I am relatively new to options trading and have one question regarding theta:

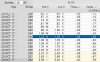

SPY is closed at $249.19 today. In thinkorswim, in October expiry, ATM strike 249P shows a theta of 0.03, smaller than 0.04 theta of OTM strike 245P, in terms of absolute value. Is this reasonable? I thought the ATM strike should decay faster than OTM strike...

Does this mean that if I make this bullish OTM vertical +245P/-249P, I will be suffering theta decay with passage of time (assuming IV and underlying price do not change)?

SPY is closed at $249.19 today. In thinkorswim, in October expiry, ATM strike 249P shows a theta of 0.03, smaller than 0.04 theta of OTM strike 245P, in terms of absolute value. Is this reasonable? I thought the ATM strike should decay faster than OTM strike...

Does this mean that if I make this bullish OTM vertical +245P/-249P, I will be suffering theta decay with passage of time (assuming IV and underlying price do not change)?