You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Ecological Overshoot

- Thread starter Ricter

- Start date

"...stagnation and unemployment, booms and busts already plague economies worldwide, as a result of the inherent tendency to overproduce. Whether governments and economies continue with business as usual, or are turned inside out by ecological revolution, either way they could find themselves dealing with inflation, shortages of basic necessities, or other threats. In either case, rationing may become unavoidable. If it does, the way it happens — justly or harshly — will depend very much on whether we have managed to build a just society."

Any Way You Slice It

By Stan Cox

originally published by The Land Magazine

February 17, 2023

There are many ways of rationing scarce resources. Stan Cox examines their advantages and drawbacks.

"For many people, notably politicians, “rationing is a four-letter word”, never to be mentioned except in the context of the Second World War. Economists, on the other hand, employ the term “rationing” to denote any means of apportioning goods and the resources used to make them such as raw materials, energy or labour. “Rationing by price”, or by “willingness to pay”, refers to the apportioning of goods through market forces, ie through changes in the market price of a scarce factor or product. Prices direct resources towards more profitable uses by industry, and once industry has turned out commodities, prices ration the commodities among consumers. That is said to provide maximum benefit to society, because the ways in which people spend their money reflect what they believe will increase their own well being.

"However willingness to pay can only be expressed by those with the ability to pay. If there is a shortage of essential goods, and a portion of the population struggles even to meet minimum requirements, then rationing by price can create intolerable hardships. What happens when society decides collectively that it is not acceptable to have supplies dwindle, allows prices to rise and lets people scramble for what they need? Governments can build a floor under consumption, to secure basic needs at the bottom of the economy, and they often put a ceiling in place as well to conserve resources that would otherwise be consumed in excess by some.

"In other words they practice rationing by means other than price."

More...

Any Way You Slice It

By Stan Cox

originally published by The Land Magazine

February 17, 2023

There are many ways of rationing scarce resources. Stan Cox examines their advantages and drawbacks.

"For many people, notably politicians, “rationing is a four-letter word”, never to be mentioned except in the context of the Second World War. Economists, on the other hand, employ the term “rationing” to denote any means of apportioning goods and the resources used to make them such as raw materials, energy or labour. “Rationing by price”, or by “willingness to pay”, refers to the apportioning of goods through market forces, ie through changes in the market price of a scarce factor or product. Prices direct resources towards more profitable uses by industry, and once industry has turned out commodities, prices ration the commodities among consumers. That is said to provide maximum benefit to society, because the ways in which people spend their money reflect what they believe will increase their own well being.

"However willingness to pay can only be expressed by those with the ability to pay. If there is a shortage of essential goods, and a portion of the population struggles even to meet minimum requirements, then rationing by price can create intolerable hardships. What happens when society decides collectively that it is not acceptable to have supplies dwindle, allows prices to rise and lets people scramble for what they need? Governments can build a floor under consumption, to secure basic needs at the bottom of the economy, and they often put a ceiling in place as well to conserve resources that would otherwise be consumed in excess by some.

"In other words they practice rationing by means other than price."

More...

"While many Americans still doubt the existence of climate change or whether climate change represents a threat serious enough to spend billions to address, coastal communities across the country have already begun heeding the wake-up call issued by scientists. San Francisco is just one of several U.S. cities to seek help from the Army Corps of Engineers in recent years. Others include Charleston, S.C., Miami and Boston. As the reality of the situation and the costs associated with it continue to sink in, more and more cash-strapped communities will no doubt seek federal assistance."

See Also: Catabolic Collapse, in this thread.

San Francisco holds its breath to find out how much it will cost to protect its waterfront from sea level rise

David Knowles

·Senior Editor

Wed, February 22, 2023 at 3:00 AM MST·13 min read

San Francisco's waterfront. (Getty Images)

SAN FRANCISCO — On a brisk February morning, a portable orange traffic sign set up near the intersection of Mission Street and Embarcadero shuddered in the wind, blinking a warning to passing drivers: “Caution: King tides.”

