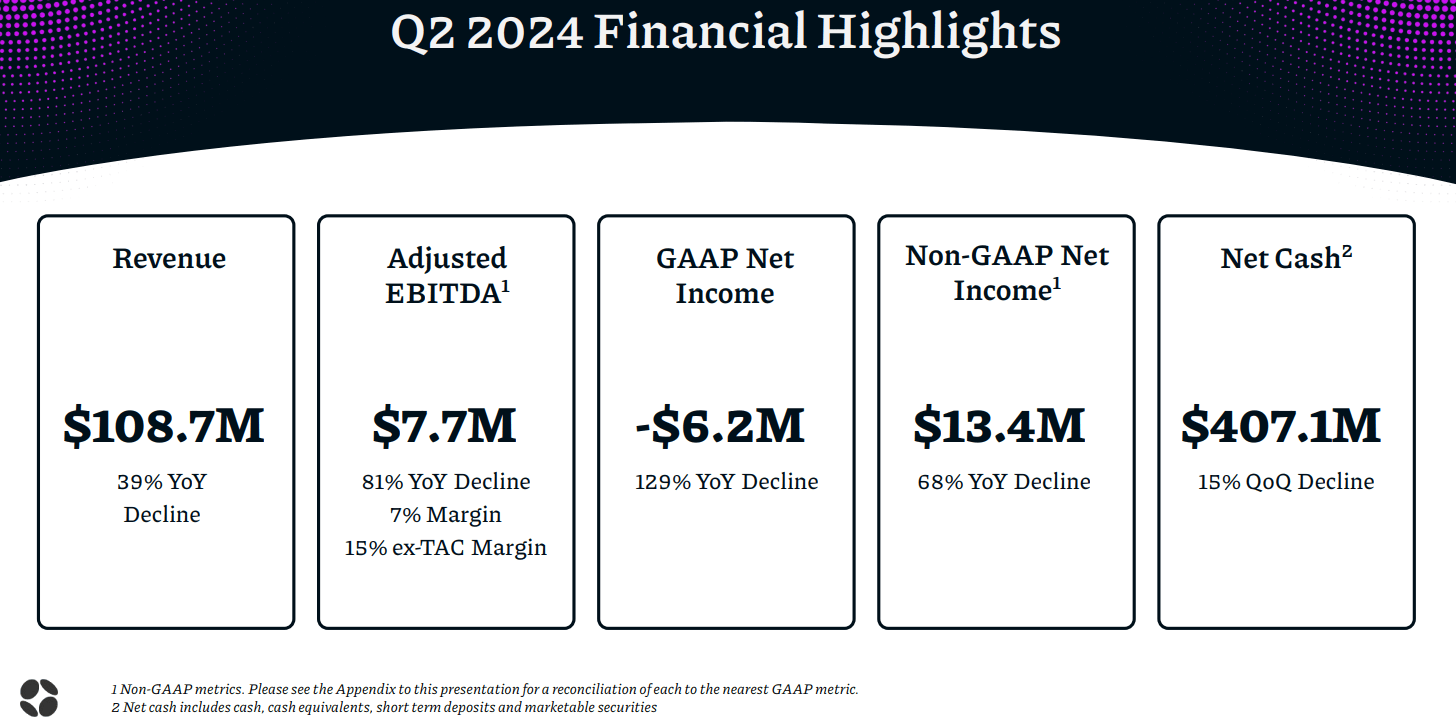

You can review the disaster for operating performance below during 2024, with little relief expected in 2025 by analysts.

Perion Network - Q2 2024 Earnings Presentation

Perion Network - Q2 2024 Earnings Presentation

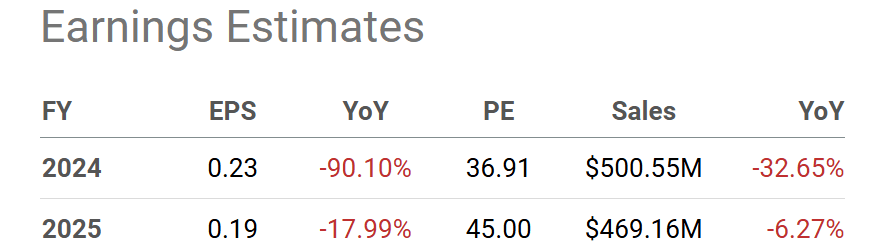

Seeking Alpha Table - Perion Network, Analyst Estimates for 2024-25, Made August 30th, 2024

