You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Best Santelli Rant in a while..

- Thread starter Tsing Tao

- Start date

Quote from Martinghoul:

I am back... I am sorry that I disappeared, but I had family matters that required my attention.

I am now back and happy to conclude our conversation, if you so desire.

Sure, if you'd like to re-engage, I welcome it. Even if the post is quite old. We have so little engagement of anything around here on economics, it's quite novel.

You essentially said Santelli knew nothing about anything he says. So, in this particular video - removing the stuff no one can prove (which is speculation on elections, etc) what is incorrect?

Quote from Ricter:

Looks like you were, too.

Trolling in my own thread, eh? That's a new one.

The guy attacks Santelli with no supporting evidence, just calling him a failed trader, and I state how unsurprised he'd show up to defend the Fed (indirectly, since Santelli is going against him). You, on the other hand, are just looking to pick your usual fight.

Quote from Maverick74:

Martin, I think you would fit in very nicely down here. You have perfected the art of not answering the question well. That's how threads down here get 100 pages long when they really only need to be one page. You get 100 pages of guys not answering questions.")

I have a soft spot for Brits Martin. Albeit mostly British actresses which I assume you don't qualify. But I'll overlook that for the time being. LOL.

I don't think Lucrum or anyone else down here agrees with someone just because they are loud and shouting. Chris Matthews seems to shout a lot. James Cramer shouts a lot. Hell our President shouts a lot. I have a funny feeling that those who agree with the Rickster are really agreeing to his point of view, not his inflection points. I could be wrong of course.

So the shouting aside and the background aside, what exactly are you disagreeing with Rick about? Part of having a debate means both parties have to actually debate. LOL. Your argument about Rick's background is irrelevant because we don't know who you are and quite frankly, we don't really know Rick either. We can pretend we know him because he is on TV every day. And we can pretend to know him reading a one paragraph synopsis on his life. But we don't really "know" him. So that debate will never go anywhere because it will come down to subjective interpretation and built in prejudices that we have for such person.

So let's debate the issue. Again I will ask, what "specifically" are you disagreeing with Rick about? And yes Martin, just pretend for the time being that I'm really big into details. I don't want to have to "guess" what you really think. I truly believe that three times is a charm. Don't disappoint me.

Martin, don't leave me hanging for another year. Why don't you start with responding to where we left off a year ago....

Please pay close attention to the last paragraph. It will allow you to properly structure your answer in a way I'll find more satisfactory. Good luck chap!

For you, anything, amico Mav, although maybe the patronizing tone is a little overdone. Still, I ain't sore. I am a big boy, I can handle it.Quote from Maverick74:

Martin, don't leave me hanging for another year. Why don't you start with responding to where we left off a year ago....

Please pay close attention to the last paragraph. It will allow you to properly structure your answer in a way I'll find more satisfactory. Good luck chap!

1. I disagree with Rick about his analogy. QE is not like using a firehose to water a tiny geranium plant. The US economy isn't tiny and neither is the US mtge mkt.

2. I disagree with Rick about this concept of collateral damage, even though he was not specific enough. I don't know where he sees this damage and why Rick, of all people, is uniquely qualified to define what's "damage" and what isn't.

3. I note that Rick didn't have a specific response to El-Erian's valid question, which, in my view, is a question a trader would ask. Instead, Rick responded as a journalist would, with a witticism. This ties in with the point above.

4. I disagree with Rick on his reflation idea that somewhere, at some indeterminate point in the future, there will be some ginormous inflation that will turn our sirloins into $1 cheeseburgers. There's just no evidence of this and the markets, which I would argue know best, have never priced any sort of runaway inflation. But, of course, Rick knows best.

5. I have absolutely no idea why there's a discussion, within the same context, of the "Solyndras" and the GM bailout. I don't see what that has to do with the QE3 topic.