Waves from San Francisco Bay now regularly breach the pier and spill into the streets at this spot during tidal surges and helped convince city officials that sea level rise caused by climate change is no longer a problem that can be ignored.

“It was into my second year that I realized that my whole job and the organization was going to do this work,” Port of San Francisco executive director Elaine Forbes, who was appointed to her position in 2016 by then-Mayor Ed Lee, said beneath the Ferry Building’s broken clock tower, its hands fixed to either high noon or midnight as it undergoes repairs. “You’re on the line of defense.”

A semi-independent entity, the port oversees 7.5 miles of the city’s coastal facilities along the bay, leasing out a wide array of properties, including landmarks like Fisherman’s Wharf, Pier 39, the Ferry Building, a cruise ship terminal and Oracle Park, where the Giants play baseball. Its revenues are crucial to the city’s bottom line, and in 2018 Forbes mobilized her office to help ensure the passage of Prop A, a voter initiative that raised $425 million in taxpayer funds to begin addressing repairs and seismic upgrades to a 3-mile section of the city’s crumbling, more-than-100-year-old sea wall in anticipation of sea level rise.

“We said at the time, this is really a down payment for the problem,” Forbes recounted.

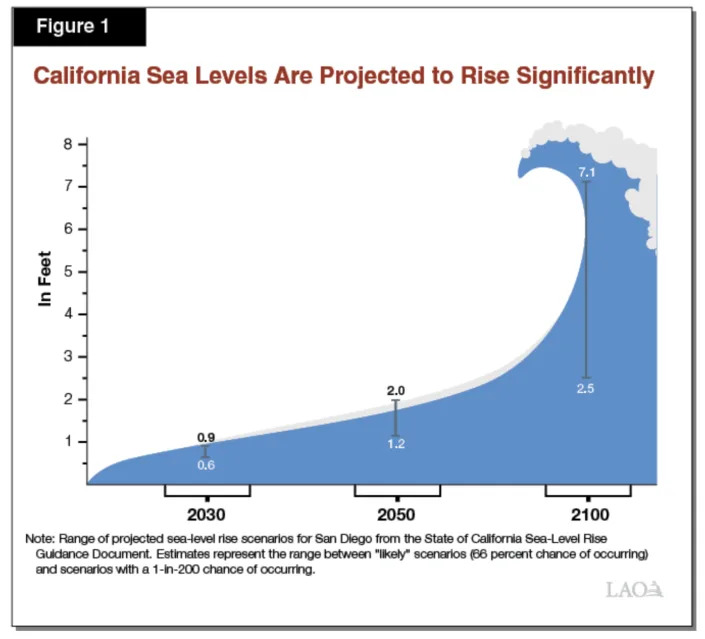

Since then, projections for how bad that problem will get have only become more dire. In 2020, the Legislative Analyst’s Office, the nonpartisan fiscal and policy adviser to the California Legislature, issued a report stating that under a scenario of continued high greenhouse gas emissions, San Francisco could see as much as 7 feet of sea level rise by 2100.

A graphic from a 2020 report by California's Legislative Analyst's Office.

In response to that grim new estimate, Forbes and the port’s commissioners announced last fall that they were partnering with the U.S. Army Corps of Engineers to conduct a comprehensive yearlong study examining how best to protect the vulnerable waterfront. Doing nothing, everyone seemed to agree, was not an option.

“The increased frequency of flooding that you’ll see as the bay comes up and you have more frequent tidal flooding, the numbers are in the billions in terms of the damages that will accumulate from that,” Brian Harper, a director of planning with the Army Corps, told Yahoo News.

But just as significant increases in sea level will result in monumental damages, adequately protecting communities from the additional rise will also become much more expensive. Complicating San Francisco’s efforts, the pandemic has badly diminished revenues from tourism and financial district foot traffic, forcing port officials to go hat-in-hand to city, state and federal entities in search of money to use to harden the coastline against rising waters.

“We’re not even at a scale to pretend to be able to pay for this project,” Forbes said. “We have a $114 million balance sheet, maybe a little higher. If we’re lucky, we have a $25 million capital budget that we squeeze out of our net revenues.”

More...

See Also: Catabolic Collapse, in this thread.

San Francisco holds its breath to find out how much it will cost to protect its waterfront from sea level rise

David Knowles

·Senior Editor

Wed, February 22, 2023 at 3:00 AM MST·13 min read

San Francisco's waterfront. (Getty Images)

SAN FRANCISCO — On a brisk February morning, a portable orange traffic sign set up near the intersection of Mission Street and Embarcadero shuddered in the wind, blinking a warning to passing drivers: “Caution: King tides.”

Waves from San Francisco Bay now regularly breach the pier and spill into the streets at this spot during tidal surges and helped convince city officials that sea level rise caused by climate change is no longer a problem that can be ignored.

“It was into my second year that I realized that my whole job and the organization was going to do this work,” Port of San Francisco executive director Elaine Forbes, who was appointed to her position in 2016 by then-Mayor Ed Lee, said beneath the Ferry Building’s broken clock tower, its hands fixed to either high noon or midnight as it undergoes repairs. “You’re on the line of defense.”

A semi-independent entity, the port oversees 7.5 miles of the city’s coastal facilities along the bay, leasing out a wide array of properties, including landmarks like Fisherman’s Wharf, Pier 39, the Ferry Building, a cruise ship terminal and Oracle Park, where the Giants play baseball. Its revenues are crucial to the city’s bottom line, and in 2018 Forbes mobilized her office to help ensure the passage of Prop A, a voter initiative that raised $425 million in taxpayer funds to begin addressing repairs and seismic upgrades to a 3-mile section of the city’s crumbling, more-than-100-year-old sea wall in anticipation of sea level rise.

“We said at the time, this is really a down payment for the problem,” Forbes recounted.

Since then, projections for how bad that problem will get have only become more dire. In 2020, the Legislative Analyst’s Office, the nonpartisan fiscal and policy adviser to the California Legislature, issued a report stating that under a scenario of continued high greenhouse gas emissions, San Francisco could see as much as 7 feet of sea level rise by 2100.

A graphic from a 2020 report by California's Legislative Analyst's Office.

In response to that grim new estimate, Forbes and the port’s commissioners announced last fall that they were partnering with the U.S. Army Corps of Engineers to conduct a comprehensive yearlong study examining how best to protect the vulnerable waterfront. Doing nothing, everyone seemed to agree, was not an option.

“The increased frequency of flooding that you’ll see as the bay comes up and you have more frequent tidal flooding, the numbers are in the billions in terms of the damages that will accumulate from that,” Brian Harper, a director of planning with the Army Corps, told Yahoo News.

But just as significant increases in sea level will result in monumental damages, adequately protecting communities from the additional rise will also become much more expensive. Complicating San Francisco’s efforts, the pandemic has badly diminished revenues from tourism and financial district foot traffic, forcing port officials to go hat-in-hand to city, state and federal entities in search of money to use to harden the coastline against rising waters.

“We’re not even at a scale to pretend to be able to pay for this project,” Forbes said. “We have a $114 million balance sheet, maybe a little higher. If we’re lucky, we have a $25 million capital budget that we squeeze out of our net revenues.”

More...

Would be awesome if someone would overlay that with solar activity (max/min). Obviously wouldn't be the cause of the spike at the end, but would be interested how it affects the volatility.

I'm just WAG here, but I'd guess the cooling you see from 800 to 1500 is related to Milankovitch cycles and cosmic rays. The solar activity cycle is about 11 years, so maybe that is visible.Would be awesome if someone would overlay that with solar activity (max/min). Obviously wouldn't be the cause of the spike at the end, but would be interested how it affects the volatility.

