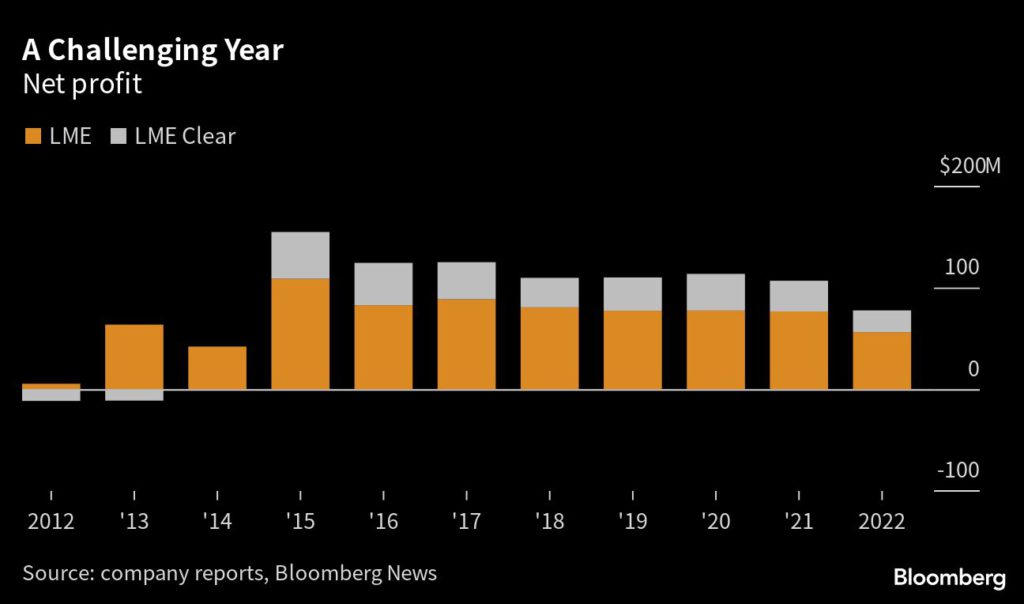

In one of the most shocking events in London trading circles, last month’s massive short squeeze on nickel led the London Metal Exchange to make the controversial call to tear up some $4bn in trades.

The move wiped an an estimated $1.3bn in returns for those holding long nickel positions, and may have helped stem the losses of those who were short, leading some traders to say they may ditch the LME for good.

More than a month later, that may now be playing out.

Funds held 48,878 lots long of nickel as of 4 March, the week before nickel trading was halted, according to Commitment of Traders reports, released by the LME and detail positions held by market participants. One month later, the number of lots long tumbled about 31% to 33,520. Bearish positions in nickel also fell, from 9,932 lots short to 9,197 lots during the same timeframe.

John Mothersole, a director at S&P global market intelligence, told Financial News the CoT reports, “show investors as a trading group [are] backing away.”

AQR Capital Management may be one of them. The investment firm co-founded by Clifford Asness says it had a long position on nickel on 8 March, the day the LME wiped trades already on the books. Asness raged against the LME on Twitter, rebutting the exchange’s stance that cancelling trades was necessary because nickel prices were “no longer reflecting the underlying physical market”.

Jordan Brooks, co-head of macro strategies at AQR, says that while the firm continues to manage its nickel positions on the LME, there will come a time to review.

READUK regulators to probe LME’s nickel fiasco after exchange cancelled $4bn in trades

“Down the road, we will take a step back and evaluate the future of business we do with the LME,” Brooks told Financial News.

When asked what the LME would need to do to restore confidence for market participants like AQR, Brooks said: “The LME would have to demonstrate a commitment to fair and transparent actions going forward.”

An LME spokesperson said, “We fully recognise the impact of these events on a broad spectrum of market participants, and understand that not all participants agreed with the course of action undertaken.

“We are committed to ensuring that the actions of all participants (including the LME itself) are fully reviewed, and appropriate actions taken to both restore confidence and support the long-term health and efficiency of the market.”

Though the LME is one of the few exchanges that trades nickel, there are dozens of exchanges that have experience serving as a marketplace for other metals.

“Ultimately, we live in a competitive economy,” Brooks said. “And I certainly wouldn’t be surprised if other exchanges aren’t going to be looking to increase their footprint materially in base metals. That’s the beauty of free markets.”

Brooks told FN that it is not the suspension that has irked traders but the cancellation of trades.

“Cancelling trades that were made in good faith, by willing counterparties, and at the expense of one party to protect the other party, is completely antithetical to the purpose of exchanges,” said Brooks.

When trading finally resumed a week later on 16 March — which was also plagued with problems — open interest in nickel was thin.

Data from IHS Markit found that open interest in various metals traded on both the LME and the Shanghai Futures Exchange — the other major exchange that trades nickel — have declined, signalling less liquid markets.