6. I am not going to comment on Rick's political commentary and leanings. I don't do US politics.

7. Again, when he was asked to give his prediction of the effect of Romney winning and appointing Taylor, Rick responded like a journalist, rather than a trader. He didn't say anything specific whatsoever. On China, it was another witty bit of fluff. On the impact of Bernanke being replaced, it was "I am sure they're gonna manage it".

Is that to your liking? I suppose some of these points aren't disagreements per se, but that is solely because Rick didn't provide any substance in his commentary that I could possibly disagree with.

EDIT: And happy 4th of July to y'all, btw!

Martin...old chap...first of all, no patronizing tone here, sorry if it came off that way. You did disappear for a year. But anyway, you have no idea how excited I get at the thought of a possibility of an intelligent conversation here, so I will do my best not to ruin it.

OK, let me just address some raw points here that Rick may or may not have made but go along with the spirit of his argument regarding the Fed and our monetary policy.

First of all, on the issue of inflation, we have TONS of it. Not in the cpi data. Inflation no longer permeates cpi for a whole hosts of reasons. Let me tell you where inflation is showing itself:

1) housing prices. Yes, even at these depressed levels. If you measure housing prices here in the states as a function of avg income you will find that the ratio is as wide today as it's ever been. People today have to take out far bigger loans and use far more leverage to buy the same homes that their parents bought 40 years ago for cash and no leverage. That's not good martin.

2) risk asset prices. Excess money supply has been flowing into assets, not goods. So the price of goods are not going up, but stocks are, diamonds are, art is, high end real estate is at record levels, etc.

3) college education. The cost of education in this country is going through the roof. One way to think of education is that it behaves similarly to a stock. An education is really an investment, just like AAPL. You buy it hoping to get a long term return. So money is chasing higher education just as it's chasing the s&p 500. The middle class here has almost completely been priced out of the market. Again, without resorting to taking on obscene amounts of debt. Martin, 50 years ago in this country it was unheard of to take out debt to go to college. Our parents worked part time jobs at school or over the summer and that almost COMPLETELY paid for school. Now graduates are leaving school with 100k to 150k in debt. Inflation.

4) Healthcare. Healthcare costs are going vertical. Now, many will point out that is simply due to the efficiency of lack there of in our system and that certainly is a part of it. But the real devil here is that anything that is strongly demanded, has a sharp sensitivity to inflation. So risk assets, college, healthcare, all have high sensitivities to demand.

5) Food. Now some will point out that the cpi data shows that food prices are holding steady. I try not to laugh at this. Yes, our genetically modified, artificial food that is mass processed is holding steady. But good, healthy food in this country has seen prices skyrocket. It's sad that today in America a middle class family cannot afford healthy food. And our government keeps subsidizing corn and other cheap byproducts to hide the real cost of food. This is why our inflation is showing up in our waste lines.

The bottom line is, in order to live the same quality of life today as our parents, we need to borrow more, leverage more, eat cheaper food, go with less healthcare and forgo college to end up with the SAME dollars as before. This is called inflation Martin. Inflation can be manipulated many ways. It doesn't have to mean an increase in price. It can mean price stays flat but quality or access goes down. Same difference.

So there ARE consequences to unlimited printing of money. We further see this play out with the gap between the rich and the poor. Many like to think we have a wage gap or salary gap in this country. This is laughable of course because the rich don't earn wages or even salaries. The rich own. They own land, investments, art, jewelry, metals, natural resources, etc. So we have this bifurcated society where one end has wealth that is increasing every year at a compounded growth rate thanks to inflation. We have the other end that owns nothing and owes everything. They are drowning in debt. Why? Because debt is the only thing that allows them to purchase the things they need to live. The same things that their parents simply paid cash for. So one end see their net worth growing every year thanks to the Fed, the other goes deeper and deeper into the red.

You'll notice Martin that in societies that have no central banks, this wealth gap is almost non existent. Of course the politicians here think that raising minimum wage a dollar an hour will close that gap. LOL. Yeah, OK, let's keep politics out of this for now.

