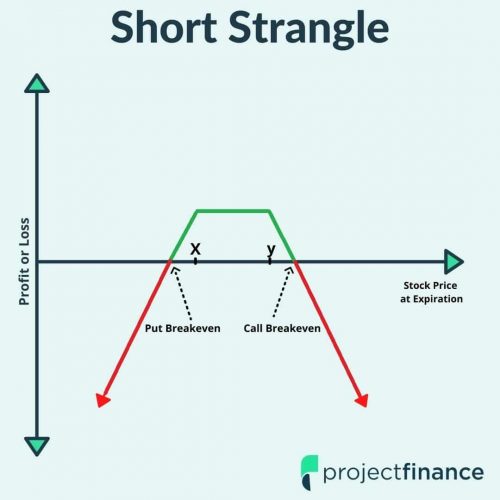

The above demonstrated strategies (Long Butterfly etc) belong to the class of options spread strategies.

Such spread strategies prevent against total loss as well against unlimited loss by automatically capping (cutting) the losses.

One can tailor such a construct oneself by choosing different strikes etc., thereby tailoring the risk/reward profile.

Such an options spread can be created by using Calls, Puts, or both combined, cf. above link.

See also https://en.wikipedia.org/wiki/Options_strategy

Such spread strategies prevent against total loss as well against unlimited loss by automatically capping (cutting) the losses.

One can tailor such a construct oneself by choosing different strikes etc., thereby tailoring the risk/reward profile.

Such an options spread can be created by using Calls, Puts, or both combined, cf. above link.

See also https://en.wikipedia.org/wiki/Options_strategy

Last edited:

") Sometimes even a profit as the minimum, ie. arbitrage

Sometimes even a profit as the minimum, ie. arbitrage