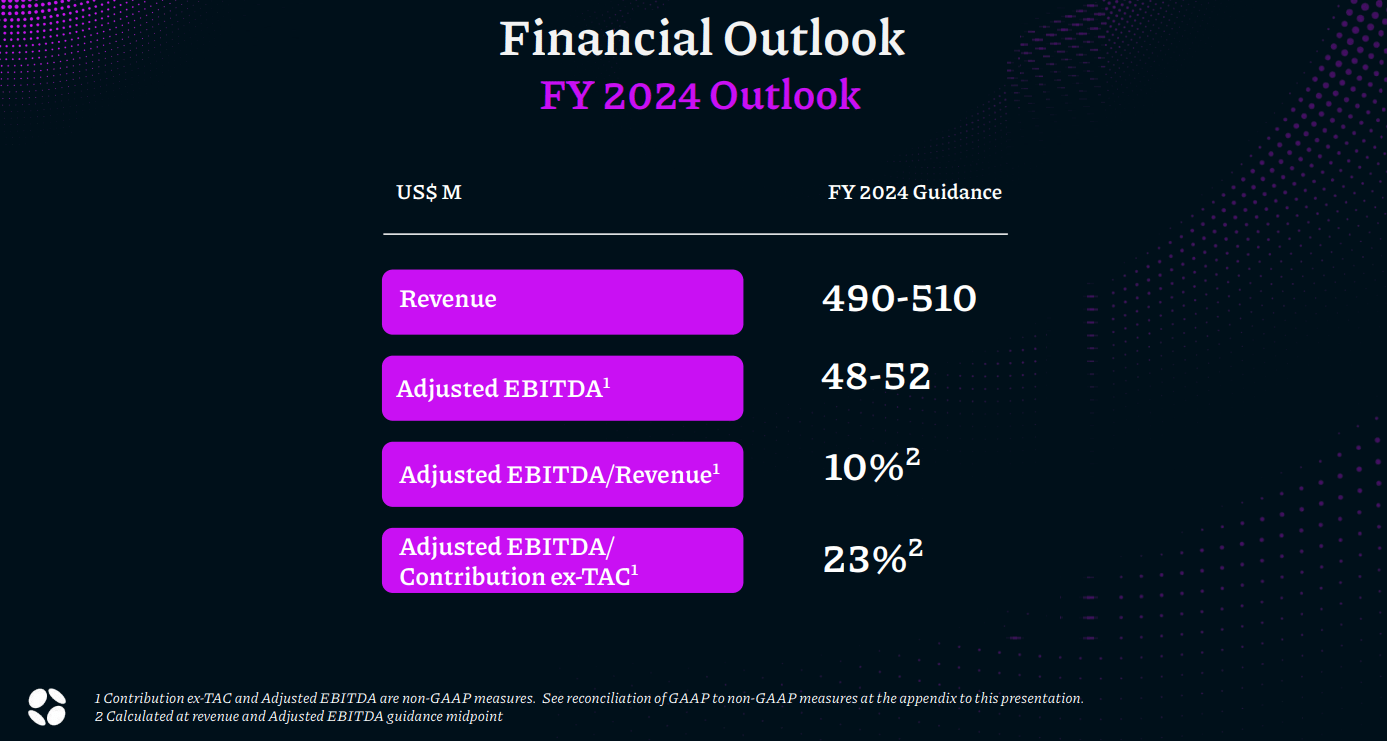

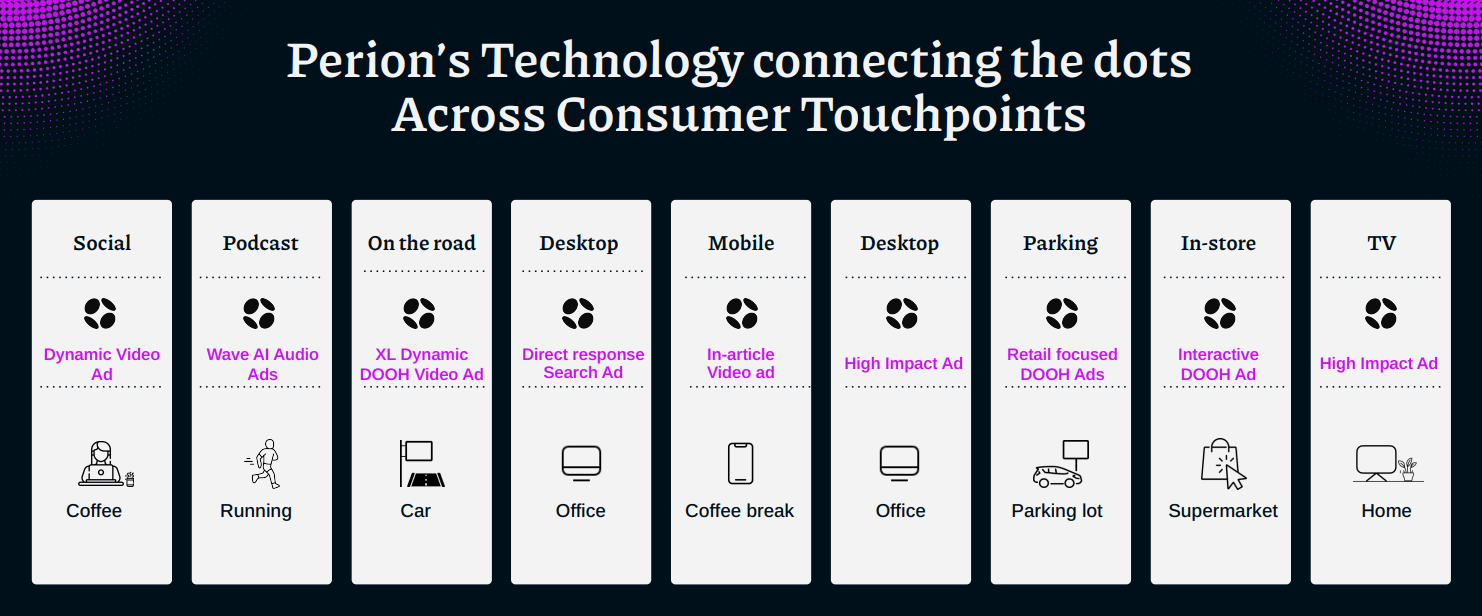

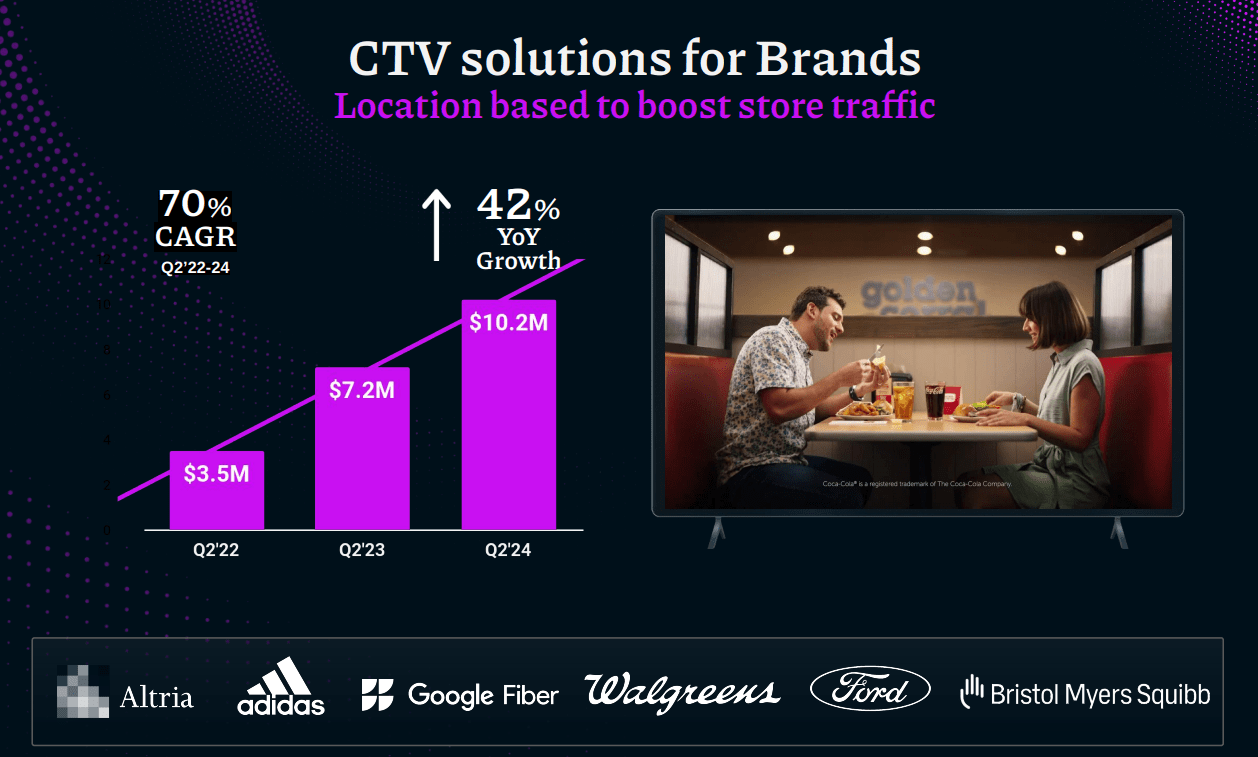

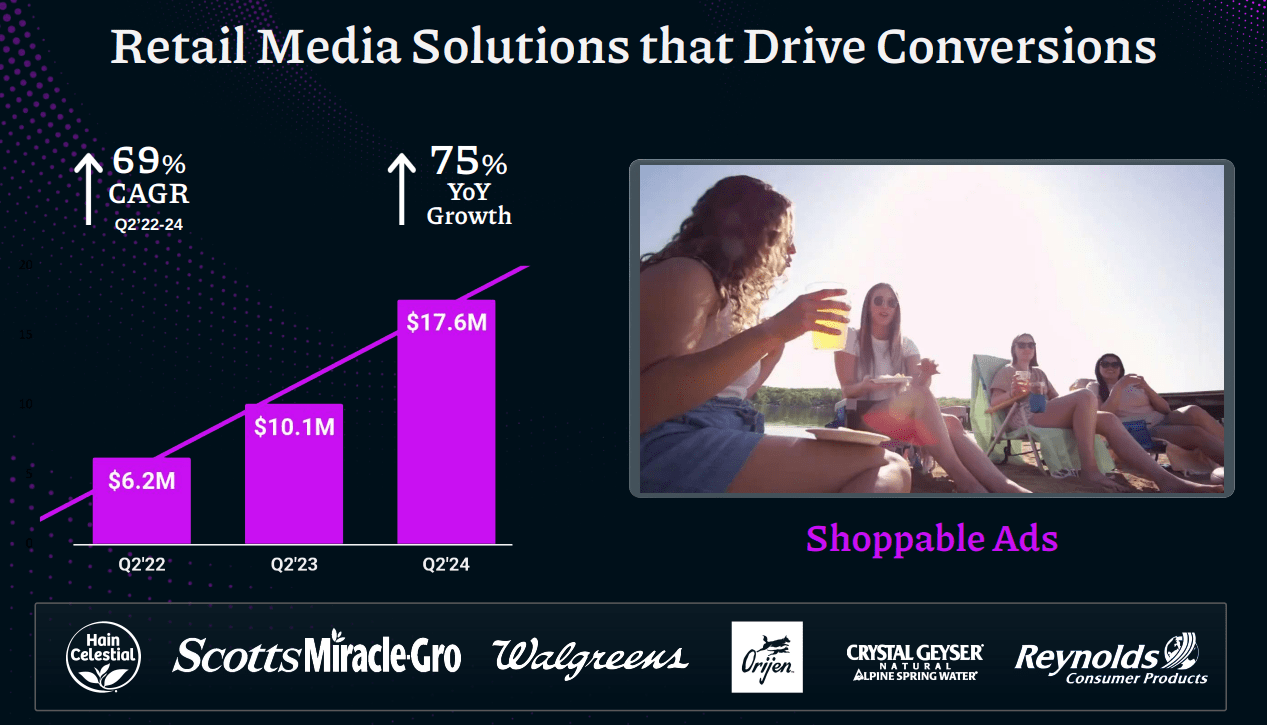

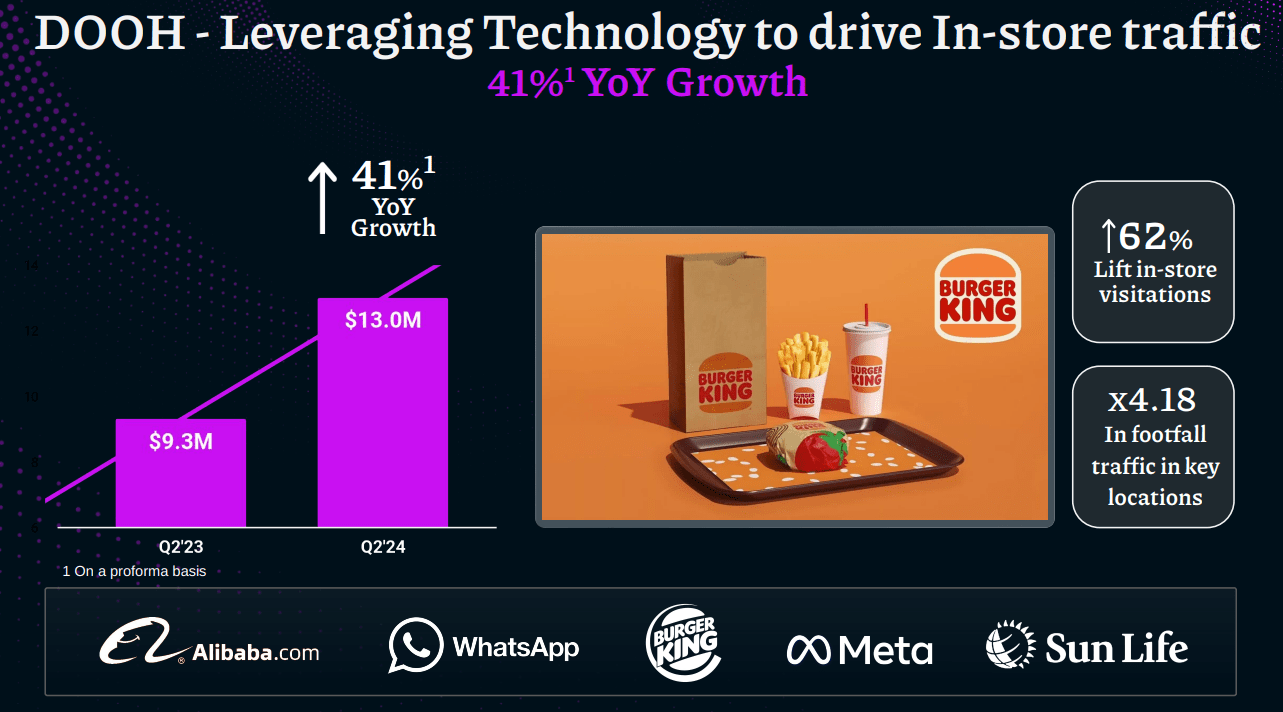

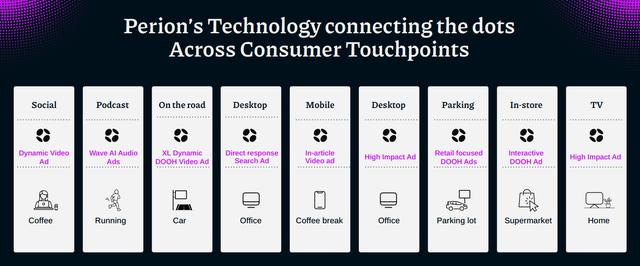

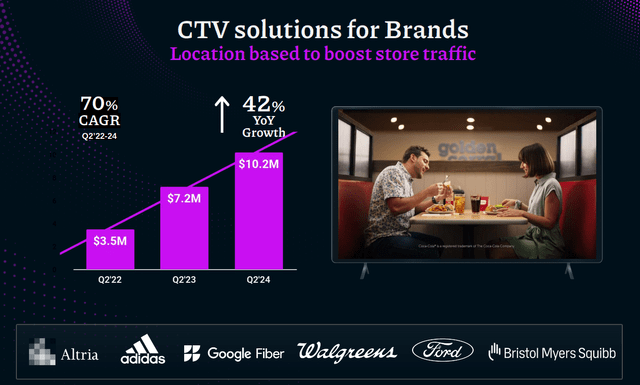

