- Oh Baby! I pulled off a swipe! Hard to explain,. I don't want to give away me secretes but if you go to a third entry portal you don't normally use (Chrome shhhhhhh) and you pretend you are your wife-- it asks? hit wife button and then you go to google and enter the heading for an article you are locked out of for an instant it shows up and if you are fast enough to drag and swipe and make the words blue and hit copy before the screen rolls up you actually gab alot of the article!!!!!

Sea Limited is showing constructive upside trading action and momentum, with a price breakout possibly in progress.

- The company operates in Southeast Asia and Latin America. Its main businesses are focused on e-commerce, mobile gaming, and digital payments.

- Sea Limited is transitioning to a self-funded growth strategy, with a strong balance sheet, improving profit margins, and its most attractive valuation ever.

With the overall U.S. equity market rising +15% to +20% since October, it is getting harder to find an honest bottoming pattern worthy of purchase for my portfolio. I am afraid a number of stocks that look like they are bottoming, areactually future "underperformers" experiencing some arbitrage buying as the general market zigzags higher (giving us a false impression of 2024's potential for positive returns).

One company that has popped onto my momentum sorts, showing incredibly constructive upside trading pressure, with little price movement as of yet, is

Sea Limited(NYSE:

SE). This company is based in Singapore, operating an online business model similar to

Alibaba(

BABA) in China or

Amazon(

AMZN) in America.

After a general recap of the business, this article will review the bullish technical trading setup, which I rate as excellent forlong-term buyers wanting to diversify out of the U.S. market.

The Business

The areas of the world served by Seal Limited include Southeast Asia (also abbreviated SEA) and the quickly growing Latin America online market. In order of importance and revenue generation,

Shopeeis a well-received e-commerce intermediary with 375 million registered users,

Garenafocuses on mobile gaming and digital entertainment with 544 million users, and

SeaMoneyis an accelerating-growth digital payments and financial services concern.

Company Website - Sea.com

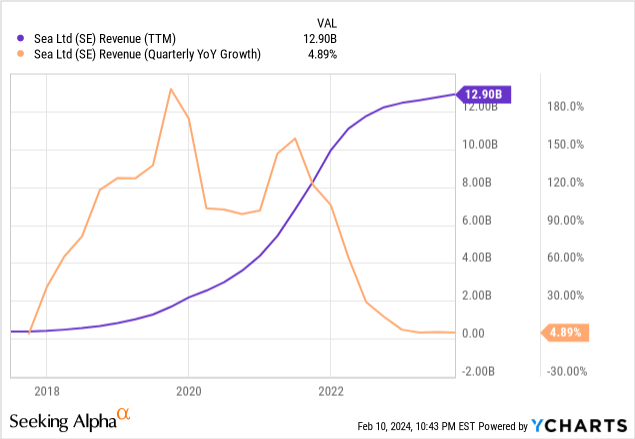

Over the trailing four quarters, $12.9 billion in revenue and $900 million in profits were reported. Unfortunately for buy-and-hold investors, the share price has moved/imploded from a peak number over $370 in October 2021 to a bottom at $32 in January for a -90% loss. The excuse? Business expansion rates have decelerated markedly from the stay-at-home boom during the early days of the pandemic in 2020-21, at the same time as Chinese and Asian economic growth has become suspect in 2023-24. I fully understand the angst owners of the stock must feel if purchased in 2021 and held all the way down.

The most straightforward explanation of wild fluctuations in Sea Limited's stock quote can be found in the acceleration and deceleration in operating sales.

YCharts - Sea Limited, Trailing Annual Sales & YoY Quarterly Growth Rate, Since 2017

For an education on all the moving parts in the underlying business, I highly recommend reading Seeking Alpha analyst

Riyado Sofian's take on the company from a

few months ago here.

