I'm sure your food price data is valid. You still seem to me to be flirting with the idea that "a little" deflation would not be so bad. As long as we can agree that deflation is negative inflation in the overall economy and not just some price reductions in a segment of the economy, oil for example, we can discuss this on the same wavelength.

It does seem to me that the official inflation figures underestimate the inflation that most of us experience in our everyday lives. It is a fact that the government has revised its methods of computing various measures of inflation in recent decades. These revisions have invariably resulted in a lower, official inflation rate used to adjust inflation indexed treasuries and entitlements. Cutting adjustments of entitlements and interest on treasuries isn't as evil as it first sounds, because there is feedback into the economy that helps hold inflation in check.

One of the changes has been the introduction of hedonics. That's perhaps the most controversial change. Also, when baskets of good and services are used to compute an inflation measure the components are weighted; changes in the prices of some components counting much more than others. You can access these weighting factors at the Bureau of Labor Statistics website. An estimate of the CPI as it would have been computed in 1986 is available at shadowstatstics.com. The 1986 methods produce an inflation rate that is about 3 to 4% higher than the CPI estimated by current methods.

A good argument can be made, I won't make it here, for the 1986 method producing inflation rates that correspond better to the inflation actually experienced by consumers. I have never known an economist, however, who seems interested in my experience with sticker shock at the grocery store. The newer methods produce numbers just as useful to economists as the older methods, but have the advantage of helping to control inflation via feedback from inflation indexed entitlements.

Clearly, the estimation of inflation in the prices of goods and services in the overall economy is an inexact undertaking. Using current methods, the Fed economists decide what they think is the best estimate for their purposes. They are aware of flaws in the inflation estimates and the difficulty of estimating the effects of changes in monetary policy, so they have built in a safety factor. And that is why you see the inflation target set at 2% and not zero %. It isn't that a two percent inflation rate is better than a one percent inflation rate; it is that 2% is less dangerous than a lower target! The Fed believes that deflation could have an extremely deleterious affect on the U.S. economy. Consequently, of the two evils, mild inflation vs. deflation, they consider the former to be a much lesser evil. They use very low core inflation, and other measures too, as a warning that deflation may be on the horizon. They want to lessen the odds of deflation by choosing a target inflation rate well away from zero. They chose 2%, and my guess is that that is not an arbitrary number, but one based on economic research and error estimates for the inflation measures.

Just having prices in some parts of the economy rising or falling is not necessarily what concerns the Fed economists. Their concern is what is happening in the economy overall, in other words, the macro view. If the core inflation rate, everything but food and energy, falls below 1%, they will start to get concerned about the possibility of deflation, i.e., a negative inflation rate, in the overall economy. The Fed's view, which I share, is backed up by past experience and a vast body of economic research and studies.

If you are one that believes "a little deflation" would not be so bad, then I would say the correctness of you position depends on how much is "a little", for how long, and what measures you would take to prevent slipping further into deflation. Would you, Fed like, try to control the deflation rate at say 2%. You could try monetary policy. Even were that possible, you'd then have real interest rates on public and private debt not merely rising, but rising compounded over time! Talk about debt trauma! Yikes!

The U.S. is a nation of borrowers and spenders -- through a constant barrage of advertising, and capitalist hucksterism in general, we have unconsciously become psychologically well-suited to borrowing and spending. Notwithstanding the impossibility of infinite growth -- this is a pattern that fuels growth and innovation in an economy. Among fully developed nations, the U.S. economy consistently leads in growth and innovation. It takes credit to grease the American economy's wheels. Significant deflation in the U.S. economy would be an unmitigated disaster!

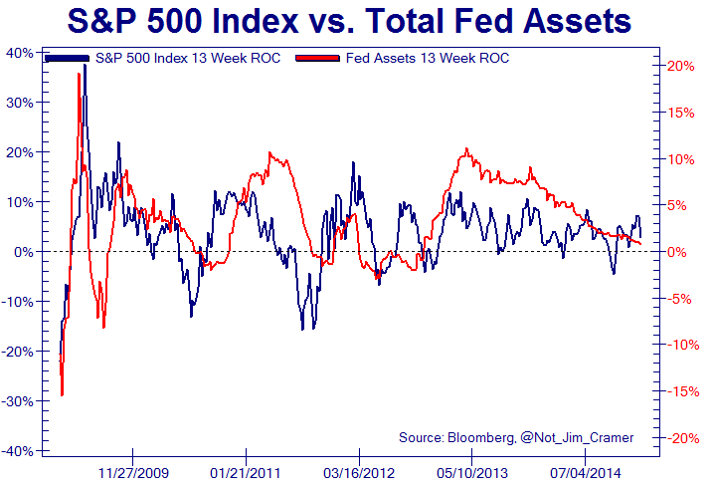

The U.S. flirted briefly with deflation in late 2008 to early 2009, but the Fed stepped in with extraordinary measures to rescue our economy. And thank goodness for that!

It isn't until you get to the last third of your post do you begin to fall off the tracks, in my opinion. First, I had a nice chuckle when you said that the Fed's view is backed up by past experience and a vast body of economic research and studies. That's quite amusing. This forum allows 10,000 characters per post, and I wouldn't be able to post all of the prediction FAILs and missed bubbles, housing crises, etc. All the things the Fed is paid to foresee with their vast experience and data. Yet, run-of-the-mill traders and economists see things clearer than they do.

When I say "a little deflation", I'm referring to the natural business cycle. The cycle that has been interrupted by massive central bank and government meddling. If the cycle were allowed to auto correct, and interest rates were not artificially altered, and bubbles weren't allowed to be created - or were deflated when spotted - we'd have short periods of deflation before growth took off again. But they don't. They try to go against the laws of nature until the walls come crashing down and real deflation is a risk. They only exacerbate this, they don't prevent it or mitigate it.

The US is a nation of borrowers and spenders because we have essentially punished those fiscally responsible (savers) and rewarded all those who took risky bets with high leverage. We've enabled the behavior and the economy we are stuck with in no different manner than a parent enables poor child behavior. So why should we be shocked when people go all-in on leverage, borrow to the hilt and just walk away when everything comes crashing down? Why should we be surprised when pension funds - who have relied on good, stable rates to provide returns have no choice but to throw their money into the casino to get some yield? Who enables all this? Your precious Fed and your beloved Big, Bloated Government.

The Us flirted briefly with deflation in late 2008 as a result of a decade or so of bad Fed/Government practice and bubble creation. Then, they compounded their error by not letting the market clear itself. The result is that deflation is coming no matter what they do.

And they know it.