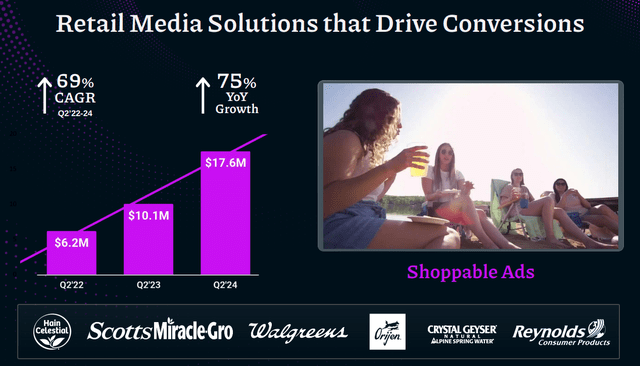

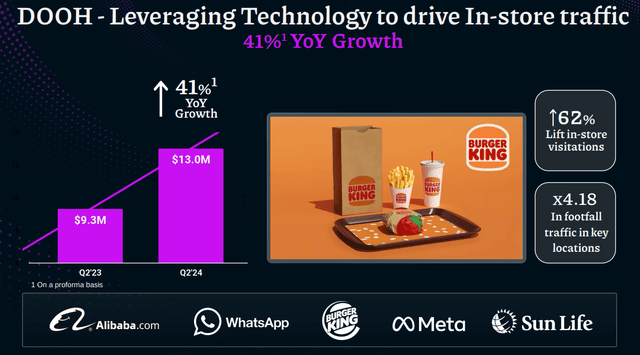

That's not to say the company cannot recover. Several of its divisions for ad-based tracking are growing rapidly in 2024. I have taken some slides from its

