You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Artificial Algorithmic Systems Real Trading

- Thread starter Alis

- Start date

Some changes after the weekend:

System 230903_24817_BN: position in ffi (1300 shares) taken by system 230904_41122_B at price 1.29

System 230904_34353_BN: position in ffi (2513 shares) taken by system 230913_22290_B at price 1.29

System 230905_8818_B: position in awm (10771 shares) taken by system 230913_22290_B at price 0.2645

System 230905_51054_B: position in asm (4615 shares) taken by system 230904_41122_B at price 1.47

System 230904_77676_B: position in asm (3323 shares) taken by system 230913_22290_B at price 1.47

System 230905_86730_BN: position in 3rg (6382 shares) taken by system 230913_22290_B at price 0.467

System 230905_51054_B: position in res (5156 shares) taken by system 230913_22290_B at price 0.578

System 230904_37848_B: position in res (5156 shares) taken by system 230905_20948_BN at price 0.578

I will use only five systems from now, more explanation later on.

System 230903_24817_BN: position in ffi (1300 shares) taken by system 230904_41122_B at price 1.29

System 230904_34353_BN: position in ffi (2513 shares) taken by system 230913_22290_B at price 1.29

System 230905_8818_B: position in awm (10771 shares) taken by system 230913_22290_B at price 0.2645

System 230905_51054_B: position in asm (4615 shares) taken by system 230904_41122_B at price 1.47

System 230904_77676_B: position in asm (3323 shares) taken by system 230913_22290_B at price 1.47

System 230905_86730_BN: position in 3rg (6382 shares) taken by system 230913_22290_B at price 0.467

System 230905_51054_B: position in res (5156 shares) taken by system 230913_22290_B at price 0.578

System 230904_37848_B: position in res (5156 shares) taken by system 230905_20948_BN at price 0.578

I will use only five systems from now, more explanation later on.

In the first post I mentioned that I’m using 600 trading systems. Of course, I wouldn’t take all the trades as it would be way too many to keep track of. During demo trading (the first half of 2023) I scored the signals based on the sum of the scores of systems that give “Buy” signal for given stock. This worked beautifully. I also liked the fact that it gave me so many signals – I could miss one here or there and it didn’t matter.

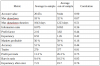

But recently I’ve checked correlation between in-sample trading and out-of-sample for various metrics. This is shown in attached file.

Two highest correlations are for final account value and bars-in ratio. (Bars-in ratio is just percentage of bars when a system has a trade opened. So 10 markets with 100 bars history would be 1000 bars. If a system has a trade opened in any 10 bars then bars-in ratio would be 1%).

Back to why I decided to trade only 5 best systems (based on in-sample performance):

The top 5 systems' out-of-sample average account value is around 38 times more than initial value (in other words, an average profit is about 3800% since 2018). More interesting is the sum of bars-in ratios: it’s just 26%. That means, that on average I will have invested only about a quarter of working capital. Unused capital will probably go to some ETFs, bonds or something similar. Of course, it’s possible that I will get more signals and I won’t be able to take them all, but I’m not worried and I’ll decide what to do when it actually happens.

This also means there are some changes to my position sizing: each trade is now about 2000 PLN. With 5 systems it means I can take about 10 trades for each system. Right now, I have around 20 signals so there is room for more.

I will slowly exit old systems at my discretion (or when actual exit signal comes) and I will replace their trades with trades from new systems.

But recently I’ve checked correlation between in-sample trading and out-of-sample for various metrics. This is shown in attached file.

Two highest correlations are for final account value and bars-in ratio. (Bars-in ratio is just percentage of bars when a system has a trade opened. So 10 markets with 100 bars history would be 1000 bars. If a system has a trade opened in any 10 bars then bars-in ratio would be 1%).

Back to why I decided to trade only 5 best systems (based on in-sample performance):

The top 5 systems' out-of-sample average account value is around 38 times more than initial value (in other words, an average profit is about 3800% since 2018). More interesting is the sum of bars-in ratios: it’s just 26%. That means, that on average I will have invested only about a quarter of working capital. Unused capital will probably go to some ETFs, bonds or something similar. Of course, it’s possible that I will get more signals and I won’t be able to take them all, but I’m not worried and I’ll decide what to do when it actually happens.

This also means there are some changes to my position sizing: each trade is now about 2000 PLN. With 5 systems it means I can take about 10 trades for each system. Right now, I have around 20 signals so there is room for more.

I will slowly exit old systems at my discretion (or when actual exit signal comes) and I will replace their trades with trades from new systems.

Attachments

System 230903_24817_BN reduced 3RG by 1060

System 230904_41122_B reduced ASM by 1310

System 230904_41122_B sold ATS at 0.442

System 230913_22290_B bought 2658 shares of NTC at 0.75

I decided that from now on I will not override my systems (even when buying trash). The whole point is to prove to myself that systems created by data mining can be profitable. We'll see how it ends.

Edit: Also, a funny thing happened today: I wanted to sell IFC (with a normal exit signal) but it was suspended from trading. Bad luck.

System 230904_41122_B reduced ASM by 1310

System 230904_41122_B sold ATS at 0.442

System 230913_22290_B bought 2658 shares of NTC at 0.75

I decided that from now on I will not override my systems (even when buying trash). The whole point is to prove to myself that systems created by data mining can be profitable. We'll see how it ends.

Edit: Also, a funny thing happened today: I wanted to sell IFC (with a normal exit signal) but it was suspended from trading. Bad luck.