"Most current debt is, in effect, a bet on future growth. But future growth is increasingly problematic. As I have explained elsewhere (in this book and in this article), global growth is coming to an end in the first decades of the current century due to depletion of fossil fuels and other resources, rising pollution levels, and declining population growth. China, whose population has started shrinking and whose recently spectacular levels of economic growth are now rapidly tapering off, is a global bellwether. High levels of global debt are likely to turn what could be a controllable shift from expansion to contraction into a blowout of unfulfilled expectations and obligations, leading to widespread suffering."

Converging Debt Crises

By Richard Heinberg, originally published by Resilience.org

February 22, 2023

An enormous debt bomb threatens the US federal government and the nation’s financial system unless warring politicians can agree on a plan to defuse it. However, there are even bigger debt bombs ticking away beneath us all, of which fewer people are aware. It may be impossible to disarm all of them, but action is required to minimize the casualties.

Let’s start by focusing on the immediate US debt threat, then widen our view to take in longer-term and more serious liabilities that have the potential to bring down the entire global industrial economy.

Congressional Hostage Takers

The United States government reached its congressionally mandated legal debt limit, $31.4 trillion, on January 19th. This debt represents past spending: cutting the budget now won’t make the debt go away. If Congress fails to raise the debt limit, the federal government could default on its debt payments—something it has never done before.

The federal debt limit was created by Congress in 1917. In recent decades, there have been periodic standoffs (in 1985, 1997, 2011, and 2013), in which Republicans threatened to let the deadline to increase the limit pass unless Democrats agreed to spending cuts in social programs. Neither side actually wanted the federal government to default, but brinksmanship served partisan interests. This time, some Republican House Freedom Caucus members appear to regard an actual debt default (not just the threat of one) as a useful tool to force major government spending cuts.

Government spending comes in three large categories—mandatory, discretionary, and interest payments. Most federal spending is mandatory, including Social Security and Medicare payments. Of discretionary spending, defense accounts for more than half. Interest payments on US debt comprise the smallest of the three categories of spending, but it is growing fast and may overtake the military budget by 2025 or 2026.

Some pundits equate debt ceiling fights with hostage negotiations. In this instance, House Speaker McCarthy may have limited ability to prevent his more radical colleagues from metaphorically shooting their captive. McCarthy’s leadership is fragile and in order to gain it, he agreed to rules that will give extremists outsized influence in upcoming negotiations. A single member will be able to force a vote on the speakership, possibly plunging the entire body back into days of voting to establish a new leader.

Since US debt (in the form of bonds and other securities) anchors the global financial system, a default could rattle economies across the globe. Americans could face a recession, and stock and bond markets would likely plunge. Still, exactly how a default would play out is uncertain. Since the US government’s payment of its financial obligations is mandated in the US constitution, it is conceivable that a default could be averted by the courts. Nevertheless, there is a very real possibility that not only Americans, but millions or billions around the globe could face hardship as a result of political hardball tactics playing out in Washington DC.

The debt ceiling standoff in America is unquestionably a volatile situation, but it’s only one aspect of the larger debt crisis facing humanity.

According to the late anthropologist David Graeber, debt has been around for about five thousand years. Debt is the flipside of money: especially in the modern world, where almost all money is created via bank loans, it’s impossible to have one without the other. In societies that use money, a pattern has played out again and again. At first, debt and money enable the expansion of trade and the creation of wealth. Then debt begins to accumulate faster than the ability to repay it, simply because it’s physically easier to borrow and spend than it is to extract resources and transform them with labor. Finally, a round of debt defaults destroys money and real wealth, leading to widespread misery. Eventually, the cycle begins again.

