You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Fully automated futures trading

- Thread starter globalarbtrader

- Start date

One more question.

Why own the futures contracts in favour of spread bets on the underlying?

Advantages as I see them: No rolling necessary, lower block size, simpler API (IG), CGT.

I'm not sure I agree with the API comment, but that's opinion. Lower block size is the main advantage of spread bets.

Disadvantages - much higher costs, OTC with all that represents

You need to roll quarterly bets; daily bets are very expensive spreadwise.

GAT

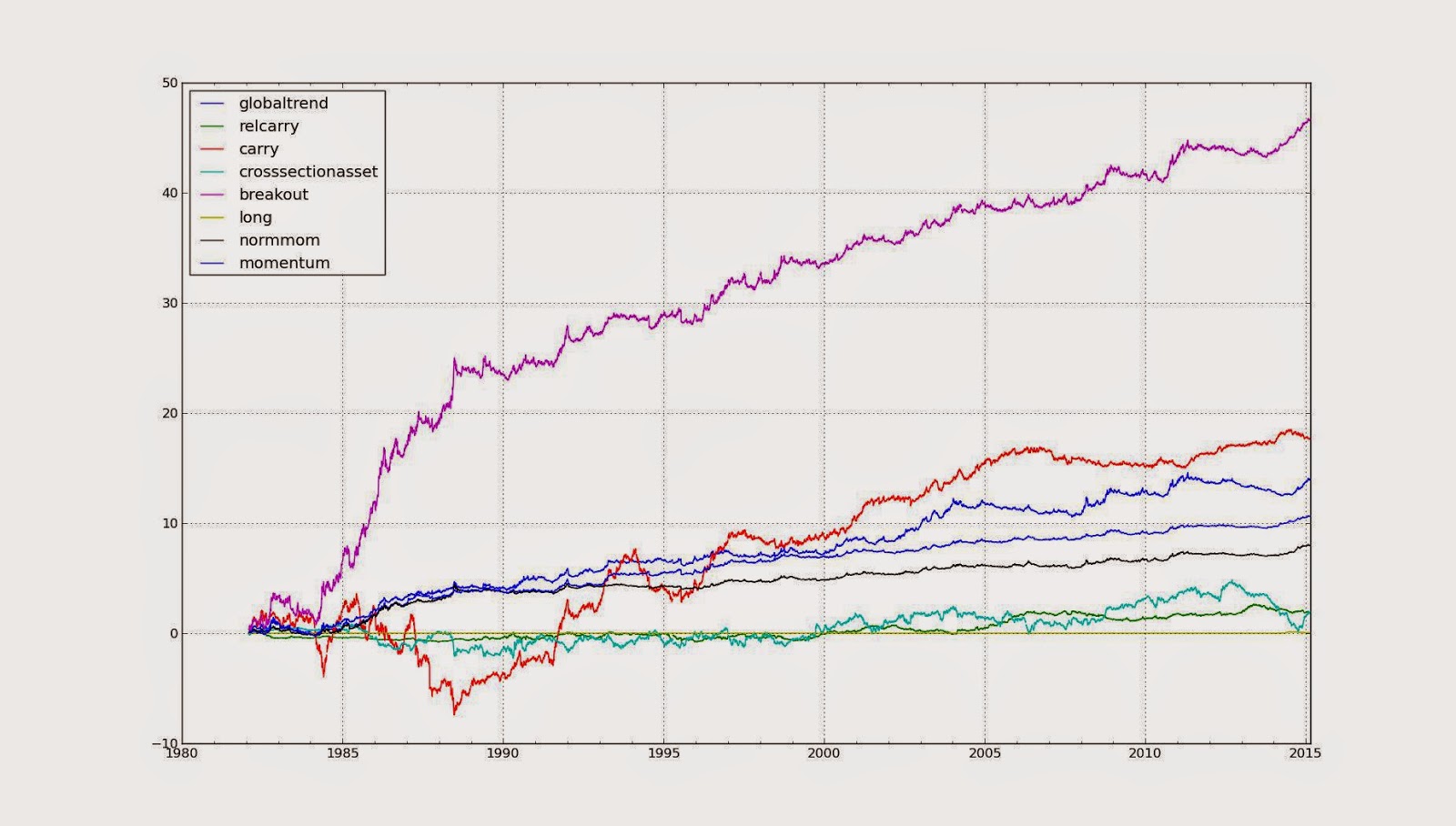

I've finally got round to producing a new backtest which can be found here

The bottom line is that the last year has indeed been exceptionally good, versus a realistic long run back tested Sharpe of 0.88.

