Cheniere Energy price target raised to $183 from $169 at JPMorgan 06:12 LNG JPMorgan analyst Jeremy Tonet raised the firm's price target on Cheniere Energy to $183 from $169 and keeps an Overweight rating on the shares. As we exit the Northern Hemisphere's winter season, benchmark liquified natural gas prices in Europe and Asia remain robust, with spot netbacks still hovering near $15/mmbtu or higher, Tonet tells investors in a research note.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

GBA Presents: THE BARE ESSENTIALS

- Thread starter stonedinvestor

- Start date

What's that company that is planning that LNG facility in TX? You posted about it. It had a picture. A rendering.Cheniere Energy price target raised to $183 from $169 at JPMorgan 06:12 LNG JPMorgan analyst Jeremy Tonet raised the firm's price target on Cheniere Energy to $183 from $169 and keeps an Overweight rating on the shares. As we exit the Northern Hemisphere's winter season, benchmark liquified natural gas prices in Europe and Asia remain robust, with spot netbacks still hovering near $15/mmbtu or higher, Tonet tells investors in a research note.

--Sono Motors 10M share Secondary priced at $4.00 06:23 SEV

--Elon Musk sells $4B in Tesla stock to fund Twitter takeover

Van & Cathie Wood doubles down on Teladoc after selloff

Apr. 28, 2022 10:54 PM ETTeladoc Health, Inc. (TDOC)ARKK,ARKW,ARKG,ARKF

--Elon Musk sells $4B in Tesla stock to fund Twitter takeover

Van & Cathie Wood doubles down on Teladoc after selloff

Apr. 28, 2022 10:54 PM ETTeladoc Health, Inc. (TDOC)ARKK,ARKW,ARKG,ARKF

- Notable fund manager, Cathie Wood, has further increased the exposure of her ETFs to Teladoc Health (NYSE:TDOC) after the telehealth company witnessed a sharp selloff on Thursday in reaction to its lower-than-expected1Q 2022 financials.

- After a ~40% drop during regular trading, Teladoc (TDOC) shares continued to fall in the post-market even as Cathie Wood-run ETFs added more than 600K company shares. Van added 75.

Phillips 66 Non-GAAP EPS of $1.32 beats by $0.05

Apr. 29, 2022 7:02 AM ETPhillips 66 (PSX)

Apr. 29, 2022 7:02 AM ETPhillips 66 (PSX)

- Phillips 66press release(NYSE:PSX): Q1 Non-GAAP EPS of $1.32beats by $0.05.

- Shares+2%PM.

- “In the first quarter, we generated strong cash flow in a volatile market environment with seasonally lower margins across our businesses,” said Greg Garland, Chairman and CEO ofPhillips 66. “While first-quarter results were lower quarter-on-quarter, we saw substantially improved financial results from our operations in March and expect continued strong performance in the second quarter. We believe current market conditions will allow us to increase shareholder returns by restarting share repurchases and increasing the dividend. In April, we repaid $1.45 billion of debt and plan to repay additional debt this year.<---------

Bloomin' Brands Non-GAAP EPS of $0.80 beats by $0.06, revenue of $1.14B beats by $10M

Apr. 29, 2022 7:06 AM ET Bloomin' Brands, Inc. (BLMN)

Innate Pharma stock rises on upcoming $50M from partner AstraZeneca, as dosing begins in lung cancer study...

___________GO TIME ON CHINA TECH________________

BYDDF- (today)

Some other China Tech idea.....? Baba/..............................

Apr. 29, 2022 7:06 AM ET Bloomin' Brands, Inc. (BLMN)

- Bloomin' Brandspress release(NASDAQ:BLMN): Q1 Non-GAAP EPS of $0.80beats by $0.06.

- Revenue of $1.14B (+15.4% Y/Y)beats by $10M.

- Q3 outlook: Total revenues of $1.1B to $1.13B vs. consensus of $1.08B; GAAP diluted EPS of $0.55 to $0.59; Adjusted diluted EPS of $0.60 to $0.65 vs. consensus of $0.60.

Innate Pharma stock rises on upcoming $50M from partner AstraZeneca, as dosing begins in lung cancer study...

___________GO TIME ON CHINA TECH________________

BYDDF- (today)

Some other China Tech idea.....? Baba/..............................

I am worried about a sprint higher in oil. Worried sick.