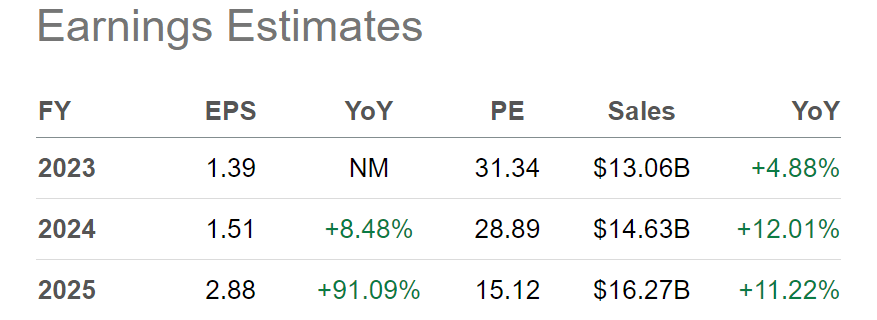

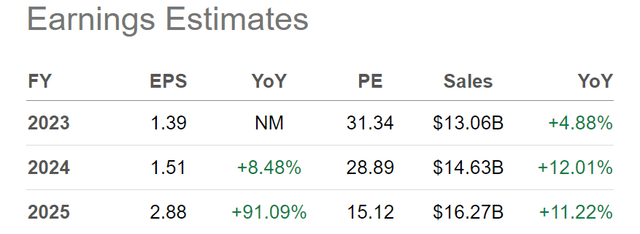

The summary bull thesis is company management is transitioning away from a landgrab grow-at-all-costs mentality to one centered on internally generated income and the self-funding of moderate rates of expansion. The company held around $1.5 billion in net cash (after debt) at the end of September, creating a liquid and conservative balance sheet. The best news is, Sea Limited is now churning out far smarter operating income levels vs. two years ago. Below is a table of the jump in income expected by Wall Street analysts for 2024-25.

Seeking Alpha Table - Sea Limited, Analyst Estimates for 2023-25, Made on February 9th, 2024

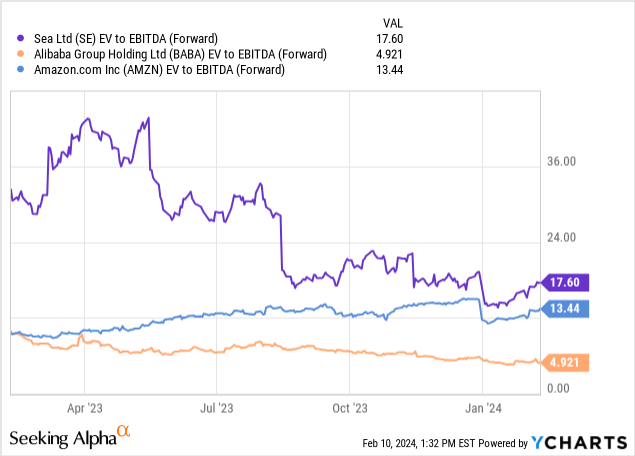

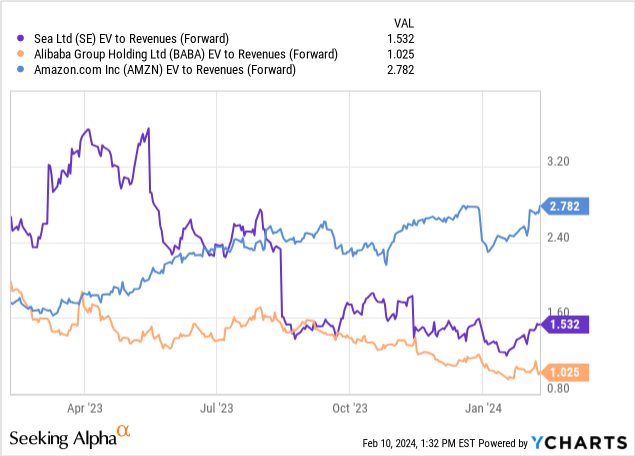

Compared to Alibaba and Amazon, Sea Limited runs a similar business model, with EV to EBITDA (17.6x) and sales (1.5x) multiples coming down on the huge share quote decline since late 2021. For sure, the enterprise valuation on forward estimates for basic cash EBITDA earnings (before reductions for interest, taxes, and non-cash depreciation & amortization) plus sales are more desirable today at HALF the ratios of 12 months ago.

