Hi Rob,

You have reported the following return on your Systematic Trading:

2014 >>> 124.0%

2015 >>> 23.0%

2016 >>> -14.0%

2017 >>> -3.7%

2018 >>> 1.0%

2019 >>> 7.0%

2020 >>> 0.3%

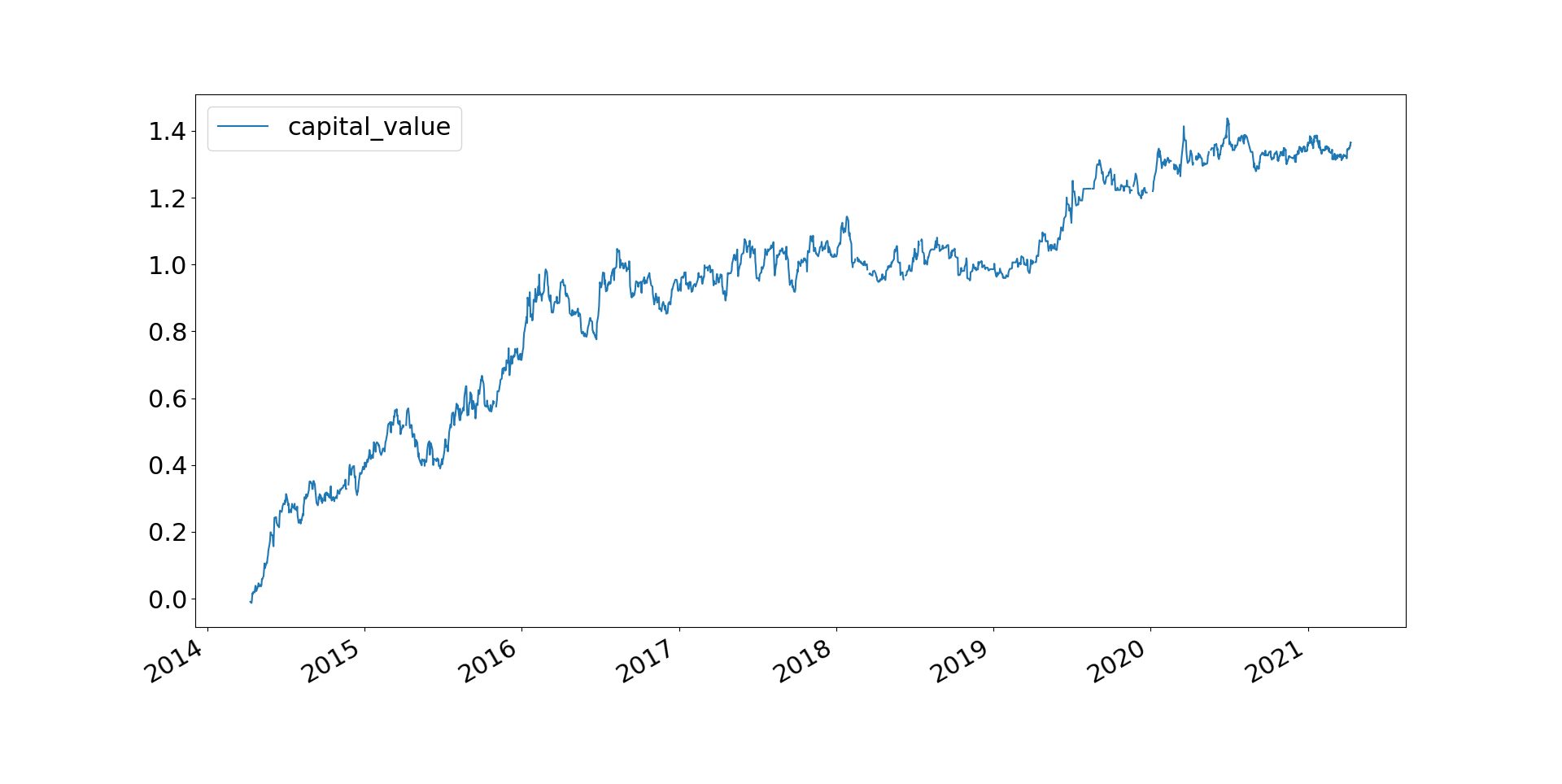

Could you please explain the following chart? is this the growth rate of your capital? or it is your profit in million GBP?

you mentioned you started with 300K Gbp. Did you add any money? how much you withdrawn from your profit?

Thanks a lot

YAD

I don't recognise those figures but let's assume they are right

The chart is the cumulative percentage return on my current capital. So 1.0 implies a 100% cumulated return. This wil be very similar, although not identical, to a log scale if I compounded my returns (which I do not, see below)

I did indeed start with 300k in risk capital but my account balance was actually larger), but I've run with 400k fixed capital for some years now. I've never added money, I withdraw all my profits above the 'high water mark'.

More explanation here

Updated figures:

My drawdown is 48k

My notional capital is 400 - 48 = 352k

My risk target is 25% * 352k = 88k

My account value is 353k (I have a 'buffer' of just 1k nowadays)

My accumulated profits are 684k (would have been 732k at high water mark)

My total withdrawals are 801k, of which 732k is profits about the HWM and the rest reflections a reduction in my buffer size.

Rob

Rob

") ) according to my schedule "soft-roll" period is Feb1-Mar13 during which new positions will be opened in Jul contract, but the existing positions in May will be allowed to exist till March 13 and will be forcefully rolled into May after.

) according to my schedule "soft-roll" period is Feb1-Mar13 during which new positions will be opened in Jul contract, but the existing positions in May will be allowed to exist till March 13 and will be forcefully rolled into May after.