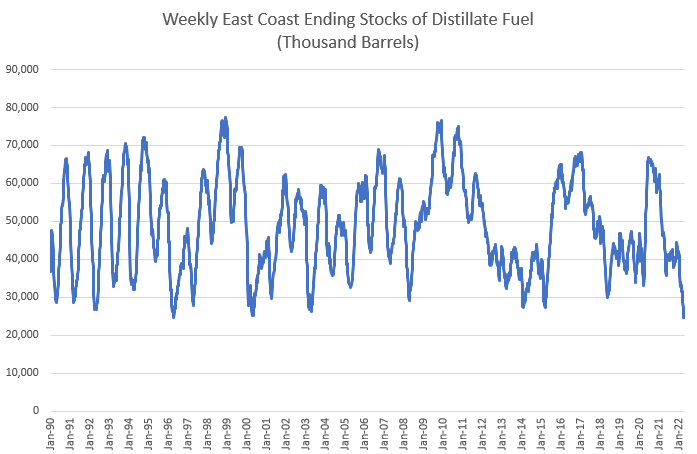

Inventories of diesel and jet fuel in the Northeast are at levels not seen since 1996, and on the precipice of hitting all time lows. And this at a time when international travel has been curtailed by pandemic-related restrictions:

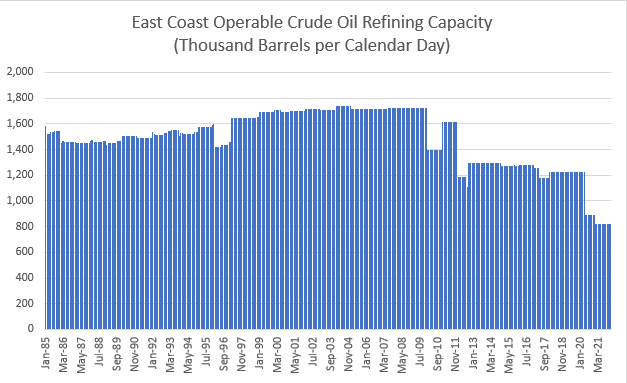

The low inventory levels are showing up in price. Diesel margins in New York Harbor currently sit above $100/b. Margins that have historically averaged less than $20/b. Jet fuel margins briefly hit $200/b earlier this month, or ~10x normal levels. While refinery utilization in April has been elevated by historic standards, years of closures and bio-refining conversions have reduced capacity in the Northeast by ~50%:

Increased demand for fuel in the Northeast has historically been met by incremental supply of refined product from the Gulf Coast. Product that has traveled up the Eastern Seaboard through the Colonial Pipeline. Recall 2021, when a ransomware attack shut the Colonial Pipeline, creating gasoline shortages throughout the region.

COULD THIS BE THE TARGET AGAIN-!

Just today, PBF's (PBF) CEO said that increased exports, largely out of the Gulf Coast to Europe, have reduced oil product volumes flowing through the Colonial Pipeline. The pipeline has historically been a bottleneck for supply, with producers being allocated only a portion of desired pipeline capacity. Thursday PBF (PBF) CEO Nimbley said, "Colonial pipeline line 2 has not been allocated. It traditionally is always allocated."

With Russian energy sanctions set to take effect in coming months, it appears that self-sanctioning has already reduced oil product exports. Between the US and Europe, around 2mb/d of refining capacity has been closed since 2019, with most refineries converted to terminals or bio-diesel plants. Given restrictions on Russian exports, China is the only supplier currently able to increase refined product exports. In March, China halted oil product exports entirely.<----- Saving for themselves.

With oil demand expected to reach new highs in 2022, a shortage of refining capacity could impact consumers everywhere. At least consumers outside of China and Russia. The Northeast is not uniquely at risk of shortage, as consumers can simply out-bid Europeans to reduce exports and pull additional product through the Colonial pipeline. But it's just these sorts of effective bidding wars that are increasing oil product prices<-- self fulfilling.

For investors, the dynamic creates unique challenges. Restricted crude oil exports from Russia have driven traders into the upstream sector. However, a refining capacity bottleneck could lift oil product prices, while restricting demand for crude oil (USO). Shifting the "economics of the barrel" to refiners for the first time in recent history. And this appears to be what is happening. Currently, oil prices are ~$40 below all time highs; however, diesel prices are almost $10 above any prior period. The dynamic would suggest that pure-play oil refiners like Valero(VLO), Philips (PSX), Par Pacific (PARR), Marathon (MPC) and others could benefit from evolving energy markets.