2009, 2011 - 2013 are flat. However 2010 is more interesting, as my backtest made some money whilst the CTA industry generally didn't. I've done a bit more digging since I wrote that post and this is a further breakdown by trading rule:

'globaltrend', 'breakout', 'normmom' and 'momentum' are different flavours of trend following. Although AHL (and I guess other CTA's) use similar versions of these rules (with the possible exception of 'normmom' which is my own entirely original, though very simple, creation) they don't have them in the same proportions as I do. In particular 'momentum', which is an EWMAC system, was a relatively large part of a typical CTA system in 2010*, wheras I have a more equal weighting. The highest blue line (below the red line) is this type of system, which did the worst in 2010.

This scale of outperformance may not be repeatable, but in general I think its better to have a spread of different kinds of trading rules rather than relying too much on one.

* I have no idea what the typical proportions are now.

Hi GAT, I have included your breakout rule with several parameters ranging from 20 to 320 in pysystemtrade as well as ewmac (parameters from 2 to 256) and carry, and applied the optimization process to these.

I have used the same sample set of instruments as you include with pysystemtrade. For curiosity, I grouped all breakout and ewmac rules together and mapped out their equity curves to compare with what you produced in the post above.

I am concerned that my breakout system and ewmac system are very highly correlated (see attached graph below), where as yours do not seem to be correlated. Have you adjusted any other parameters around your breakout strategy / do you have any insight as to why my ewmac and breakout curves move very close to one another?

Thanks!

Hi GAT, I have included your breakout rule with several parameters ranging from 20 to 320 in pysystemtrade as well as ewmac (parameters from 2 to 256) and carry, and applied the optimization process to these.

I have used the same sample set of instruments as you include with pysystemtrade. For curiosity, I grouped all breakout and ewmac rules together and mapped out their equity curves to compare with what you produced in the post above.

I am concerned that my breakout system and ewmac system are very highly correlated (see attached graph below), where as yours do not seem to be correlated. Have you adjusted any other parameters around your breakout strategy / do you have any insight as to why my ewmac and breakout curves move very close to one another?

Thanks!

View attachment 164060

I agree that looks wrong. If I was to guess, perhaps the forecast and instrument weights that have come out are creating the high correlation?

If it's any help I'm going to do some coding for psystemtrade in the next week or so, and one of the things I'll include will be the breakout rule.

GAT

Video of my MTA presentation https://www.mta.org/video/the-myth-of-the-perfect-trading-system/

enjoy

GAT

enjoy

GAT

Hi GAT,

So I'm up to bootstrapping weights on single instruments now, using an expanding window, looking at Corn using EWMAC.

I'm concerned the weights never really seem to stabilise:

(legend is LFast).

For reference I've plotted the price series here:

.png")

I've taken slippage of 0.25/380 + $2.80 in fees for every contract traded.

Does this look right? Would you feel comfortable trading this? (I'm beginning to wonder if my implementation is sound).

Thanks!

So I'm up to bootstrapping weights on single instruments now, using an expanding window, looking at Corn using EWMAC.

I'm concerned the weights never really seem to stabilise:

(legend is LFast).

For reference I've plotted the price series here:

I've taken slippage of 0.25/380 + $2.80 in fees for every contract traded.

Does this look right? Would you feel comfortable trading this? (I'm beginning to wonder if my implementation is sound).

Thanks!

Last edited:

Hi GAT,

So I'm up to bootstrapping weights on single instruments now, using an expanding window, looking at Corn using EWMAC.

I'm concerned the weights never really seem to stabilise:

View attachment 164079

(legend is LFast).

For reference I've plotted the price series here:

View attachment 164080

I've taken slippage of 0.25/380 + $2.80 in fees for every contract traded.

Does this look right? Would you feel comfortable trading this? (I'm beginning to wonder if my implementation is sound).

Thanks!

No doesn't look right at all. All the money going into a pair that I wouldn't include at all would terrify me. Have you got the account curves of the individual rules just on corn? What do they look like before and after costs?

GAT

Looks wrong. Curves are way too smooth (not enough standard deviation)

GAT