YCharts - Sea Limited vs. Alibaba & Amazon, EV to Forward Estimated EBITDA, 1 Year

YCharts - Sea Limited vs. Alibaba & Amazon, EV to Forward Estimated Sales, 1 Year

Profit margins, both gross and final, have jumped considerably over recent years. Gross margins (46%) are the highest of the three names, with analysts projecting after-tax margins meeting or beating mighty Amazon during 2023-25.

YCharts - Sea Limited vs. Alibaba & Amazon, Gross Profit Margins, 5 Years

YCharts - Sea Limited vs. Alibaba & Amazon, Final Profit Margins, 5 Years

Aggressive Accumulation - Bottoming Pattern

The most exciting part of the Sea Limited investment backdrop is price appears to be in the early stages of breaking out of a base pattern since August. In addition, buying momentum supporting the price has been picking up steam since September. Let me explain.

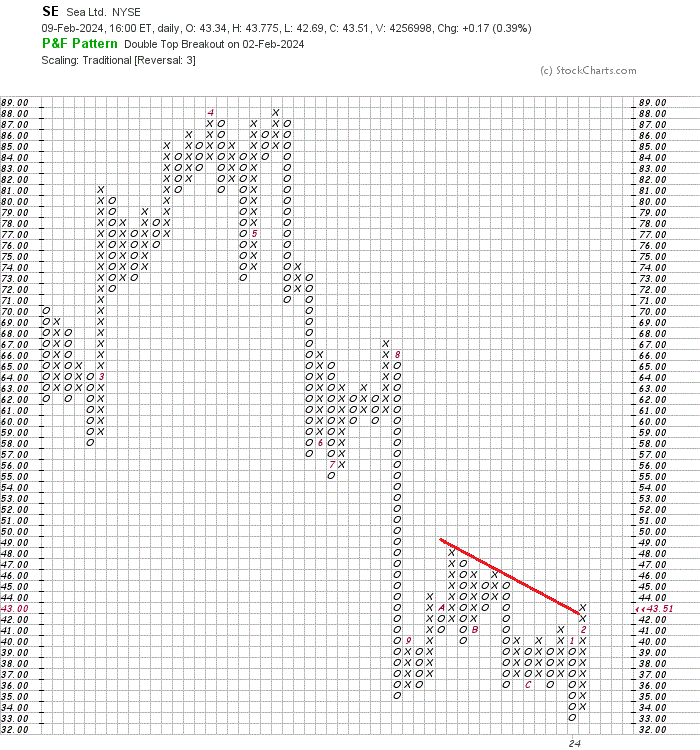

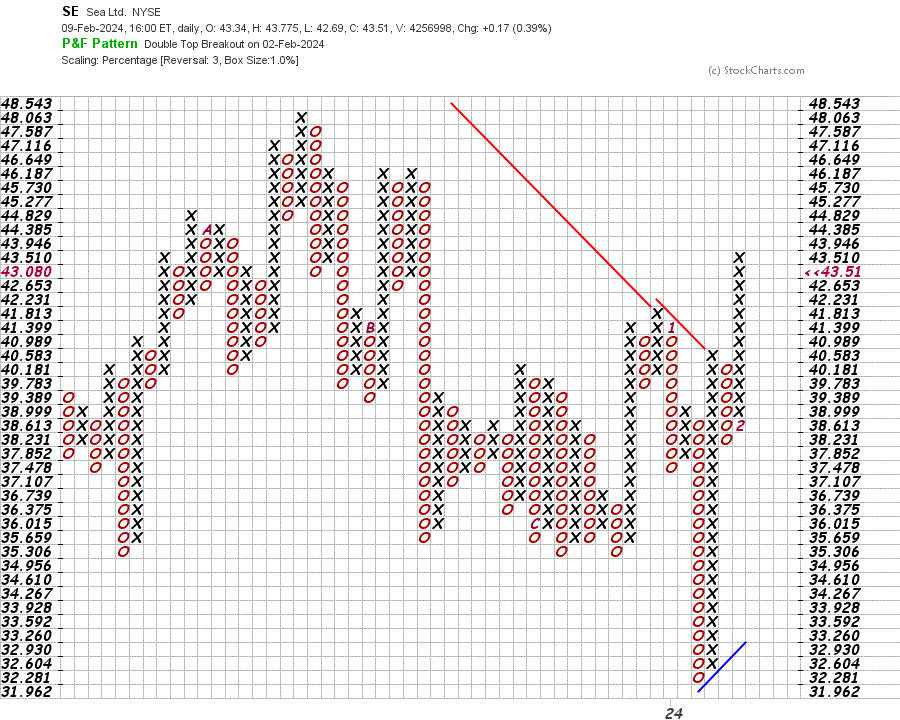

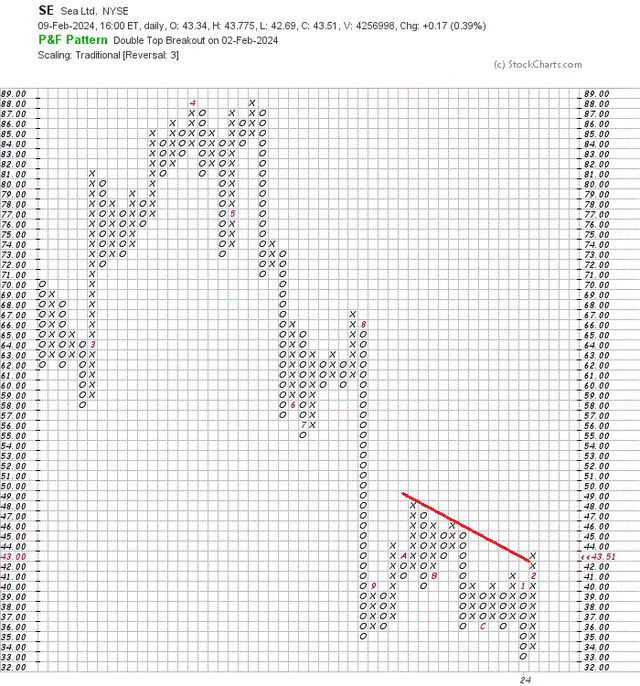

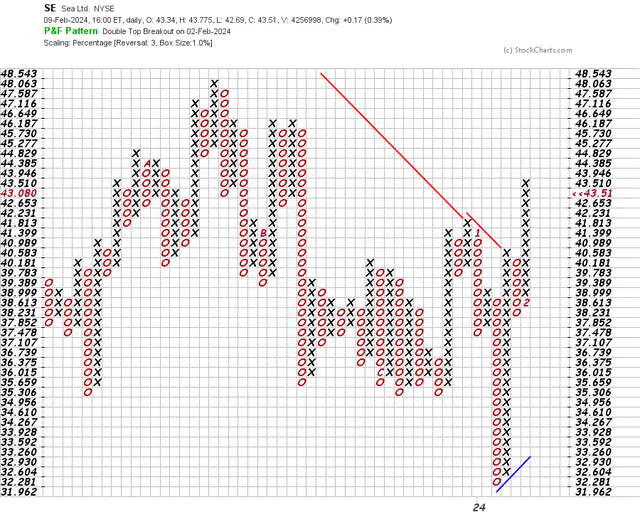

The price pattern becomes quite clear when we draw

Point & Figurecharts. This type of chart is focused purely on price changes (and does not utilize the traditional equal increments of time). P&F graphs can give insight into overhead share supply. In the current case for Sea Limited, sellers may be disappearing and/or exhausting share volumes for sale. Breaking above the red trendlines drawn as resistance is the key first signal of a potential turnaround.

