Unbelievable! You might want to adjust those negative deltas, buddy.https://secure.marketwatch.com/story/funds-600-million-lost-week-captivates-traders-2017-02-16

This is a nail in a coffin for all those who think that spreads are safer than naked options.

It is all about leverage and risk management.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

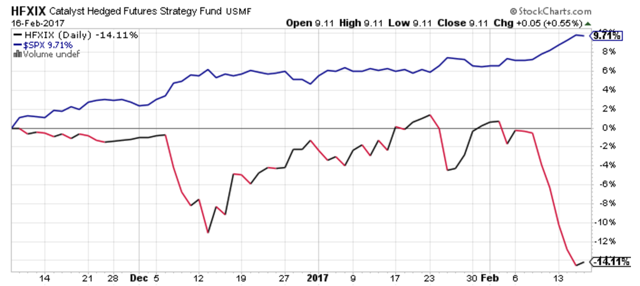

Fund loses 600mil (15%) doing spreads

- Thread starter RedDuke

- Start date

Perhaps simply due to a wrong directional bet!

Twice when S&P turning up 4%, it went down 12%.

http://seekingalpha.com/article/4047142-catalyst-hedged-futures-strategy-fund-rails

https://secure.marketwatch.com/story/funds-600-million-lost-week-captivates-traders-2017-02-16

Here’s how Catalyst got into trouble: The Catalyst fund’s strategy uses options on the S&P 500 index, contracts that allow investors to buy or sell at set prices over fixed time frames. In this case, the fund employed a “butterfly spread” that benefits the fund if the market remains stable, rises slightly or declines in any magnitude.

Twice when S&P turning up 4%, it went down 12%.

http://seekingalpha.com/article/4047142-catalyst-hedged-futures-strategy-fund-rails

Apparently, Catalyst's book was set up to benefit from declines in the market, as well as sideways and slow up moving markets. The fund's Achilles heel was a rapidly rising market. What is now readily apparent in hindsight is that Catalyst's book was net short gamma in way out of the money calls. Probably, somewhere between 5% and 10% out of the money, through the sale of February 1x4 or 1x5 call spreads. That's a buy of one call and the simultaneous sale of four or five higher strike calls. In a market that isn't moving, this part of the position will slowly decay and expire worthless, adding return to the fund through the collection of time premium. In a rapidly rising market, this is a huge problem as the fund becomes shorter and shorter as the market rises, generating increasing losses. These trades, according to some traders, left the fund short more than $15 billion SPX deltas.

Last edited:

Yeah, so maybe the bet wasn't totally stupid, after all... Obviously, it's impossible to know what the process for these guys is like, so it's all just educated guessing at best. Moreover, I am reasonably certain, based on what I've heard in the mkt, that the culprit was a very large 1 x 3 call spread position, rather than a fly.Please. I appreciate it.

Basically, the stupidest reason to do a 1 x X ratio spread is along the lines of "it will never get there". If that was the thinking here, then investors should run from these guys as fast as they can.

The not-so-stupid reason to do these is the idea that vol and mkt direction are correlated. There are all sorts of clever terms for these phenomena and they can get kinda complex (ask sle, if you want the gory details), but the basic idea is that, at least in the case of, say, SPX, vol tends to decline when the mkt rallies. So it could be that this was the reasoning here, which would make this a bit less of a silly bet. However, it still might have been at least somewhat silly, because of the leverage (a drawdown of 18% in a week is nothing to sneeze at) and the not-so-great entry level (vol already being so low).

the market is a pack of lies funded by mythical money. No amount of analysis or smarts will work all the time. The market gets a dose of truth from time to time and that is when all those smug assholes who think they are clever in a bull market, lose their poor clients' life savings. Ino longer bet against bullshit markets as I got my ass kicked 2004/5 when the market never looked back. However you can position for this if you understand that volatility is problem with calls, so rolling them is miserable-generating losses and opportunity cost. No sane trader could position themselves for a Trump administration-so many unknowns

Every...type of strategy/trade is essentially "garbage" ...the only difference is that if they happen to be Winning strategies, or trades,...then they are now called Genius trades, or a genius trader

I have to respectfully disagree with this point. Some strategies do have alpha that is persistent. The problem is that alpha has capacity, and once that capacity is reached, the alpha goes to 0. This is how markets stay efficient.

So based on this we can expect the market to correct deep next week because the trade is closed? Just skeptical that a $600m loss in a fund can drive the market for a week.

This is the question I have as well. If the trade caused that much market movement shouldn't it have caused dramatic changes in the skew structure of the options especially on the call side as they had to close specific strikes? Because I didn't see it.So based on this we can expect the market to correct deep next week because the trade is closed? Just skeptical that a $600m loss in a fund can drive the market for a week.

This is the question I have as well. If the trade caused that much market movement shouldn't it have caused dramatic changes in the skew structure of the options especially on the call side as they had to close specific strikes? Because I didn't see it.

So based on this we can expect the market to correct deep next week because the trade is closed? Just skeptical that a $600m loss in a fund can drive the market for a week.

The market didn't rally because of this fund. For much of the delta this fund bought there was a bank or market maker selling delta against them.