I don't think you understand what diversification really means. What you did with your corn and soy trade is not diversification.

Regards

Shelton

Diversification in this context means having trading systems for multiple instruments, which have less than 100% correlation with each other.

Some of those trading systems will have very high correlation (but also see my further comments below). But sometimes they will have quite different positions on, which is what gives you the diversification.

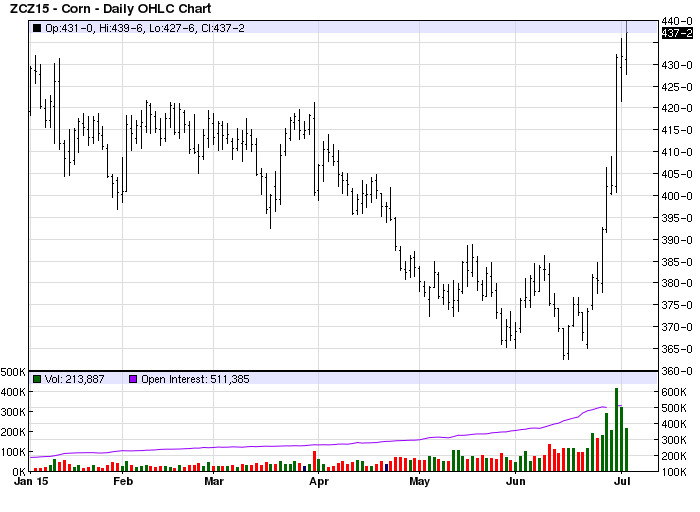

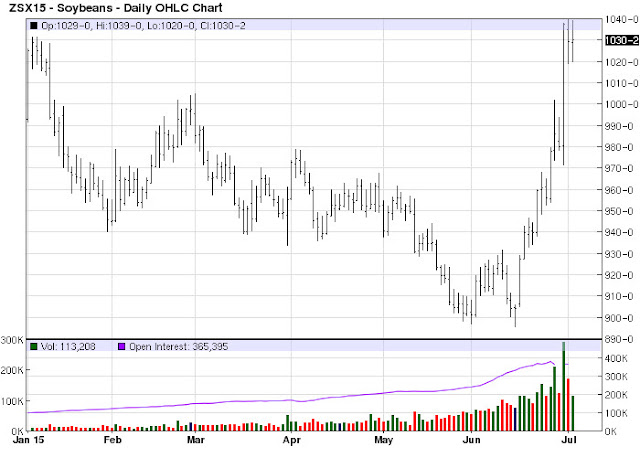

Common knowledge is that grains are highly correlated. A sophisticated system trader like yourself has probably studied the exact degree of correlation and then some.

Don't you feel that having opposing positions within the grain complex would neutralize your exposures and be innefficient use of capital?

This is a very interesting point.

So let's start from the premise that with enough capital I'd want to trade every liquid instrument in the world. Why? Because diversification is the only free lunch. To put it another way I don't know in advance which of my instruments will make money. So I should hedge my bets by holding as many of them as possible.

As long as something has less than 100% correlation with what I'm already trading then with no other constraints I would definitely want to add it, because it's going to improve my risk adjusted return (leaving aside the argument about how stable correlations are).

To reiterate the point from above usually I'll have the same bet on in very similar markets; but sometimes I'll have an opposing bet on. Because I leverage up to account for diversification I should (in the long run) end up earning more with the same amount of risk. So at least in this world having offsetting positions isn't a 'waste' of capital.

Actually if I have a lot of capital, like a few billion dollars, then I

have to trade every liquid instrument. I even have to trade for example both the front, middle and back Eurodollars; even though they are 98% correlated with each other. This is because I can't deploy my capital equal weighted across all the markets that are out there, since in many of them I'd be too large a proportion of the open interest.

Note that the correlations of trading systems are lower than the correlations of the actual instruments themselves. If you read the blog you'll see this is partly because (a) you might not use exactly the same system even on highly correlated markets and (b) modest differences in behaviour can translate to larger differences in positions over time. So the correlation of those eurodollar systems might 'only' be 90%.

Let's go from the other extreme now. Suppose I have a portfolio that only contains corn, because I only have enough capital for that one future. If I got a bit more money and could only trade two futures it would be crazy to trade both corn and soyabeans. I'd be better off putting my money into corn and say treasuries.

As I got more money I'd be better off adding more asset classes. So I'd add maybe Crude, then an equity like S&P500, then maybe Gold, a currency; and then eurodollar and VIX.

Only when you reach this point (which is probably a six figure portfolio) would you start to think about adding a second product to each asset class. And again in ags I'd probably add hogs or cattle next, rather than another grain like soyabean.

Anyway, you get the idea. At some point it becomes logical to trade both corn and soyabeans (and I also have wheat). I've reached that point.

I'd love to hear his explaination for why his "system" went short on one grain and long on the other given the fact they had almost the exact same charts.

I was also curious about this which is why I dug into it and posted the topic originally. Read the blog, which has the explanation in it.

I'd love to hear why you feel the need to use the word 'system' in quotes like that. Is it because you don't believe I really have a system, because you don't think it's a very good one, or because you don't agree with systematic trading?

GAT