Now let's move on to the mortgage market. You say the mortgage market is not small. That's actually not true. The mortgage market is very small. What is large is the mortgage back securities market. BIG difference. Yes, we have created derivatives upon derivatives upon derivatives that leverage existing mortgage debt and actually create synthetic mortgage debt that doesn't even exist. So yes, you are correct, the derivatives market is huge. But the underlying market is not that big. Not after you subtract out real equity that is embedded in the product.

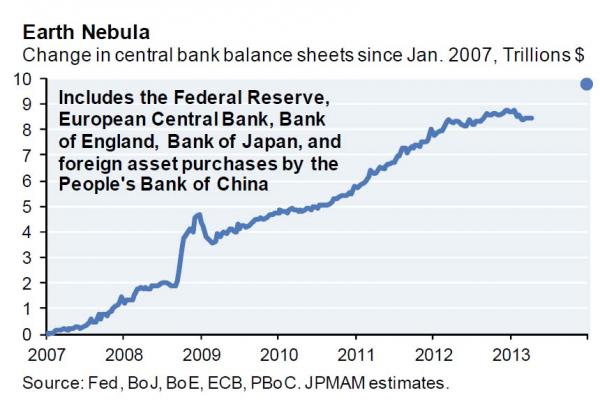

Martin, if we take a step back here, we need to ask ourselves how was it, that for the last 100 years up until about 2008, the combined balance sheets of ALL central banks around the world never exceeded even a trillion dollars. Not during all the wars, the famine, the riots, the depressions, recessions, assassinations, droughts, epidemics, etc, we never had to leverage ourselves to this degree. But in the last 5 years, the central banks around the world now carry over 13 trillion, yes trillion, on their balance sheets. Why is that Martin? What has systemically changed to warrant this? How were we able to go this long without printing money but today, if we don't do it, the world is going to end?

So what has this done for us Martin? Why is it that we have printed all this money yet still have no job growth, middle class affordability gone, quality of life on the downturn and supposedly, the whole house of cards will collapse if we stop printing. What's the end game here Martin? How rich can the rich get? At what point do we just say OK, the rich own everything and the other 99% will just live off welfare and benefits. You know that is where we are headed. There is no way the middle class can buy in at this point. Prices keep rising and are far out of reach. If the middle class man wants to pretend he is a member of the club, he has to go into debt and hope the bank doesn't call in the loan.

OK, let me address your last comment about Solyndra, et al. The reason Rick brought that up was because of the concept of moral hazard. The idea that the government or banks can take risks with no consequences. It's an open door to corruption at worst and inefficiency at best. Same is true with our central banks. If they never have to pay the price of being wrong, then what is going to stop them. Society has always had a way of correcting it's wrong. This happens either through nature or through nurture. It's what creates a long term equilibrium in the world. You produce too much, prices go down. You produce too little, prices go up. And somewhere in the middle you find your efficiency. But what if these rules didn't apply anymore? What if one could take risk with no consequences? What if one could step around the law with no consequences. What if one would never be held accountable for their actions and behavior? Then the equilibrium breaks. And we get disequilibrium. We get a society of extremes. We get a market with no real value. Prices are manufactured for show. This is a scary world we are headed into Martin. Rick is asking valid questions. He likes to shout. He may have an agenda. But the questions are valid. The smartest people in the world who are looking at this problem, the best answer they can come up with is, they are absolutely clueless as to how this is going to end. People like Soros, Bill Gross, Jeremy Granthem, Jim Grant, etc. all believe this will end badly.

So Martin, what says you? Your serve.

OK, let me just address some raw points here that Rick may or may not have made but go along with the spirit of his argument regarding the Fed and our monetary policy.

First of all, on the issue of inflation, we have TONS of it. Not in the cpi data. Inflation no longer permeates cpi for a whole hosts of reasons. Let me tell you where inflation is showing itself:

1) housing prices. Yes, even at these depressed levels. If you measure housing prices here in the states as a function of avg income you will find that the ratio is as wide today as it's ever been. People today have to take out far bigger loans and use far more leverage to buy the same homes that their parents bought 40 years ago for cash and no leverage. That's not good martin.