VLO-

PSX-

PARR-

MPC-

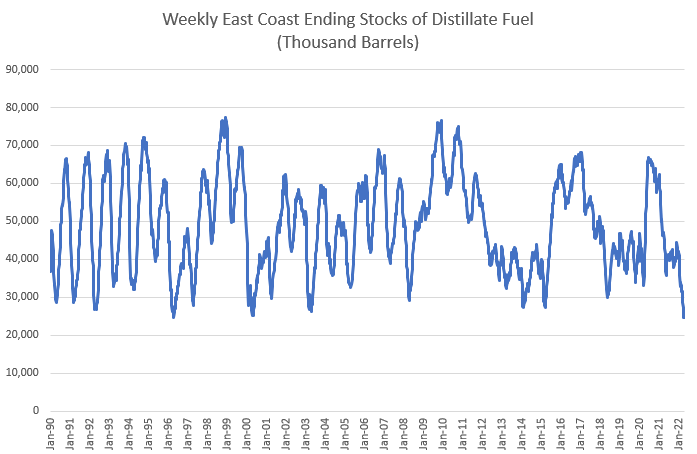

Inventories of diesel and jet fuel in the Northeast are at levels not seen since 1996, and on the precipice of hitting all time lows. And this at a time when international travel has been curtailed by pandemic-related restrictions:

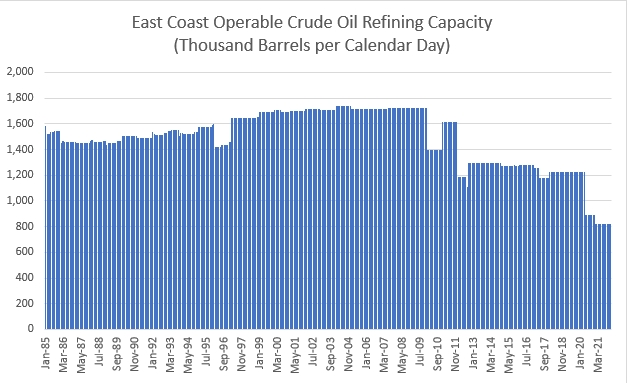

The low inventory levels are showing up in price. Diesel margins in New York Harbor currently sit above $100/b. Margins that have historically averaged less than $20/b. Jet fuel margins briefly hit $200/b earlier this month, or ~10x normal levels. While refinery utilization in April has been elevated by historic standards, years of closures and bio-refining conversions have reduced capacity in the Northeast by ~50%:

Increased demand for fuel in the Northeast has historically been met by incremental supply of refined product from the Gulf Coast. Product that has traveled up the Eastern Seaboard through the Colonial Pipeline. Recall 2021, when a ransomware attack shut the Colonial Pipeline, creating gasoline shortages throughout the region.

COULD THIS BE THE TARGET AGAIN-!

Just today, PBF's (PBF) CEO said that increased exports, largely out of the Gulf Coast to Europe, have reduced oil product volumes flowing through the Colonial Pipeline. The pipeline has historically been a bottleneck for supply, with producers being allocated only a portion of desired pipeline capacity. Thursday PBF (PBF) CEO Nimbley said, "Colonial pipeline line 2 has not been allocated. It traditionally is always allocated."

With Russian energy sanctions set to take effect in coming months, it appears that self-sanctioning has already reduced oil product exports. Between the US and Europe, around 2mb/d of refining capacity has been closed since 2019, with most refineries converted to terminals or bio-diesel plants. Given restrictions on Russian exports, China is the only supplier currently able to increase refined product exports. In March, China halted oil product exports entirely.<----- Saving for themselves.

With oil demand expected to reach new highs in 2022, a shortage of refining capacity could impact consumers everywhere. At least consumers outside of China and Russia. The Northeast is not uniquely at risk of shortage, as consumers can simply out-bid Europeans to reduce exports and pull additional product through the Colonial pipeline. But it's just these sorts of effective bidding wars that are increasing oil product prices<-- self fulfilling.

For investors, the dynamic creates unique challenges. Restricted crude oil exports from Russia have driven traders into the upstream sector. However, a refining capacity bottleneck could lift oil product prices, while restricting demand for crude oil (USO). Shifting the "economics of the barrel" to refiners for the first time in recent history. And this appears to be what is happening. Currently, oil prices are ~$40 below all time highs; however, diesel prices are almost $10 above any prior period. The dynamic would suggest that pure-play oil refiners like Valero(VLO), Philips (PSX), Par Pacific (PARR), Marathon (MPC) and others could benefit from evolving energy markets.