Q2 2024 Earnings Presentation to illustrate this reality below.

Perion Network - Q2 2024 Earnings Presentation

Perion Network - Q2 2024 Earnings Presentation

Perion Network - Q2 2024 Earnings Presentation

Perion Network - Q2 2024 Earnings Presentation

The Undervaluation Story

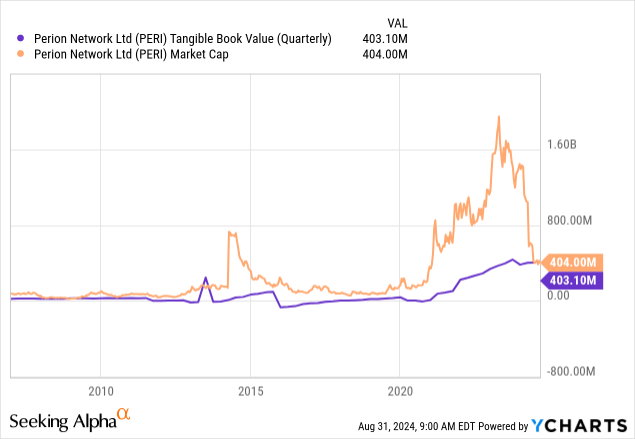

Below is a basic chart comparing tangible accounting book value for Perion, against the equity market capitalization, using prevailing stock pricing times outstanding share counts. Notice price has almost always traded above tangible book value, looking back to 2006.

