(cont'd from above)

Question of Choice

Was there really a choice? Did Speece make these mistakes acting alone or because of "venality of its leaders".

Pettis answers ...

Blaming Nations

Because German capital flows to Spain ensured that Spanish inflation exceeded German inflation, lending rates that may have been "reasonable" in Germany were extremely low in Spain, perhaps even negative in real terms. With German, Spanish, and other banks offering nearly unlimited amounts of extremely cheap credit to all takers in Spain, the fact that some of these borrowers were terribly irresponsible was not a Spanish "choice".

Couldn't Spain have refused to accept the cheap credit, and so would not have suffered from speculative market excesses, poor investment, and the collapse in the savings rate? Not really. Pettis explains ...

"There is no such a decision-maker as 'Spain'. As long as a country has a large number of individuals, households, and business entities, it does not require uniform irresponsibility, or even majority irresponsibility, for the economy to misuse unlimited credit at excessively low interest rates. The experience of Germany after 1871 suggests that it is nearly impossible to prevent a massive capital inflow form destabilizing domestic markets."

As German money poured into Spain, with Spain importing capital equal to 10% of GDP at its peak, the massive capital inflows and declining interest rates ignited asset price bubbles. Pro-Cyclical Feedback Loops

Spain could not stop these pro-cyclical feedback loops of massive proportion because Spain did not have control over its own interest rate policy or currency.

Instead, the ECB had an interest rate policy best described in my opinion as "one size fits Germany".

The bubble-blowing feedback loop fed on itself until it blew up. Who is really to blame for that?

Target2

No discussion of eurozone problems would be complete without a discussion of Target2, an abomination created by the eurozone founders and one of the fundamental flaws of the euro.

Target2 stands for Trans-European Automated Real-time Gross Settlement System.

It is a reflection of capital flight from the "Club-Med" countries in Southern Europe (Greece, Spain, and Italy) to banks in Northern Europe.

Pater Tenebrarum at the Acting Man blog provides this easy to understand example: "Spain imports German goods, but no Spanish goods or capital have been acquired by any private party in Germany in return. The only thing that has been 'acquired' is an IOU issued by the Spanish commercial bank to the Bank of Spain in return for funding the payment."

Also, if people in "Speece" no longer trust their banks, they pull their deposits and park them elsewhere.

Channel for Capital Flight

PIMCO explains Target2 as a Channel for Capital Flight.

Question of Choice

Was there really a choice? Did Speece make these mistakes acting alone or because of "venality of its leaders".

Pettis answers ...

Blaming Nations

Because German capital flows to Spain ensured that Spanish inflation exceeded German inflation, lending rates that may have been "reasonable" in Germany were extremely low in Spain, perhaps even negative in real terms. With German, Spanish, and other banks offering nearly unlimited amounts of extremely cheap credit to all takers in Spain, the fact that some of these borrowers were terribly irresponsible was not a Spanish "choice".

Couldn't Spain have refused to accept the cheap credit, and so would not have suffered from speculative market excesses, poor investment, and the collapse in the savings rate? Not really. Pettis explains ...

"There is no such a decision-maker as 'Spain'. As long as a country has a large number of individuals, households, and business entities, it does not require uniform irresponsibility, or even majority irresponsibility, for the economy to misuse unlimited credit at excessively low interest rates. The experience of Germany after 1871 suggests that it is nearly impossible to prevent a massive capital inflow form destabilizing domestic markets."

As German money poured into Spain, with Spain importing capital equal to 10% of GDP at its peak, the massive capital inflows and declining interest rates ignited asset price bubbles. Pro-Cyclical Feedback Loops

Spain could not stop these pro-cyclical feedback loops of massive proportion because Spain did not have control over its own interest rate policy or currency.

Instead, the ECB had an interest rate policy best described in my opinion as "one size fits Germany".

The bubble-blowing feedback loop fed on itself until it blew up. Who is really to blame for that?

Target2

No discussion of eurozone problems would be complete without a discussion of Target2, an abomination created by the eurozone founders and one of the fundamental flaws of the euro.

Target2 stands for Trans-European Automated Real-time Gross Settlement System.

It is a reflection of capital flight from the "Club-Med" countries in Southern Europe (Greece, Spain, and Italy) to banks in Northern Europe.