2) risk asset prices. Excess money supply has been flowing into assets, not goods. So the price of goods are not going up, but stocks are, diamonds are, art is, high end real estate is at record levels, etc.

3) college education. The cost of education in this country is going through the roof. One way to think of education is that it behaves similarly to a stock. An education is really an investment, just like AAPL. You buy it hoping to get a long term return. So money is chasing higher education just as it's chasing the s&p 500. The middle class here has almost completely been priced out of the market. Again, without resorting to taking on obscene amounts of debt. Martin, 50 years ago in this country it was unheard of to take out debt to go to college. Our parents worked part time jobs at school or over the summer and that almost COMPLETELY paid for school. Now graduates are leaving school with 100k to 150k in debt. Inflation.

4) Healthcare. Healthcare costs are going vertical. Now, many will point out that is simply due to the efficiency of lack there of in our system and that certainly is a part of it. But the real devil here is that anything that is strongly demanded, has a sharp sensitivity to inflation. So risk assets, college, healthcare, all have high sensitivities to demand.

5) Food. Now some will point out that the cpi data shows that food prices are holding steady. I try not to laugh at this. Yes, our genetically modified, artificial food that is mass processed is holding steady. But good, healthy food in this country has seen prices skyrocket. It's sad that today in America a middle class family cannot afford healthy food. And our government keeps subsidizing corn and other cheap byproducts to hide the real cost of food. This is why our inflation is showing up in our waste lines.

The bottom line is, in order to live the same quality of life today as our parents, we need to borrow more, leverage more, eat cheaper food, go with less healthcare and forgo college to end up with the SAME dollars as before. This is called inflation Martin. Inflation can be manipulated many ways. It doesn't have to mean an increase in price. It can mean price stays flat but quality or access goes down. Same difference.

So there ARE consequences to unlimited printing of money. We further see this play out with the gap between the rich and the poor. Many like to think we have a wage gap or salary gap in this country. This is laughable of course because the rich don't earn wages or even salaries. The rich own. They own land, investments, art, jewelry, metals, natural resources, etc. So we have this bifurcated society where one end has wealth that is increasing every year at a compounded growth rate thanks to inflation. We have the other end that owns nothing and owes everything. They are drowning in debt. Why? Because debt is the only thing that allows them to purchase the things they need to live. The same things that their parents simply paid cash for. So one end see their net worth growing every year thanks to the Fed, the other goes deeper and deeper into the red.

You'll notice Martin that in societies that have no central banks, this wealth gap is almost non existent. Of course the politicians here think that raising minimum wage a dollar an hour will close that gap. LOL. Yeah, OK, let's keep politics out of this for now.

Now let's move on to the mortgage market. You say the mortgage market is not small. That's actually not true. The mortgage market is very small. What is large is the mortgage back securities market. BIG difference. Yes, we have created derivatives upon derivatives upon derivatives that leverage existing mortgage debt and actually create synthetic mortgage debt that doesn't even exist. So yes, you are correct, the derivatives market is huge. But the underlying market is not that big. Not after you subtract out real equity that is embedded in the product.

Martin, if we take a step back here, we need to ask ourselves how was it, that for the last 100 years up until about 2008, the combined balance sheets of ALL central banks around the world never exceeded even a trillion dollars. Not during all the wars, the famine, the riots, the depressions, recessions, assassinations, droughts, epidemics, etc, we never had to leverage ourselves to this degree. But in the last 5 years, the central banks around the world now carry over 13 trillion, yes trillion, on their balance sheets. Why is that Martin? What has systemically changed to warrant this? How were we able to go this long without printing money but today, if we don't do it, the world is going to end?