YCharts - Perion Network, Equity Market Cap vs. Tangible BV, Since 2006

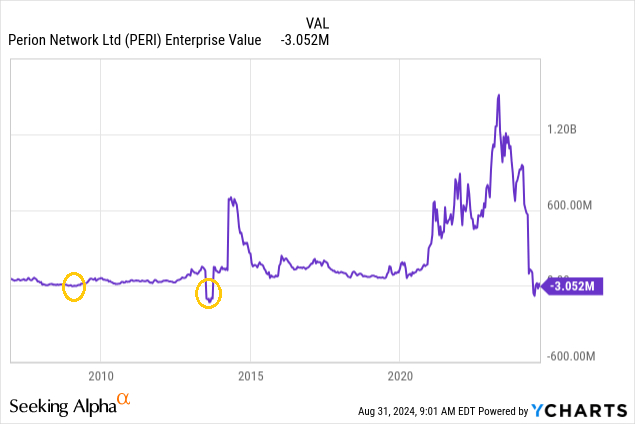

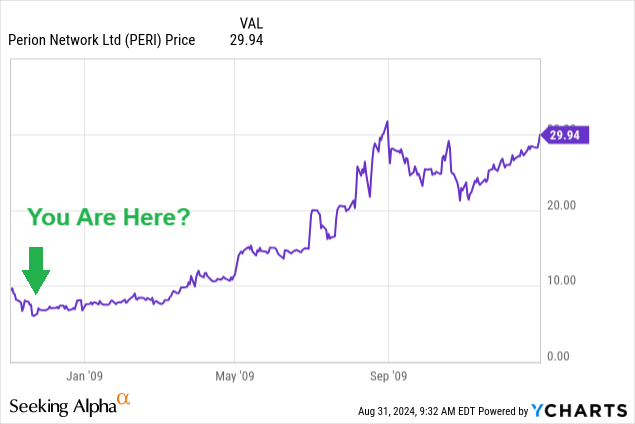

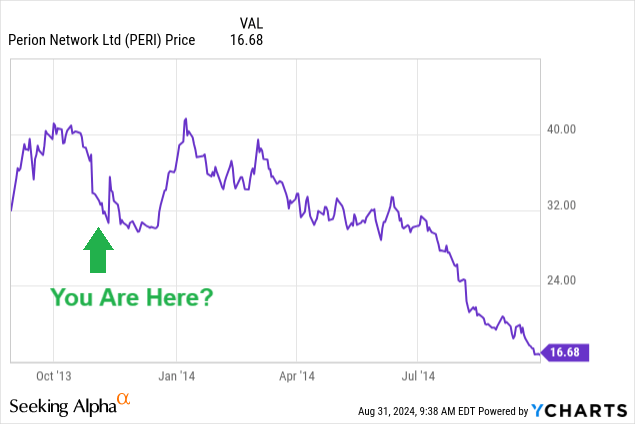

Even more interesting is the enterprise value calculation. The average U.S. equity almost never trades at a "negative" EV number (equity value + all debt - cash holdings), yet this is the third time over twenty years for Perion. I have circled the previous two instances in gold below (late 2008 and late 2013).

YCharts - Perion Network, Enterprise Value, Since 2006, Author Reference Points

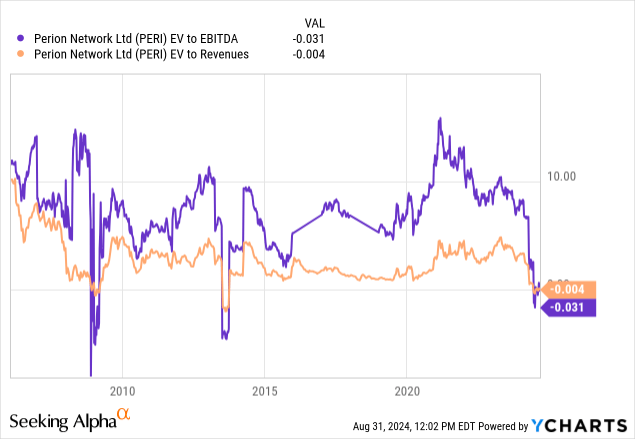

You can really see the negative EV to EBITDA and Revenue numbers on a log scale from YCharts below. You are essentially buying the company for free if earnings, cash flow, and overall cash levels rise in the future. Typically, negative enterprise value setups are reserved for businesses reporting large income losses, with similar results expected indefinitely.

YCharts - Perion Network, EV to Trailing EBITDA & Revenues, Since 2006

How did the company's stock respond after the previous two EV wipeouts below zero? I have charted the outcomes below. The first occurred in late 2008 during the Great Recession. This situation turned out to be a terrific buying opportunity with price rising from $7 to $31 over the following nine months! However, example two in late 2013 didn't work out as well. Prices around $32 would witness a minor jump to $41 months later, followed by price sliding all the way to $16 later in 2014.

