Are you able to share a bit on how to do optimal hedging?

As you may already know, albeit being very rigorous in its derivations and systematic approach, options sensitivities leave a wide gap to be filled by heuristics and relatively arbitrary techniques when it comes to two areas: 1, the future volatility, and 2, the right hedging approach due to the former.

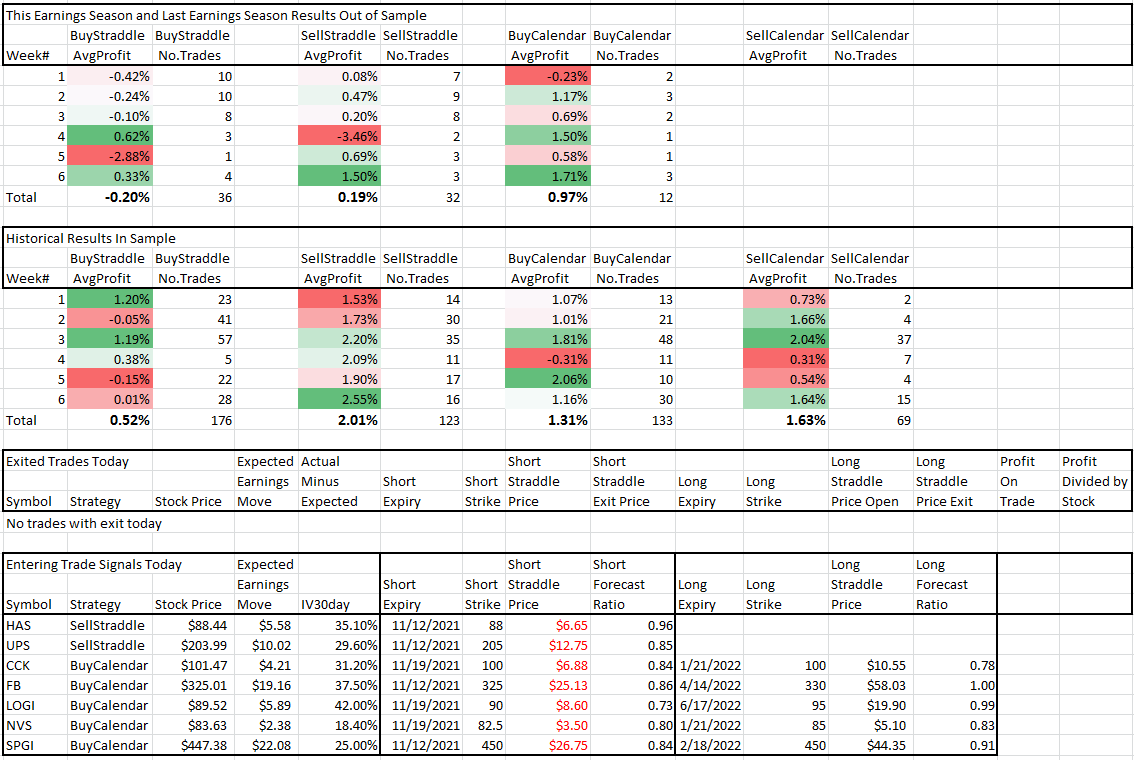

My approach is "book-based" in terms of an options book, estimating the overall exposure. At any given point, I have positions in multiple expiry and strikes. However, on a minimal number of underlying (10 - 12), I aim to have most of my sensitivities "netted" out and print the critical levels for the positions where I intend to keep the position until expiry and delta hedge those positions. For example, I can take a tesla position of 25 calls with strike 1000 that I am net short expiring on December 17th. The position was entered at the beginning of this year and was initially part of a multi-leg combo on the put and the call side.

Most of the positions in the combo have been deconstructed and what remains is the 25 shorted call contracts that I hedge on a block of 125 shares per pre-defined price level with the algo... below is a simple GUI for my algo that is on my desktop for simple and quick actions, initial order carpet and limits and offsets are uploaded via a simple CSV and once started the logic is on the server-side that takes over and handles the positions.

It's capable of hedging on multi markets and multi-currency for Tesla, Apple, FB, and Netflix; after the US markets close, the after-hours included the algo switches to XETRA to hedge the position there. I do the design and formalization of my algos and the models but have 2 Dev resources that do the coding. For the Index options, I have another approach involving hedging with options.

So not really sure if this is the optimal approach or not, but it has saved me tonnes by not having to hedge more frequently.

Section 1:

This section lists status updates of the program. After every action taken by the program, a notification is displayed here for a quick view.

Section 2:

The inputs are displayed in this section when they are loaded from the program.

Section 3:

The real-time order status of carpet order, as well as subsequent orders, is shown here. Please refer to the strategy for the logic.

You can view the order status of BUY LONG orders on the top half and that of SELL SHORT orders on the bottom half of the section.

Section 4:

The real-time order status of stop-loss orders is shown here. Order types and the offsets are handled by the strategy logic based on market events.

Last edited: