Code:

code contractid filled_datetime filledtrade filledprice

2849 AEX 201503 2015-03-04 08:02:38 -1 481.250000

2848 AUSSTIR 201603 2015-03-04 02:34:45 -1 97.980000

2850 US5 201506 2015-03-04 14:20:22 -1 118.867188

Slippage in GBP, for entire trade

code gbpt_slippage_process gbpt_slippage_bidask gbpt_slippage_execution gbpt_slippage_all_trading gbpt_slippage_total

2849 AEX -247.44 7.28 -0.00 7.28 -240.17

2850 US5 -0.00 2.54 -0.00 2.54 2.54

2848 AUSSTIR 18.34 6.11 -12.23 -6.11 12.23

Total slippage: process -229.100000; bidask 15.930000; execution -12.230000; all trading 3.710000; grand total -225.400000These are mainly risk reduction trades on the back of the recent drawdown.

The AEX sample price was grabbed at closing time, and traded the next morning, hence the large positive price movement.

Yesterdays LOSS: £1,645

In my past i used work for an affiliated firm of ahl so i was somewhat familiar with their product. Ahl, Aspect and the like would have gradually building and tapering positions in various markets over multi systems like what you are doing. But such firms had a sharpe of maybe 1.0.

You have a sharpe of twice that. What would you say you are doing differently from them?

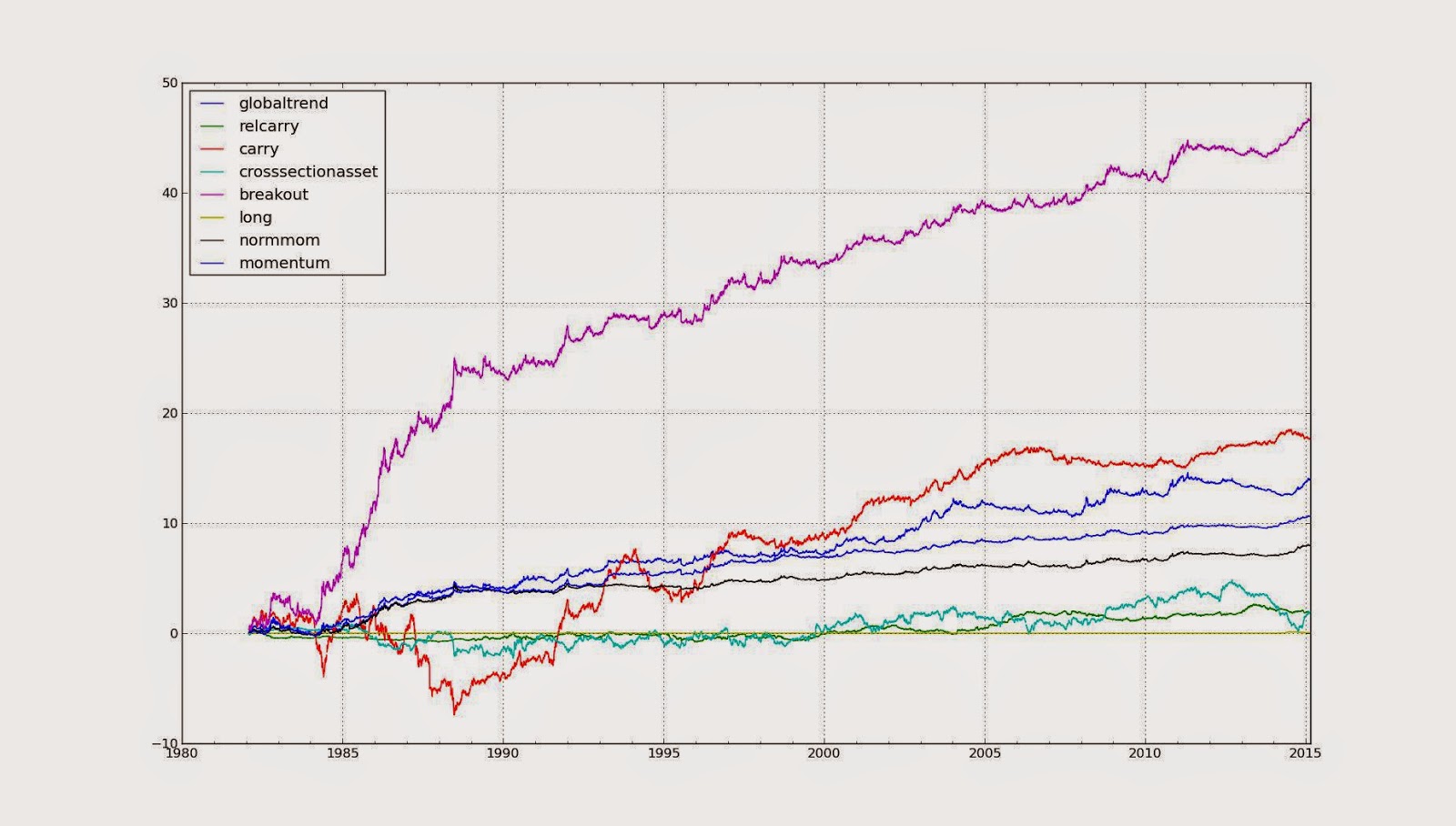

Not much differently (I don't know if you are aware of this but I used to work for AHL). AHL also had a very high Sharpe last year. On a risk adjusted basis we're probably pretty even. I will soon post my simulated returns. The average SR from 1980 onwards is about 0.9. So in a similar ballpark.

For what its worth:

Reasons why AHL should do better than me, in order of importance:

- Much wider set of markets traded; perhaps 300 versus 43.

- Much lower execution commissions paid

- Smarter execution algos, but more importantly experienced execution traders.

- Large team of researchers refining and developing models

Reasons why I might do better, most important first:

- I have a lower allocation to trend following, so a more diversified style of trading.

- There are no fees

- Institutional pressures leading to models changing and frequent overrides (http://qoppac.blogspot.co.uk/2014/05/why-black-box-hedge-funds-should-have.html)

- Smaller size, so lower slippage

")