Hi GAT,

I am currently reading your book I must say it has really filled in all the gaps in my 5 years of experience with the markets. I have several questions about an old chart you posted in page 6 of this thread.

If you don't mind sharing,

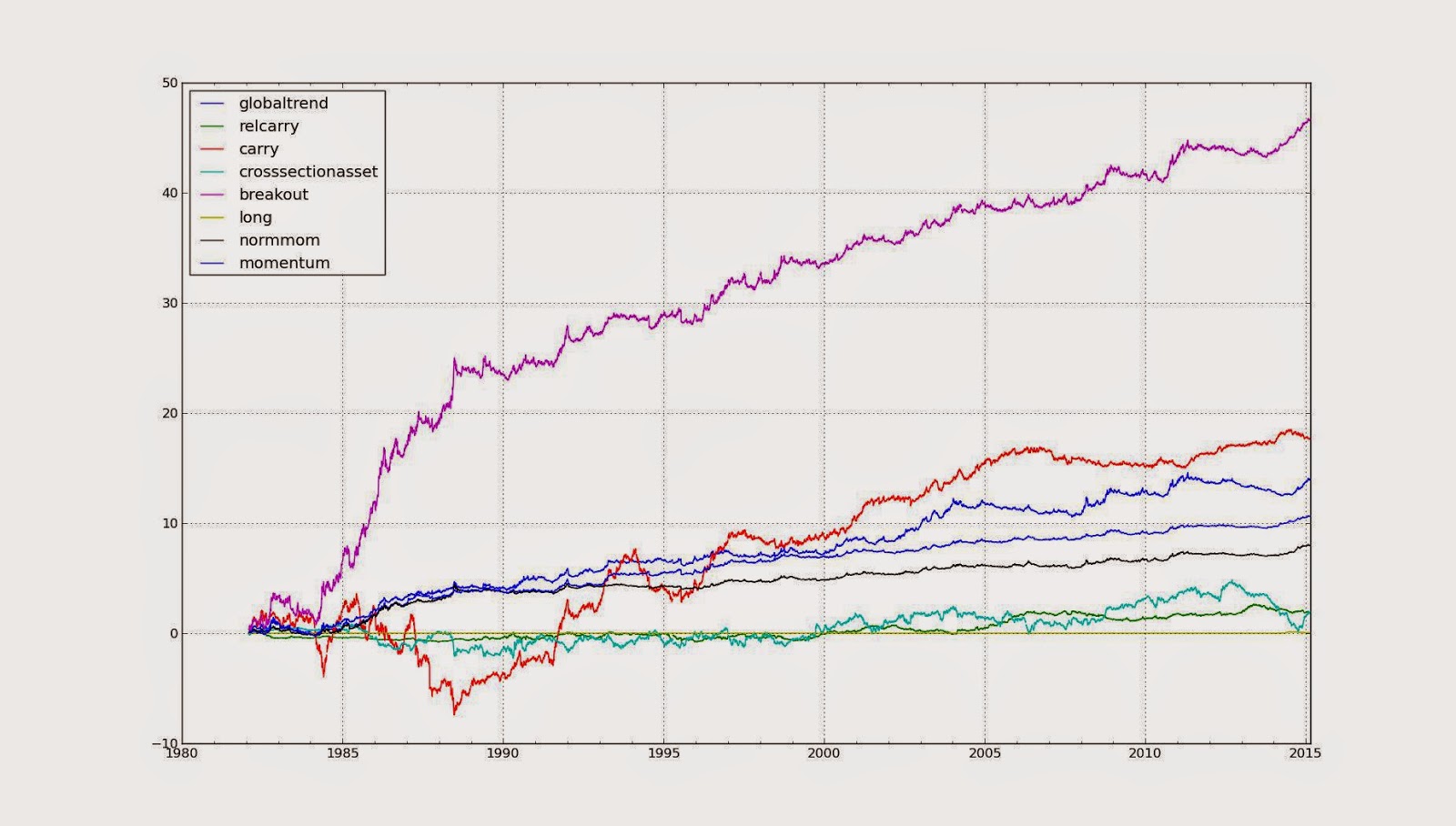

1) Why does breakout outperform momentum by such a huge margin? I ask because you provided some correlations in your blog for ewmac vs breakout and it seems that breakout and momentum should be pretty similar in terms of performance.

Is the breakout rule in this picture similar to http://qoppac.blogspot.sg/2016/05/a-simple-breakout-trading-rule.html or a vastly different animal?

2) What is the difference between relative carry and carry?

3) What is the difference between momentum and normmom?

4) What is the difference between globaltrend vs momentum?

5) Can you elaborate a bit more about crosssectionasset?

Thank you so much!

1) the graph is not vol adjusted, but shows the contribution of each trading rule to total profits. Breakout has a higher weight, so contributes more. Having said that breakout does seem to be more profitable than ewmac [remember something can be correlated, but still have a higher average return].

2) carry is done on each instrument, relative carry within asset class

3) the former is ewmac on the price, the latter ewmac on the cumulative vol normalised returns

4) the former looks at the entire asset class, the latter just each instrument

5) it's mean reversion within asset class ;if CAC has outpaced AEX then I'd buy the latter

I'll be releasing python code for all these at some point

GAT