I´m not expert at write code but i have some basic knowlodge of amibroker and Mestatock. I think i can translate the rules to both languages. Dont ask me about tradestation code.... i'm not that good.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

ETF (mostly) trading system development

- Thread starter QuantpTrader

- Start date

Can you run your system on a random selection of other ETFs? Choose a period that is as long as possible.

I usually do that test in related markets like (SPY, IWM or MDY) and see if the system makes profit and if the equity line have a positive slope. I dont expect to achieve the same results....

Also, i dont test the system in other non related markets because i dont follow the idea that one size fits all.

Basically the system have two parameters that can be optimized (i never change, with a small exception the ATR_STOP formula (in theory you could, but i choose not to do it), so i don’t considered it a parameter that can be optimized).

The parameters are:

The parameters are:

- The IBS threshold

- The number of days in the Highest High Close

In order to evaluate real time performance i will provide real-time signals on my twitter account under the hastag #QQQIBSM1.

From time to time i will also provide here the updated results of the system.

Any comments or critics? Or can we go to the next one?

From time to time i will also provide here the updated results of the system.

Any comments or critics? Or can we go to the next one?

#QQQIBSM1 system is on daily data. Entries are made on the open of next day after the signal. Exits are also on the next open day after the exit signal.

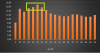

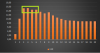

This is what you are competing against, QQQ buy and hold annual returns:

You are way under almost every year on your system so it is a lot of work and commission to underperform simple buy and hold. You started out beating it first 3 years then consistently underperformed so you need to rethink the strategy.

This is what you are competing against, QQQ buy and hold annual returns:

View attachment 189811

You are way under almost every year on your system so it is a lot of work and commission to underperform simple buy and hold. You started out beating it first 3 years then consistently underperformed so you need to rethink the strategy.

Thanks for feedback. Will elaborate more on this and the previous post later in the day, but the way you see it is one way, the way i seet it is that buy and hold had a negative performance of minus 15%.