It's not statistically significant. I also added the rule, and saw that there wasn't the statistical evidence to include it, so removed it.

I did implement @globalarbtrader 's short bias on vol futures.

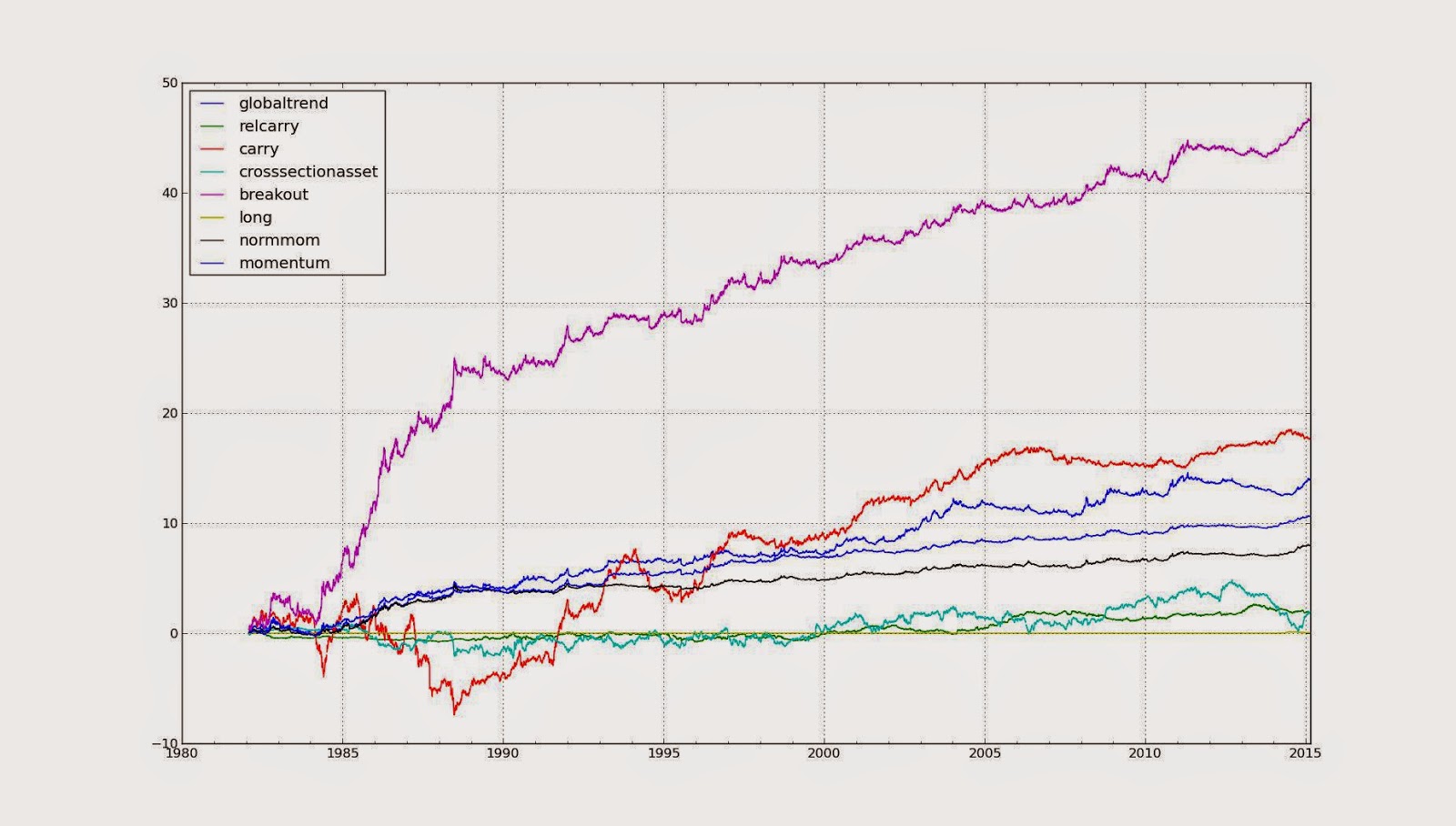

I find it puzzling that breakout didn't do it for you when looking at this graph. I wonder what can explain the discrepancy?

")

")