StockCharts.com - Sea Limited, Basic P&F Graph, 1 Year

StockCharts.com - Sea Limited, Short-Term P&F Graph, 4 Months

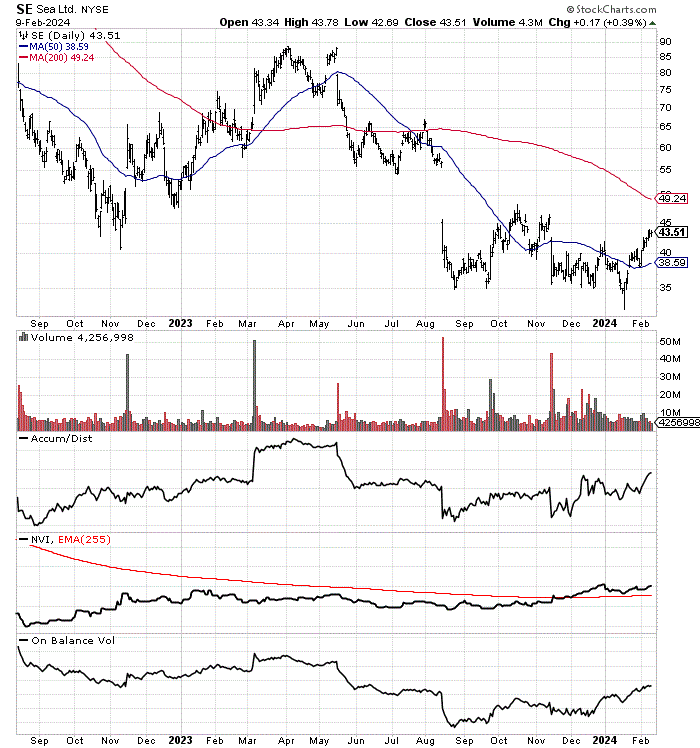

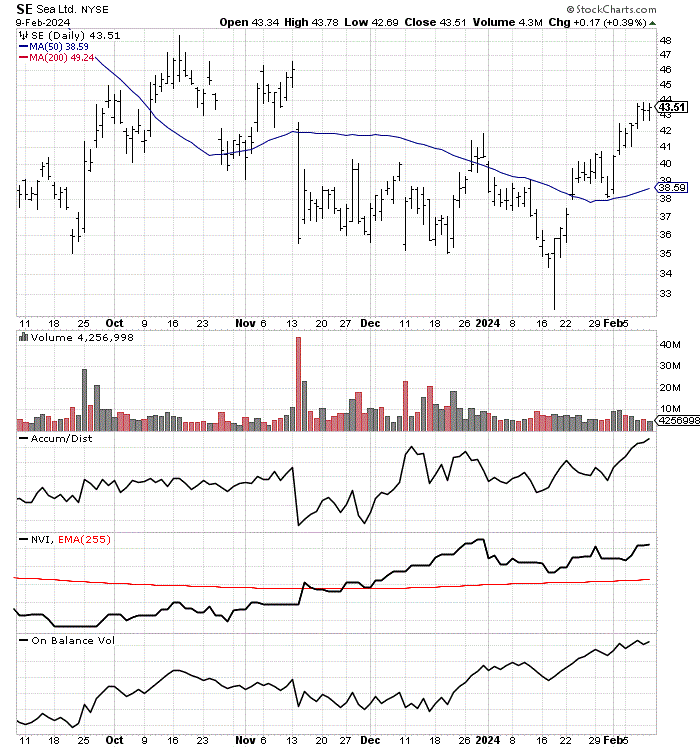

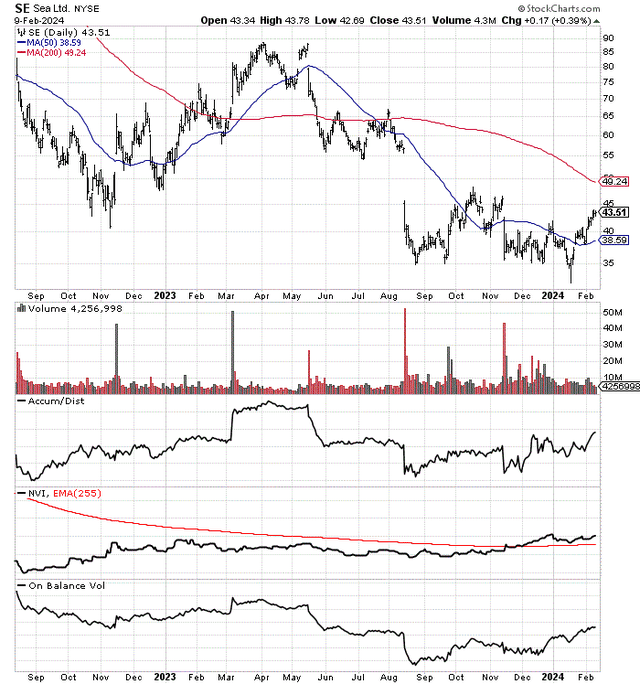

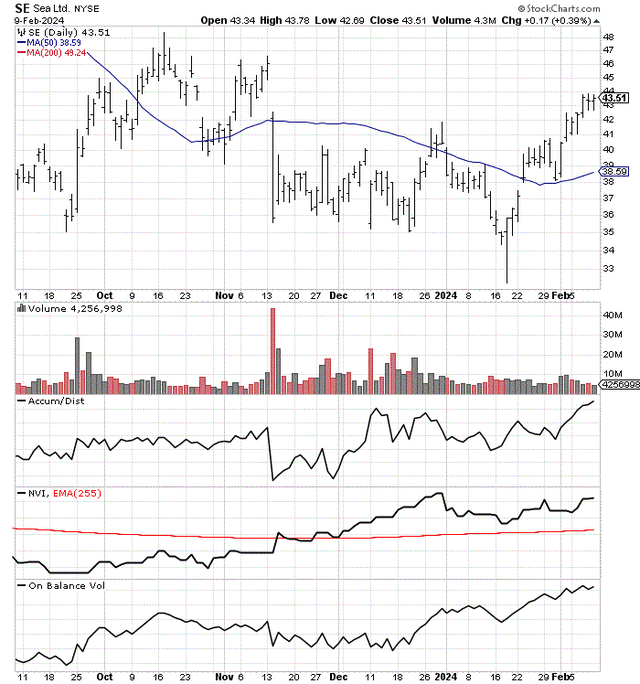

Just as impressive is the upward trend in many of my favorite momentum indicators, despite a relatively flat stock quote. Below, I have drawn an 18-month chart, and one focused on the latest 5 months of daily trading action.

Despite price selling off about -10% vs. its October peak, the

Accumulation/Distribution Line,

Negative Volume Index, and

On Balance Volumereadings were trading at or near 6-month highs last week. It could be buyers are starting to overrun sellers. This momentum setup is quite rare and usually a super-bullish development.

StockCharts.com - Sea Limited, 18 Months of Daily Price & Volume Changes

StockCharts.com - Sea Limited, 5 Months of Daily Price & Volume Changes

Final Thoughts

The company is expected to report December Q4 earnings in early March. If the news is good, I would expect an oversized gain in the share quote into April-May. Insider anticipation of bullish Q4 results or guidance for the new year could explain the robust underlying buying pressure in the stock for months.

I did write about Alibaba in a bullish manner

several weeks ago here. I would look at Sea Limited as a complimentary play, especially if Asia's economic fortunes turn for the better in 2024.

What could go wrong with investing in Sea Limited? For me, the biggest risk is Asia's economy remains sluggish all year. Under this scenario, getting much above $55 or $60 a share may prove difficult. Another downside possibility is a sizable "bear market" in global equities could keep the quote around $40.

Spending less on growth has also cost the company market share to more aggressive competition. Sea Limited's main competitors include

Mercoado Libre,

Lazada(owned by Alibaba), and

Tokopedia, which recently received a large investment from

TikTok. However, in my view, the transition to business profitability and sustainable growth will soon reward shareholders.

In terms of bearish target forecasts, I doubt price declines below $30 on a sustainable basis (closer to 1x sales). Why?