So what has this done for us Martin? Why is it that we have printed all this money yet still have no job growth, middle class affordability gone, quality of life on the downturn and supposedly, the whole house of cards will collapse if we stop printing. What's the end game here Martin? How rich can the rich get? At what point do we just say OK, the rich own everything and the other 99% will just live off welfare and benefits. You know that is where we are headed. There is no way the middle class can buy in at this point. Prices keep rising and are far out of reach. If the middle class man wants to pretend he is a member of the club, he has to go into debt and hope the bank doesn't call in the loan.

OK, let me address your last comment about Solyndra, et al. The reason Rick brought that up was because of the concept of moral hazard. The idea that the government or banks can take risks with no consequences. It's an open door to corruption at worst and inefficiency at best. Same is true with our central banks. If they never have to pay the price of being wrong, then what is going to stop them. Society has always had a way of correcting it's wrong. This happens either through nature or through nurture. It's what creates a long term equilibrium in the world. You produce too much, prices go down. You produce too little, prices go up. And somewhere in the middle you find your efficiency. But what if these rules didn't apply anymore? What if one could take risk with no consequences? What if one could step around the law with no consequences. What if one would never be held accountable for their actions and behavior? Then the equilibrium breaks. And we get disequilibrium. We get a society of extremes. We get a market with no real value. Prices are manufactured for show. This is a scary world we are headed into Martin. Rick is asking valid questions. He likes to shout. He may have an agenda. But the questions are valid. The smartest people in the world who are looking at this problem, the best answer they can come up with is, they are absolutely clueless as to how this is going to end. People like Soros, Bill Gross, Jeremy Granthem, Jim Grant, etc. all believe this will end badly.

So Martin, what says you? Your serve.

Quote from Martinghoul:

For you, anything, amico Mav, although maybe the patronizing tone is a little overdone. Still, I ain't sore. I am a big boy, I can handle it.

1. I disagree with Rick about his analogy. QE is not like using a firehose to water a tiny geranium plant. The US economy isn't tiny and neither is the US mtge mkt.

I don't believe Rick was comparing the US economy to the plant. I think he was saying that the Fed's fire hose was an enormous amount of water that was only achieving a tiny bit of benefit.

Quote from Martinghoul:

2. I disagree with Rick about this concept of collateral damage, even though he was not specific enough. I don't know where he sees this damage and why Rick, of all people, is uniquely qualified to define what's "damage" and what isn't.

You see no evidence of bubbles anywhere in the world's economy? Really?

Quote from Martinghoul:

3. I note that Rick didn't have a specific response to El-Erian's valid question, which, in my view, is a question a trader would ask. Instead, Rick responded as a journalist would, with a witticism. This ties in with the point above.

He answered it, even if you didn't like it. EE asked at what point do you tell investors to focus on the collateral damage, and Rick said they'll focus on it when they're drowning in liquidity - when it's too late. That's what I got. I suppose you can read whatever you want from it.

Quote from Martinghoul:

4. I disagree with Rick on his reflation idea that somewhere, at some indeterminate point in the future, there will be some ginormous inflation that will turn our sirloins into $1 cheeseburgers. There's just no evidence of this and the markets, which I would argue know best, have never priced any sort of runaway inflation. But, of course, Rick knows best.

It's rather difficult for the bond market to price anything in when the Fed is controlling it quite well with massive purchases, no? I mean, how can rates signal trouble ahead when the Fed is essentially keeping rates down?

Quote from Martinghoul:

5. I have absolutely no idea why there's a discussion, within the same context, of the "Solyndras" and the GM bailout. I don't see what that has to do with the QE3 topic.

Nor do I.

Quote from Martinghoul:

7. Again, when he was asked to give his prediction of the effect of Romney winning and appointing Taylor, Rick responded like a journalist, rather than a trader. He didn't say anything specific whatsoever. On China, it was another witty bit of fluff. On the impact of Bernanke being replaced, it was "I am sure they're gonna manage it".

He is a journalist. The guy has a 4 minute slot to complete his text, so I'm sure he'd like to be a bit more verbose, but time doesn't allow it. That doesn't diminish the weight of the message, as long as you're willing to listen to it and not just write it off because you don't personally like the guy.