Over the past two centuries, and especially since 1950, the world has seen the highest rate of production of goods and services in all history. While technology played a role, the key enabler was cheap, abundant energy from fossil fuels. During this period, GDP was generally adopted as a measure of economic success, and growth became normalized. Because it was assumed that the economy would continue to grow, it was generally believed that most debt incurred now could be repaid in the future. Further, increasing household debt (including credit card debt, mortgages, and student loans) enabled most people to consume now and pay later, and helped expand the whole economy.

More...

Converging Debt Crises

By Richard Heinberg, originally published by Resilience.org

February 22, 2023

An enormous debt bomb threatens the US federal government and the nation’s financial system unless warring politicians can agree on a plan to defuse it. However, there are even bigger debt bombs ticking away beneath us all, of which fewer people are aware. It may be impossible to disarm all of them, but action is required to minimize the casualties.

Let’s start by focusing on the immediate US debt threat, then widen our view to take in longer-term and more serious liabilities that have the potential to bring down the entire global industrial economy.

Congressional Hostage Takers

The United States government reached its congressionally mandated legal debt limit, $31.4 trillion, on January 19th. This debt represents past spending: cutting the budget now won’t make the debt go away. If Congress fails to raise the debt limit, the federal government could default on its debt payments—something it has never done before.

The federal debt limit was created by Congress in 1917. In recent decades, there have been periodic standoffs (in 1985, 1997, 2011, and 2013), in which Republicans threatened to let the deadline to increase the limit pass unless Democrats agreed to spending cuts in social programs. Neither side actually wanted the federal government to default, but brinksmanship served partisan interests. This time, some Republican House Freedom Caucus members appear to regard an actual debt default (not just the threat of one) as a useful tool to force major government spending cuts.

Government spending comes in three large categories—mandatory, discretionary, and interest payments. Most federal spending is mandatory, including Social Security and Medicare payments. Of discretionary spending, defense accounts for more than half. Interest payments on US debt comprise the smallest of the three categories of spending, but it is growing fast and may overtake the military budget by 2025 or 2026.

Some pundits equate debt ceiling fights with hostage negotiations. In this instance, House Speaker McCarthy may have limited ability to prevent his more radical colleagues from metaphorically shooting their captive. McCarthy’s leadership is fragile and in order to gain it, he agreed to rules that will give extremists outsized influence in upcoming negotiations. A single member will be able to force a vote on the speakership, possibly plunging the entire body back into days of voting to establish a new leader.

Since US debt (in the form of bonds and other securities) anchors the global financial system, a default could rattle economies across the globe. Americans could face a recession, and stock and bond markets would likely plunge. Still, exactly how a default would play out is uncertain. Since the US government’s payment of its financial obligations is mandated in the US constitution, it is conceivable that a default could be averted by the courts. Nevertheless, there is a very real possibility that not only Americans, but millions or billions around the globe could face hardship as a result of political hardball tactics playing out in Washington DC.

The debt ceiling standoff in America is unquestionably a volatile situation, but it’s only one aspect of the larger debt crisis facing humanity.

According to the late anthropologist David Graeber, debt has been around for about five thousand years. Debt is the flipside of money: especially in the modern world, where almost all money is created via bank loans, it’s impossible to have one without the other. In societies that use money, a pattern has played out again and again. At first, debt and money enable the expansion of trade and the creation of wealth. Then debt begins to accumulate faster than the ability to repay it, simply because it’s physically easier to borrow and spend than it is to extract resources and transform them with labor. Finally, a round of debt defaults destroys money and real wealth, leading to widespread misery. Eventually, the cycle begins again.

Over the past two centuries, and especially since 1950, the world has seen the highest rate of production of goods and services in all history. While technology played a role, the key enabler was cheap, abundant energy from fossil fuels. During this period, GDP was generally adopted as a measure of economic success, and growth became normalized. Because it was assumed that the economy would continue to grow, it was generally believed that most debt incurred now could be repaid in the future. Further, increasing household debt (including credit card debt, mortgages, and student loans) enabled most people to consume now and pay later, and helped expand the whole economy.

More...