Pater Tenebrarum at the Acting Man blog provides this easy to understand example: "Spain imports German goods, but no Spanish goods or capital have been acquired by any private party in Germany in return. The only thing that has been 'acquired' is an IOU issued by the Spanish commercial bank to the Bank of Spain in return for funding the payment."

Also, if people in "Speece" no longer trust their banks, they pull their deposits and park them elsewhere.

Channel for Capital Flight

PIMCO explains Target2 as a Channel for Capital Flight.

The EU’s loans to Greece, Ireland and Portugal are just the tip of the iceberg of a fledgling transfer system that is creeping into the eurozone via the back door. A far bigger and implicit subsidy is growing beneath the surface in the form of TARGET2.

When the European Central Bank (ECB) creates money, as it currently is doing in grand style, it must end up somewhere. The allocation of TARGET2 balances among the seventeen national central banks, which together with the ECB make up the Eurosystem, reflects where the market allocates the money created by the ECB. The fact that the Bundesbank has a large TARGET2 claim (asset) on the Eurosystem, while national central banks in southern Europe and Ireland together have an equally large TARGET2 liability, simply reflects that a lot of the ECB’s newly created money has ended up in Germany. Why? Because of capital flight.

Countries in southern Europe generated persistent current account deficits since joining the euro in 1999, some of them large. A current account deficit means a country spends more in total than it earns. That extra spending is financed by borrowing from abroad. The source for such borrowing comes from a current account surplus country, like Germany. Since the euro eliminated exchange rate risk among its member states, Germany has invested a substantial portion of its savings in Europe’s current account deficit countries. Some of those savings are now returning home. That’s the capital flight.

Enter the ECB. The ECB stepped into the void left by foreign investors pulling their savings out of these current account deficit countries by lending their banks more money. TARGET2 balances thus reflect intra-Eurosystem credits among the national central banks sharing the euro. When large capital flight to Germany occurred before the euro’s introduction, the deutschemark would appreciate against other European currencies. While pegged against the deutschemark, these exchange rates were still flexible. That flexibility disappeared with the euro.

When capital flight occurs today, the Bundesbank effectively ends up with loans to the other national central banks that are reflected in the TARGET2 claims on the Eurosystem. Target2 Imbalances

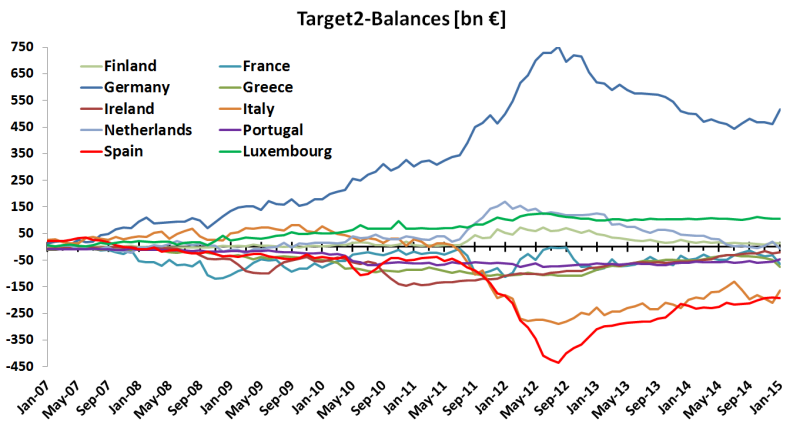

Chart courtesy of Euro Crisis Monitor.

As of January 15, 2015, the Target2 numbers look like this, in billions of euros:

CountryJan-15

Belgium-13.525

Germany 515.266

Estonian.a.

Ireland-19.431

Greece-75.994

Spain-191.917

France-64.700

Italy-164.474

Cyprus-2.543

Luxembourg106.722

Malta-1.546

Netherlands-7.127

Austria-37.375

Portugal-47.504

Slovenian.a.

Slovakian.a.

Finland12.500

Latvia-2.735

Key Target2 Numbers

The ECB treats all of these surpluses and deficits as if they were equal and as if they don't matter. Clearly they are not equal, and they do matter.

Role of Attitudes

It's not entirely true that attitudes played no role in this mess. Germans tend to view things quite differently because of their experience with hyperinflation in the 1920s.

Today, socialists rule France, Greece, Spain and other countries. Greece has a history of defaults.