VLO-

PSX-

PARR-

MPC-

--Sono Motors 10M share Secondary priced at $4.00 06:23 SEV

Warren Buffett and VZ's 'Woodstock for Capitalists' a smaller affair after pandemic

1 / 3

Warren Buffett meets with VZ to discuss BYDDF and RH

BYDDF----> $28.93

RH-----> $353

LyondellBasell Non-GAAP EPS of $4.00 beats by $0.45, revenue of $13.16B beats by $490M

EQT may invest in U.S. LNG export facility to tap global markets, CEO says

Apr. 28, 2022 7:07 PM ETEQT Corporation (EQT)

CHUNYIP WONG/E+ via Getty Images

EQT Corp. (NYSE:EQT) said Thursday it may take an equity stake in a liquefied natural gas export project, as it seeks to capitalize on the booming global demand for LNG with Russian threats sending European gas prices swinging wildly.

"We are currently in discussions with LNG end-users across various geographies and are contemplating equity investment opportunities in LNG export facilities," CEO Toby Rice said in an earnings conference call.

Current U.S. Henry Hub natural gas prices are elevated from historical levels, but delivered LNG prices in Europe and Asia have surged ~3x higher than a year ago, and EQT would seek to capture the strong margins between domestic feedgas and higher spot prices for cargoes delivered to end-user markets.

"Our ultimate prize that we're looking for here at EQT is to get exposure to international markets," Rice said on the call. "One of the ways that we get more flexibility towards accessing those contracts is to take an investment in the LNG facility itself."

Longer-term supply agreements would allow EQT to directly benefit from higher gas prices overseas while reducing buyers' exposure to extreme volatility, the CEO said.

EQT shares gained 2.6% in Thursday's trading after the company missed Q1 earnings by a wide margin but raised full-year free cash flow guidance by 50%.

This has to be that stock... oh stoney where is the memory.... Damn it! Um these guys are building a big facility they just got some permits.... UGH!!! W.... W something.... F*!

EQT may invest in U.S. LNG export facility to tap global markets, CEO says

Apr. 28, 2022 7:07 PM ETEQT Corporation (EQT)

CHUNYIP WONG/E+ via Getty Images

EQT Corp. (NYSE:EQT) said Thursday it may take an equity stake in a liquefied natural gas export project, as it seeks to capitalize on the booming global demand for LNG with Russian threats sending European gas prices swinging wildly.

"We are currently in discussions with LNG end-users across various geographies and are contemplating equity investment opportunities in LNG export facilities," CEO Toby Rice said in an earnings conference call.

Current U.S. Henry Hub natural gas prices are elevated from historical levels, but delivered LNG prices in Europe and Asia have surged ~3x higher than a year ago, and EQT would seek to capture the strong margins between domestic feedgas and higher spot prices for cargoes delivered to end-user markets.

"Our ultimate prize that we're looking for here at EQT is to get exposure to international markets," Rice said on the call. "One of the ways that we get more flexibility towards accessing those contracts is to take an investment in the LNG facility itself."

Longer-term supply agreements would allow EQT to directly benefit from higher gas prices overseas while reducing buyers' exposure to extreme volatility, the CEO said.

EQT shares gained 2.6% in Thursday's trading after the company missed Q1 earnings by a wide margin but raised full-year free cash flow guidance by 50%.

This has to be that stock... oh stoney where is the memory.... Damn it! Um these guys are building a big facility they just got some permits.... UGH!!! W.... W something.... F*!

Ok Got it Thanks baron-

Telurian Inc. (TELL)<----------

6.16+0.15(+2.58%)

As of 01:03PM EDT

New Fortress Energy Inc. (NFE)<----------------

41.50-3.61(-8.00%)

As of 01:06PM EDT. Market open.

These are the two building out.... which one is the partner?

Telurian Inc. (TELL)<----------

6.16+0.15(+2.58%)

As of 01:03PM EDT

New Fortress Energy Inc. (NFE)<----------------

41.50-3.61(-8.00%)

As of 01:06PM EDT. Market open.

These are the two building out.... which one is the partner?

Who Owns Forest River RV? 5 Facts You Should Know (Explained)But that whole travel the USA and catch Covid everywhere- that's over. The infatuation with being a rambler not connected anywhere that's over. It's dead Van I have my ears to the ground. These folks are saving money now. Traveling is expensive. even in a junky RV-

Written by Mike Gilmour in RV Guide

Have you ever wondered who owns forest river RV? We´ve got you covered.

Forest River, Inc. is one of the largest producers of towable recreational vehicles (RVs), with 15 manufacturing facilities throughout the United States.

With a variety of products ranging from towable RVs to Park Models, Forest River has something that would fit almost any lifestyle.

From folding dinettes to flatscreen TVs and a fully equipped kitchen to a private bathroom and shower, each Forest River RV provides the comfort and convenience you need for an enjoyable outdoor experience.

So, who owns Forest River RV? Forest River RV Company is owned by Berkshire Hathaway.