I re-read an old post from acrary which stressed the importance of being consistently profitable over a certain interval. It made a lot of sense to me to approach profitability in this way because it's logically the only way you can trade for a living. If you don't get a paycheck each week, you miss your rent or eat less- it's not just some arbitrary number.

I took an algorithmic approach so that an automated system could hypothetically calculate trading goals for itself. I created a stochastic model of net weekly trading results to find out the required profit factor, winning percentage, and trade frequency to be confident, with statistical certainty, that a system will not lose money.

At the end of each week you look at your results to see if your system is performing normally or not. Abnormal and normal are based on confidence intervals so it is not an emotional decision to cut a system off after a drawdown.

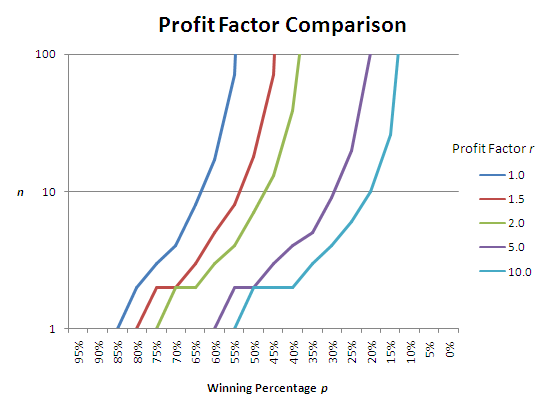

Here's a chart of the results, the curves are the minimum profit factor (r), trade frequency (n), and winning percentage (p) to be consistently profitable with 90% certainty:

You can see that it is crucial to have a decent winning percentage unless your system can generate hundreds of signals to trade on each week. The number of trades required per week is actually exponential with the decreasing winning percentage. It is apparent that it is better to have a system that makes a few good trades per week rather than one that frequently miscalls trends.

I was wondering how you all determine targets for your system- it seems illogical to rely on a system to remove the emotional factor from trading when the assumptions it's based on are gut feelings. Do you use Monte Carlo VaR analysis instead of variance-covariance? Do you use a different mathematical model?

Details of my model-derivation thought process are in this word file and this excel table (warning: Math)

Regards,

Max

__________________

maxdama.com - The log of my research on and implementation of automated trading strategies

I took an algorithmic approach so that an automated system could hypothetically calculate trading goals for itself. I created a stochastic model of net weekly trading results to find out the required profit factor, winning percentage, and trade frequency to be confident, with statistical certainty, that a system will not lose money.

At the end of each week you look at your results to see if your system is performing normally or not. Abnormal and normal are based on confidence intervals so it is not an emotional decision to cut a system off after a drawdown.

Here's a chart of the results, the curves are the minimum profit factor (r), trade frequency (n), and winning percentage (p) to be consistently profitable with 90% certainty:

You can see that it is crucial to have a decent winning percentage unless your system can generate hundreds of signals to trade on each week. The number of trades required per week is actually exponential with the decreasing winning percentage. It is apparent that it is better to have a system that makes a few good trades per week rather than one that frequently miscalls trends.

I was wondering how you all determine targets for your system- it seems illogical to rely on a system to remove the emotional factor from trading when the assumptions it's based on are gut feelings. Do you use Monte Carlo VaR analysis instead of variance-covariance? Do you use a different mathematical model?

Details of my model-derivation thought process are in this word file and this excel table (warning: Math)

Regards,

Max

__________________

maxdama.com - The log of my research on and implementation of automated trading strategies

Easier said than done?? well you can only know it when you trade with real money..

Easier said than done?? well you can only know it when you trade with real money..