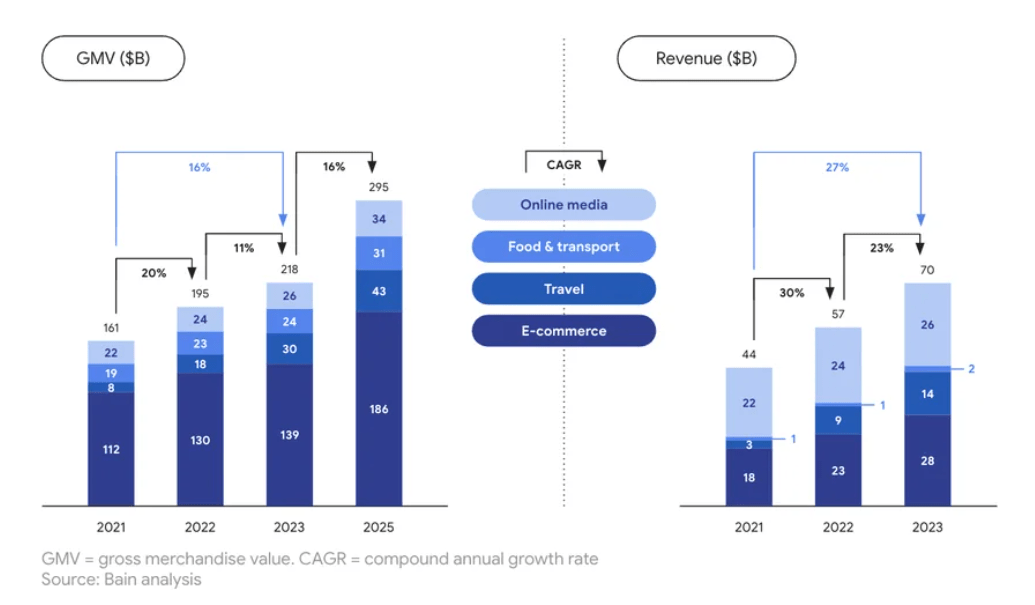

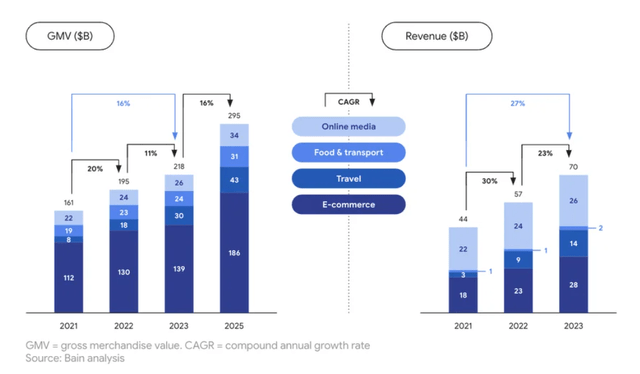

The growth outlook of sharply rising online use, especially through smartphones, in Southeast Asia is too positive to ignore. A

Google Blog in November, with research data from

Bain, highlighted the extraordinary digital growth of late in the Southeast Asia region,

The region’s digital economy is set to hit US$100 billion in revenue — an eight-time revenue increase for digital businesses in the last eight years. In fact, revenue is growing 1.7 times as fast as GMV, which is reaching US$218 billion this year.

Google Blog - Sapna Chadha Author, Southeast Asia Region Digital Economy Growth, November 1st, 2023

The bottom line is macroeconomic online sales have been mushrooming in the 20% to 30% annual range for this region of the world. Since Sea Limited is well positioned to ride this upward trend, while its valuation is back to a normal range, the outlook for share pricing is very bright. Given margin improvement on a 10% to 15% sales growth rate for years (subpar vs. the industry), I believe EPS well above $3 annually are approaching.

My plan is to acquire shares next week, as the valuation foundation exists to support a far higher quote on ANY resumption of higher business growth rates. The stock may be sitting in a similar position to the winning Big Tech names in America bought during late 2022 at depressed levels. I rate Sea Limited a

Strong Buy, with upside targets as high as $100 (3x sales) in 18 to 24-months, given any unexpected jump in revenue.

by

Paul Franke

Nationally ranked stock picker for 30 years. Victory Formation and Bottom Fishing Club quant-sort pioneer.....Paul Franke is a private investor and speculator with 37 years of trading experience. Mr. Franke was Editor and Publisher of the Maverick Investor® newsletter during the 1990s, widely quoted by CNBC®, Barron’s®, the Washington Post® and Investor’s Business Daily®. Paul was consistently ranked among top investment advisors nationally for stock market and commodity macro views by Timer Digest® during the 1990s.

SO THIS CAT AGREES WITH ME TA-WISE.

THIS IS A CLASSIC TEST OF TA VS FUNDI!!!!!