I'm sure Krugman is trying to think how he'll explain this in his NYT column. For a long time now we've heard that there's no problem with more debt. After all, look at the bond market! No matter how many times those of us with a shred of intelligence have replied that this was because the Fed was the only game in town, buying up all the debt issued and keeping rates artificially low, the Krugmanites didn't believe it. "Debt doesn't matter!" they would cry.

Well, yesterday the Bearded Blunder himself indicated that rates would probably rise sometime a year from now. Furthermore, the life blood of markets everywhere - otherwise known as QE - is about to be pulled back slightly (and only slightly). But apparently this was enough to send a shockwave through the markets. Debt doesn't matter, indeed. An interesting blog article, from Mish:

http://globaleconomicanalysis.blogspot.com/2013/06/fed-keeps-low-rate-policy-intact.html

Curve Watchers Anonymous has a close eye on treasury yields in the wake of essentially no news from Bernanke as to when the Fed might actually begin hiking rates.

A mere hint the Fed might slow its QE program was enough to send treasury yields and the US dollar higher and stocks lower.

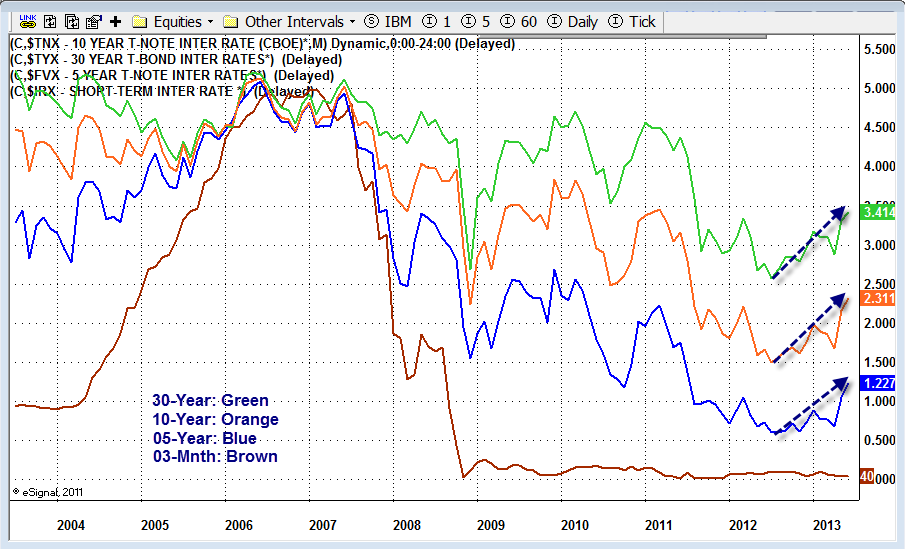

Yield Curve 2013-06-19

Curve Watchers Anonymous notes the yield on the 10-year note is up 13 basis points from yesterday, and the 5-year note is up 17 basis points from yesterday.

Here are some charts Yields are off by a factor of 10. For example 5-year treasury yield is 1.27% not 12.27%. Note the selloff (rise in yield) the mid-day moment Bernanke opened his mouth.

$FVX - 5-Year Treasury Note

$TNX - 10-Year Treasury Note

$TYX - 30-Year Treasury Bond

These are significant selloffs in this environment.

So what did the Fed say?

Nothing. At least nothing the market should not have expected.

Bloomberg reports Bernanke Says Fed on Course to End Asset Buying in Mid-2014.

Over that bit of nonsensical fluff (completely expected as well as frequently repeated fluff at that), the bond and stock markets threw a hissy fit.

This is further evidence the current markets are all about liquidity and speculation and nothing about fundamentals (in case you did not realize that already).

Well, yesterday the Bearded Blunder himself indicated that rates would probably rise sometime a year from now. Furthermore, the life blood of markets everywhere - otherwise known as QE - is about to be pulled back slightly (and only slightly). But apparently this was enough to send a shockwave through the markets. Debt doesn't matter, indeed. An interesting blog article, from Mish:

http://globaleconomicanalysis.blogspot.com/2013/06/fed-keeps-low-rate-policy-intact.html

Curve Watchers Anonymous has a close eye on treasury yields in the wake of essentially no news from Bernanke as to when the Fed might actually begin hiking rates.

A mere hint the Fed might slow its QE program was enough to send treasury yields and the US dollar higher and stocks lower.

Yield Curve 2013-06-19

Curve Watchers Anonymous notes the yield on the 10-year note is up 13 basis points from yesterday, and the 5-year note is up 17 basis points from yesterday.

Here are some charts Yields are off by a factor of 10. For example 5-year treasury yield is 1.27% not 12.27%. Note the selloff (rise in yield) the mid-day moment Bernanke opened his mouth.

$FVX - 5-Year Treasury Note

$TNX - 10-Year Treasury Note

$TYX - 30-Year Treasury Bond

These are significant selloffs in this environment.

So what did the Fed say?

Nothing. At least nothing the market should not have expected.

Bloomberg reports Bernanke Says Fed on Course to End Asset Buying in Mid-2014.

Federal Reserve Chairman Ben S. Bernanke said the central bank may start reducing bond purchases later this year and end them in mid-2014 if the economy continues to improve as the central bank forecasts.

âIf the incoming data are broadly consistent with this forecast, the committee currently anticipates that it would be appropriate to moderate the pace of purchases later this year,â Bernanke said today in a press conference in Washington. âIf the subsequent data remain broadly aligned with our current expectations for the economy, we will continue to reduce the pace of purchases in measured steps through the first half of next year, ending purchases around mid-year.â

Bernanke stressed that the Fed has âno deterministic or fixed planâ to end asset purchases.

âIf you draw the conclusion that I just said that our policies -- that our purchases will end in the middle of next year, youâve drawn the wrong conclusion, because our purchases are tied to what happens in the economy,â he said. âIf the economy does not improve along the lines that we expect, we will provide additional support.â

The Fed repeated that it will keep buying assets âuntil the outlook for the labor market has improved substantially.â

Over that bit of nonsensical fluff (completely expected as well as frequently repeated fluff at that), the bond and stock markets threw a hissy fit.

This is further evidence the current markets are all about liquidity and speculation and nothing about fundamentals (in case you did not realize that already).

")