Sorry? 1 sec bar signals? And a 250 tick stop loss....??

I'm no expert, but thats insane.

Why not test with much tighter stops....10 ticks, 20 ticks, 30 ticks.... etc.

If you need a 250 tick "buffer" to maintain a positive expectancy system, then you've got one of those inverted risk-to-reward scalping systems that blow up over the long term.

Thats what it sounds like.

Thanks for the feedback. I certainly agree that 250-ticks initial stop (about the average daily range for CL) is a lot.

Average winning trade is 70-ticks (long) to 98-ticks (short) ... this is not a scalping system. All trades are 1 contract, no add-on.

Trade decisions are made on 1-min TF, but trade execution is on 1-sec TF (for better accuracy of backtesting).

As for stops ... I have yet to produce a CL trading system with a meaningful positive expectancy at 10-ticks initial stop. My experience is that getting out on stop is the worse exit strategy ... I prefer using the initial stop as "catastrophic" stop, and actively manage exits.

"Catastrophic" might have different meaning for different people. I use 5 to 10% of the max. allowable drawdown for a system to define that level. For this one, I am using 24k as the max. allowable drawdown (roughly twice the max. historical DD, although this is just a confirmation datapoint, I use MC simulations to decide on the max. allowable drawdown), so 250-ticks is just past that 10% mark (v06 actually uses a 225-ticks initial stop).

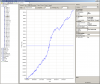

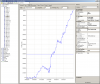

To answer your question directly, below is the performance table using various initial stop size (0 means no-stop). As you can see, reducing the initial stop size essentially reduces the overall win% and P&L, without having much impact on the max. historical drawdown.