YCharts - Perion Network, Daily Price Change, Nov 2008 to Dec 2009

YCharts - Perion Network, Daily Price Change, Sept 2013 to Sept 2014

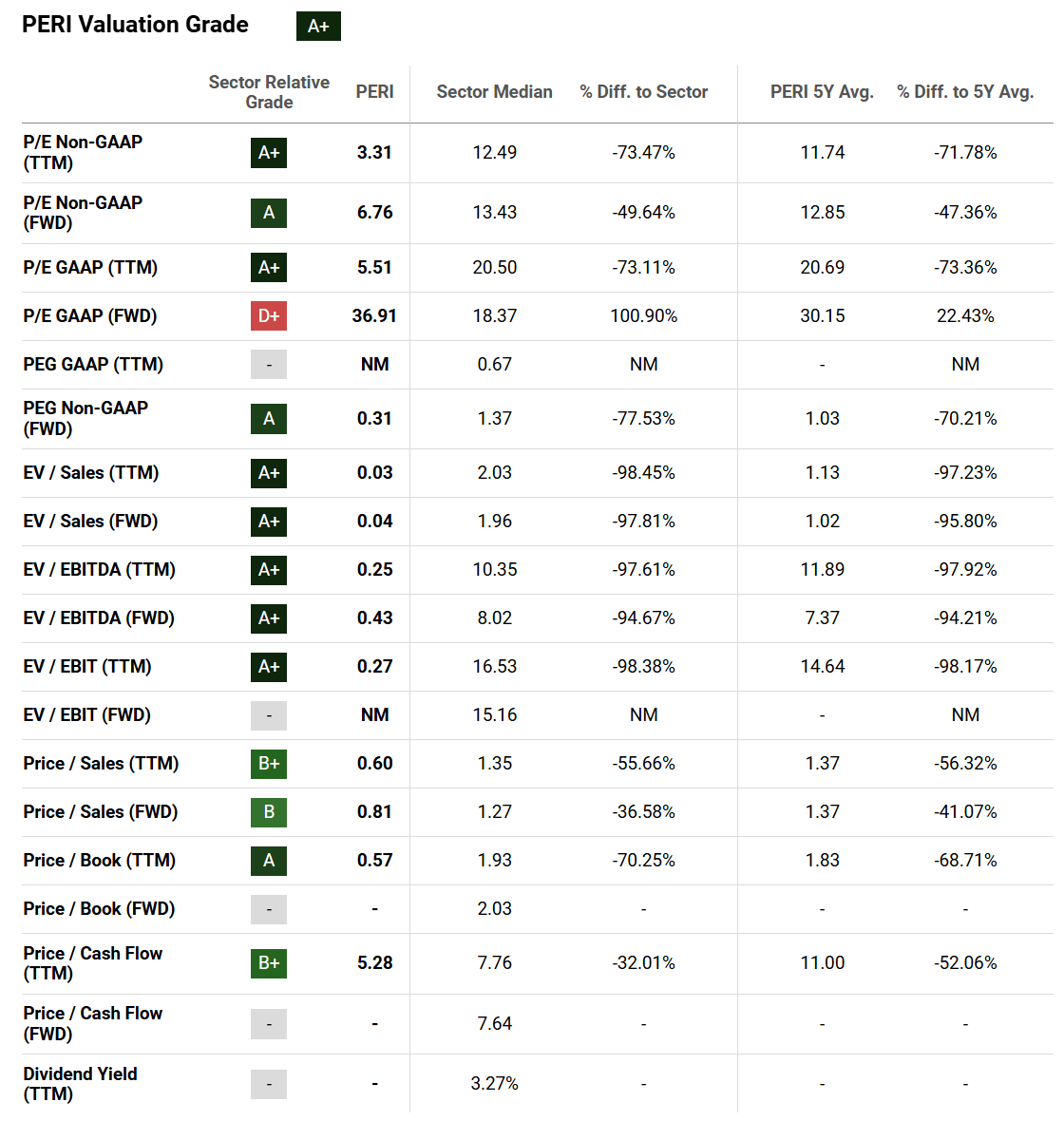

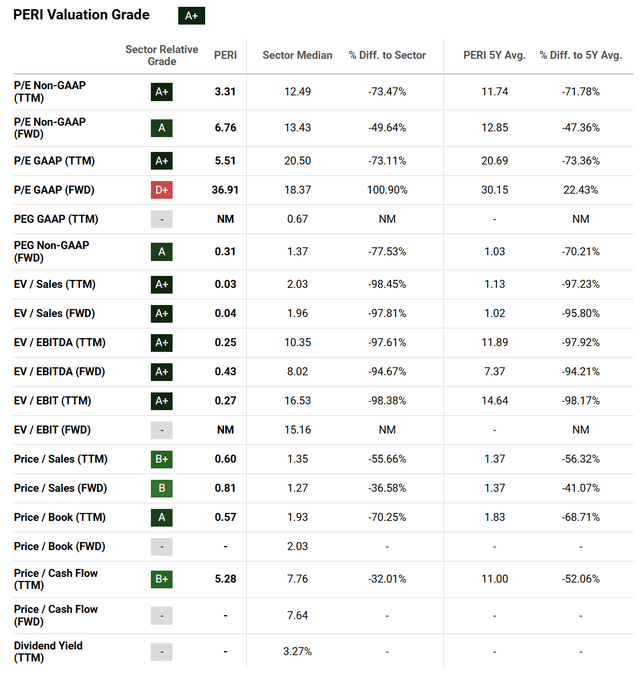

Seeking Alpha's computer-scoring system gives Perion an "A+"

Quant Valuation Grade today, largely a function of the ultra-low EV calculation. Bullish price to book value comparisons are also part of SA's equation. Plus, earnings from 6-12 months ago are still being counted vs. a rather bleak immediate income prediction by management. Still, if sales and earnings hold up in 2025, $8 for the share quote could be an amazing bargain in hindsight.

Seeking Alpha Table - Perion Network, Quant Valuation Grade, August 30th, 2024

Final Thoughts

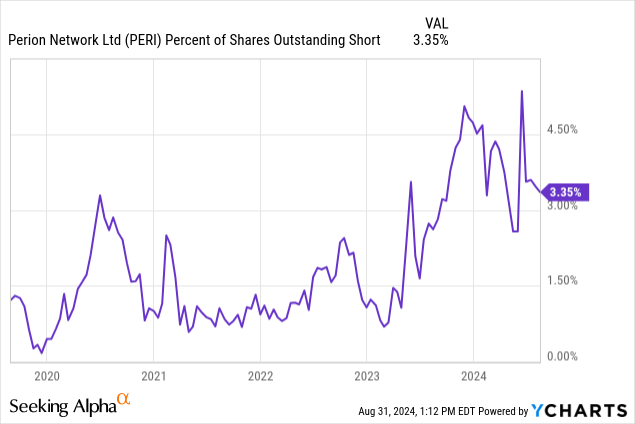

The bearish trader, short interest position is higher than a few years ago, but 3% of outstanding counts is not an amazing size. There is not a massive short-covering pool to propel the stock well beyond $15 or $20 anytime soon. I will add, I don't believe shorting the stock at $8 near net-cash levels makes any rational sense today.