To completely dismiss such items is wrong. But who bears responsibility? The Germans, the Greeks, the Spaniards? Speece?

The answer is the eurozone founders and the eurozone aggregate members.

Greece lied to get into the eurozone. But every country knew Greece lied. If they didn't, they should have. And if Germany knew Greece lied, who gets the bigger share of the blame?

More fundamentally, the eurozone founders knew full well there were serious productivity differences, work rule differences, pension differences, etc., etc., between countries. The eurozone founders mistakenly assumed that all the countries would get together and solve these issues.

Oops. That is damn near impossible now because rule changes require consent of every eurozone country. The more countries that are added, the more difficult it is to get rule changes.

Currently a mass of rule changes are sorely needed on agricultural issues, work issues, pension issues, and literally dozens of issues. Any country can block reform.

(cont'd below)

When the European Central Bank (ECB) creates money, as it currently is doing in grand style, it must end up somewhere. The allocation of TARGET2 balances among the seventeen national central banks, which together with the ECB make up the Eurosystem, reflects where the market allocates the money created by the ECB. The fact that the Bundesbank has a large TARGET2 claim (asset) on the Eurosystem, while national central banks in southern Europe and Ireland together have an equally large TARGET2 liability, simply reflects that a lot of the ECB’s newly created money has ended up in Germany. Why? Because of capital flight.

Countries in southern Europe generated persistent current account deficits since joining the euro in 1999, some of them large. A current account deficit means a country spends more in total than it earns. That extra spending is financed by borrowing from abroad. The source for such borrowing comes from a current account surplus country, like Germany. Since the euro eliminated exchange rate risk among its member states, Germany has invested a substantial portion of its savings in Europe’s current account deficit countries. Some of those savings are now returning home. That’s the capital flight.

Enter the ECB. The ECB stepped into the void left by foreign investors pulling their savings out of these current account deficit countries by lending their banks more money. TARGET2 balances thus reflect intra-Eurosystem credits among the national central banks sharing the euro. When large capital flight to Germany occurred before the euro’s introduction, the deutschemark would appreciate against other European currencies. While pegged against the deutschemark, these exchange rates were still flexible. That flexibility disappeared with the euro.

When capital flight occurs today, the Bundesbank effectively ends up with loans to the other national central banks that are reflected in the TARGET2 claims on the Eurosystem. Target2 Imbalances

Chart courtesy of Euro Crisis Monitor.

As of January 15, 2015, the Target2 numbers look like this, in billions of euros:

CountryJan-15

Belgium-13.525

Germany 515.266

Estonian.a.

Ireland-19.431

Greece-75.994

Spain-191.917

France-64.700

Italy-164.474

Cyprus-2.543

Luxembourg106.722

Malta-1.546

Netherlands-7.127

Austria-37.375

Portugal-47.504

Slovenian.a.

Slovakian.a.

Finland12.500

Latvia-2.735

Key Target2 Numbers

- Germany has a Target2 surplus of €515 billion.

- Greece has a target2 deficit of €76 billion.

- Spain has a target2 deficit of €192 billion.

- Italy has a target2 deficit of €164 billion.

The ECB treats all of these surpluses and deficits as if they were equal and as if they don't matter. Clearly they are not equal, and they do matter.

Role of Attitudes

It's not entirely true that attitudes played no role in this mess. Germans tend to view things quite differently because of their experience with hyperinflation in the 1920s.

Today, socialists rule France, Greece, Spain and other countries. Greece has a history of defaults.

To completely dismiss such items is wrong. But who bears responsibility? The Germans, the Greeks, the Spaniards? Speece?

The answer is the eurozone founders and the eurozone aggregate members.

Greece lied to get into the eurozone. But every country knew Greece lied. If they didn't, they should have. And if Germany knew Greece lied, who gets the bigger share of the blame?

More fundamentally, the eurozone founders knew full well there were serious productivity differences, work rule differences, pension differences, etc., etc., between countries. The eurozone founders mistakenly assumed that all the countries would get together and solve these issues.

Oops. That is damn near impossible now because rule changes require consent of every eurozone country. The more countries that are added, the more difficult it is to get rule changes.

Currently a mass of rule changes are sorely needed on agricultural issues, work issues, pension issues, and literally dozens of issues. Any country can block reform.

(cont'd below)