Mothersole said lower open interest can be attributed to fewer market participants trading the asset class.

READMetals guru on the ‘apoplectic rage’ of nickel traders over LME debacle

“This matches reports that market participants have retreated, at least temporarily, from trading because of higher initial margins and/or difficulties in obtaining letters of credit for transactions,” he said.

The LME said the drop in open interest across non-ferrous such as nickel, aluminium and copper was due to high volatlity and “geopolitical instability”.

The LME told FN, “Open interest has fallen broadly in line with expectation, and is a trend that is evident across commodity markets – driven by the risk-off sentiment among financial investors.”

It’s still unclear where the long term trends will land. But Mark Thompson, a veteran metals trader and hedge fund manager, says to expect a drop in trading on the LME.

“We’re in the middle of a massive bull market,” Thompson, now an executive at mining development firm Tungsten West, told FN last month. The Ukraine war has led to a supply crunch and energy and commodity prices worldwide have soared. “Volume should be expanding enormously right now, but I don’t think we’re going to see that. We’re going to see volumes shrink.”

The move wiped an an estimated $1.3bn in returns for those holding long nickel positions, and may have helped stem the losses of those who were short, leading some traders to say they may ditch the LME for good.

More than a month later, that may now be playing out.

Funds held 48,878 lots long of nickel as of 4 March, the week before nickel trading was halted, according to Commitment of Traders reports, released by the LME and detail positions held by market participants. One month later, the number of lots long tumbled about 31% to 33,520. Bearish positions in nickel also fell, from 9,932 lots short to 9,197 lots during the same timeframe.

John Mothersole, a director at S&P global market intelligence, told Financial News the CoT reports, “show investors as a trading group [are] backing away.”

AQR Capital Management may be one of them. The investment firm co-founded by Clifford Asness says it had a long position on nickel on 8 March, the day the LME wiped trades already on the books. Asness raged against the LME on Twitter, rebutting the exchange’s stance that cancelling trades was necessary because nickel prices were “no longer reflecting the underlying physical market”.

Jordan Brooks, co-head of macro strategies at AQR, says that while the firm continues to manage its nickel positions on the LME, there will come a time to review.

READUK regulators to probe LME’s nickel fiasco after exchange cancelled $4bn in trades

“Down the road, we will take a step back and evaluate the future of business we do with the LME,” Brooks told Financial News.

When asked what the LME would need to do to restore confidence for market participants like AQR, Brooks said: “The LME would have to demonstrate a commitment to fair and transparent actions going forward.”

An LME spokesperson said, “We fully recognise the impact of these events on a broad spectrum of market participants, and understand that not all participants agreed with the course of action undertaken.

“We are committed to ensuring that the actions of all participants (including the LME itself) are fully reviewed, and appropriate actions taken to both restore confidence and support the long-term health and efficiency of the market.”

Though the LME is one of the few exchanges that trades nickel, there are dozens of exchanges that have experience serving as a marketplace for other metals.

“Ultimately, we live in a competitive economy,” Brooks said. “And I certainly wouldn’t be surprised if other exchanges aren’t going to be looking to increase their footprint materially in base metals. That’s the beauty of free markets.”

Brooks told FN that it is not the suspension that has irked traders but the cancellation of trades.

“Cancelling trades that were made in good faith, by willing counterparties, and at the expense of one party to protect the other party, is completely antithetical to the purpose of exchanges,” said Brooks.

When trading finally resumed a week later on 16 March — which was also plagued with problems — open interest in nickel was thin.

Data from IHS Markit found that open interest in various metals traded on both the LME and the Shanghai Futures Exchange — the other major exchange that trades nickel — have declined, signalling less liquid markets.

Mothersole said lower open interest can be attributed to fewer market participants trading the asset class.

READMetals guru on the ‘apoplectic rage’ of nickel traders over LME debacle

“This matches reports that market participants have retreated, at least temporarily, from trading because of higher initial margins and/or difficulties in obtaining letters of credit for transactions,” he said.

The LME said the drop in open interest across non-ferrous such as nickel, aluminium and copper was due to high volatlity and “geopolitical instability”.

The LME told FN, “Open interest has fallen broadly in line with expectation, and is a trend that is evident across commodity markets – driven by the risk-off sentiment among financial investors.”

It’s still unclear where the long term trends will land. But Mark Thompson, a veteran metals trader and hedge fund manager, says to expect a drop in trading on the LME.

“We’re in the middle of a massive bull market,” Thompson, now an executive at mining development firm Tungsten West, told FN last month. The Ukraine war has led to a supply crunch and energy and commodity prices worldwide have soared. “Volume should be expanding enormously right now, but I don’t think we’re going to see that. We’re going to see volumes shrink.”