YCharts - Perion Network, Short Interest, 5 Years

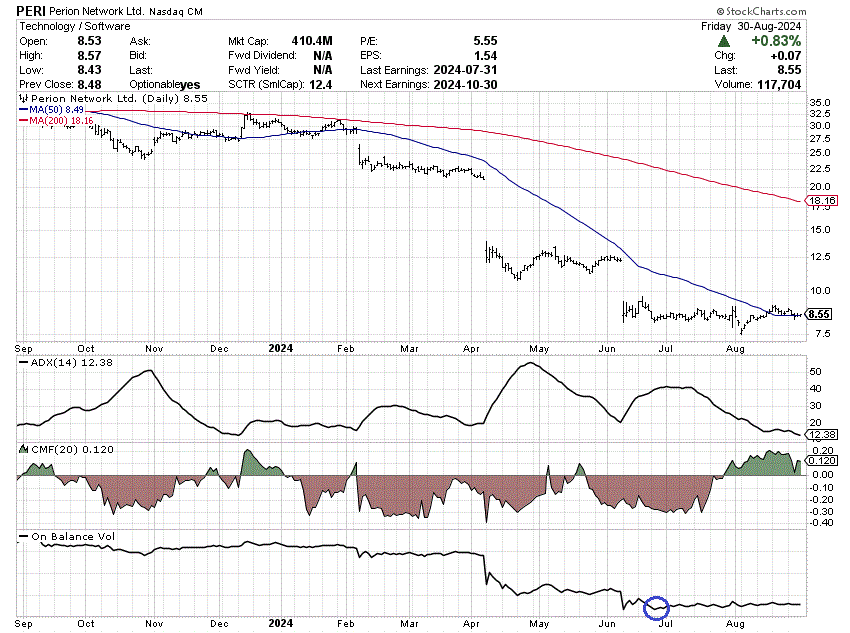

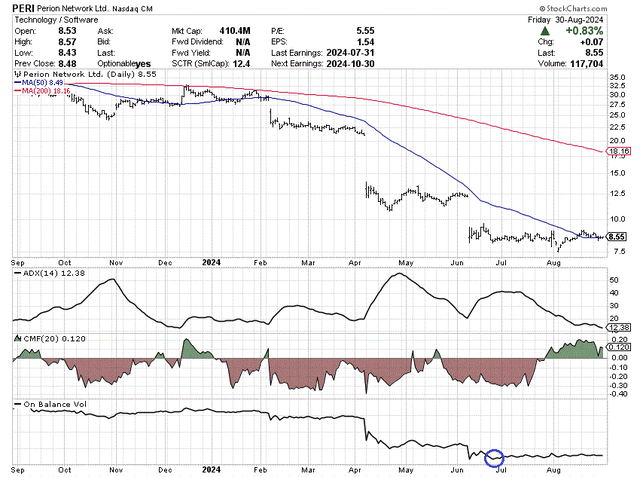

The trigger for me writing this story revolves around the chart pattern. Perion's price has been trading above its 50-day moving average on-and-off-again for a few weeks. Often this action will encourage buyers to step in and sellers to raise limit-order prices. So, the timing of a bounce off its lows with the potential for sizable retracement of the major losses since February may be close at hand.

Other positives include a much lower

Average Directional Index and green 20-day

Chaikin Money Flow readings over the last month. Both may be signaling the worst of the selling has run its course. In addition,

On Balance Volume numbers bottomed in late June (circled in blue below).

StockCharts.com - Perion Network, 12 Months of Daily Price & Volume Changes, Author Reference Point

What are risks owning Perion with a negative enterprise value? My easy answer is substantial operating losses cannot appear. If the company continues to see sales implode and income turns sharply negative, cash holdings will move into reverse.

Management could also do something stupid with the $400 million in cash, like acquire a similar company that is not earning any money. Exchanging $20+ million in cash investment yield annually for something worse would encourage me to sell any future Perion position and run for the hills.

In terms of technical upside targets, I am thinking a refill of the price gaps around $12 and then $14-22 are possibilities, given sales stabilize and the company can build cash levels from here. Rebounding to $16-17 would generate a rough double on your investment capital (+100%), when purchasing shares around $8.

And, if things don't turn around in 2025, slow cash burn should allow investors to get out with $5 or $6 per share. As a consequence, I feel the risk/reward equation is tilted in favor of bulls. I rate Perion Network shares a

Buy, and will try to add a stake next week to my diversified portfolio. If quick trading profits appear before the end of the year, I will likely take some if not all of money off the table in this name.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.