No offense, but why the CFD market? Also, I think you are doing too much for calculating. The holding cost and fee are just crazy and can't be compared to the CME products. Let's say if you have to adjust your position daily, or even 2 times a week due to the 'N' changes. That's already 8 times a month for trading fee + (around)20 days holding cost, which is a crazy amount of fixed fees that you should pay even before making a profit out of it.

For CME Micro Crude oil, where one tick movement (0.01) equals $1, I got the minimum capital for 1 contract as around $13,000 from the last close price, 71.78. In order to run 4 contracts, that is around $52,000. Compare the tick movement per lot size with the CFD crude oil.

For the FX rate, I used 1.0, and for σ%, I used just 20 days of "something" (if you don't get it, DM me)

If you look at p.72 from his newest book, you will see the minimum capital to trade for each symbol, and I think $13,000 is quite the right number since for Gasoline futures, it is more than $450,000.

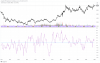

One thing I don't understand is Rob's dynamic EWMAC doesn't make money on RB, HO, while the static approach makes money.... I don't know what I coded wrong. It made good profit on NG though.

@globalarbtrader, could you please confirm if your Strategy no.9 makes money on these two instruments (HO and RB)? If so, I need to re-write my whole code.

")