A COLOSSAL FAILURE OF COMMON SENSE

JANUARY 27, 2021 NY TIMES BESTSELLING AUTHOR LAWRENCE MCDONALD LEAVE A COMMENT

*Our institutional client flatform includes; financial advisors, family offices, RIAs, CTAs, hedge funds, mutual funds, and pension funds.

Email tatiana@thebeartrapsreport.com to get on our live Bloomberg chat over the terminal, institutional investors only please, it’s a real value add.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Companies Outed by Short Sellers

Enron

Wirecard

Sunbeam

Lehman

Worldcom

Madoff

Cendant

Tyco

*In a world of state-controlled central bank liquidity, message boards, and leverage; who are we actually protecting? How many Bernie Madoffs, how many Bernie Ebbers will be running around the Hamptons this Summer?

The Problem of 2021 – The Fed’s Macro Pru Risk Tools are designed for 2008, not 1999

Several Institutional Clients are talking up a Possible macro-pru Fed Adjustment, Central Bank Action, warning…

Bailout Alert: *CITADEL, POINT72 TO INVEST $2.75 BLN IN MELVIN CAPITAL

Comments from Our Live Institutional Chat on Bloomberg

The bailout of Long Term Capital Mgmt LTCM: $3.6 billion

The bailout of someone short $GME: $2.75 billion

*According to usinflationcalculator.com, that $3.6B bailout in 1998 is equivalent to $5.72B today. The bailout that saved the world was $5B now look at us.. $1 trillion “isn’t enough.”

CIO West Coast: “ I think mkt is really scary when a $13bn hf can be down 40%+ a month into the year and asking for bailouts.”

CIO East Coast: “ I don’t see anything systematic in a few short sellers getting chopped up. The fact the two deepest pockets in equities just rode in before the shxt had even made it to the fan says there isn’t a problem. Classic Fed, wrong macropru toolbox. What did citadel securities do in revenue? $6.7bn? I’ll bet 60% of that drops straight to the bottom line. We have an Option vol seller (Citadel) + buy-side (point 72) deploying a reddit fire hose, comedy”

CIO Hedge Fund NYC: “I remember 1999 well. I think this is now at least as crazy. The GME squeeze is quite a doozy. I think the short-selling community is pretty destroyed. “

What Triggered the Bailout? It’s similar to the SoftBank whale gamma squeeze.

A) Large herd of organized players buys large amounts of upside calls on stocks with the greatest % short interest.

B) Option traders getting lifted in SIZE, have (MUST) to buy stock to hedge all the incoming call buyers.

C) As option buyers buy the stocks GME, BB, BBBY etc, this triggers short squeeze as % of float available is very small. Compared to the 1990s, the options ease of use is 10x more accessible today, cheaper commissions (they are paying, just don’t see it) today as well. Message boards (Reddit), a social element similar to the 1990s. So the options angle triggers more of a gamma squeeze with a larger, more mobilized herd. Next, Elon Musk and VCs pile on the action.

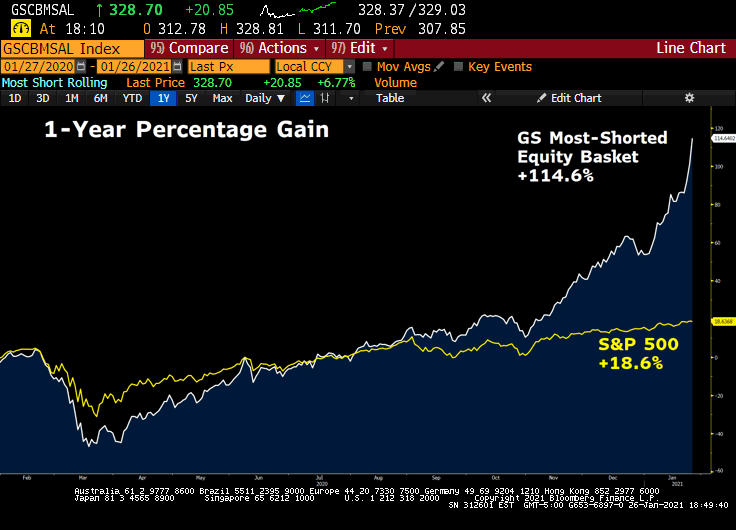

Impact: Nasdaq has witnessed two inter-day bearish reversals of 2.7% and 1.8% this week. VIX touches 200d (27.45) first time since election day.

A Bull-Raid on Short Sellers

Think of the 1990s mob taking out famed short-seller Julien Robertson vs. the 2020 mob trying to attempt the same thing, now think Genghis Kahn vs. Atila the Hun innovation, mobilized, organized leverage.

Think of the 1990s mob taking out famed short-seller Julien Robertson vs. the 2020 mob trying to attempt the same thing, now think Genghis Kahn vs. Atila the Hun innovation, mobilized, organized leverage.

We are Looking at more Macro-pru fix Incentive Fuel for the Fed!!!

Market extremes always force a policy response, oftentimes in Bear markets with March 2020 the shock and awe moment of all time. But what about a colossal bull market perch… covered in froth?

WHAT ARE MACROPRUDENTIAL POLICIES? AND HOW DO THEY DIFFER FROM MICROPRUDENTIAL POLICIES?

With Lehman Brothers in mind, macroprudential policies are financial policies aimed at ensuring the stability of the financial system as a whole to prevent substantial disruptions in credit and other vital financial services necessary for stable economic growth. The stability of the financial system is at greater risk when financial vulnerabilities are high, such as when institutions and investors have high leverage and are overly reliant on uninsured short-term funding, and interconnections are complex and opaque.

For the first time in four years, we are looking at an FOMC without Trump constraints. More importantly, they’re wearing the inequality dunce cap sitting in the corner. After a decade of fueling gross inequality, central bankers are out to prove their innocence as newfound social justice warriors.

The problem, looking over the list of the Fed’s macro-prudential tools – most are bank balance sheet related, that’s not where the problem is. Over the last hundred years, after each financial crisis, there has been a unique metamorphosis, a transformation into another serpent, a far different beast. If the Fed has learned anything, this time the focus must be on stock market leverage, margin requirements, etc. It´s far more 1999 than 2008. If Alan Greenspan could go back in time, what macropru tools should he have used in the dotcom era?

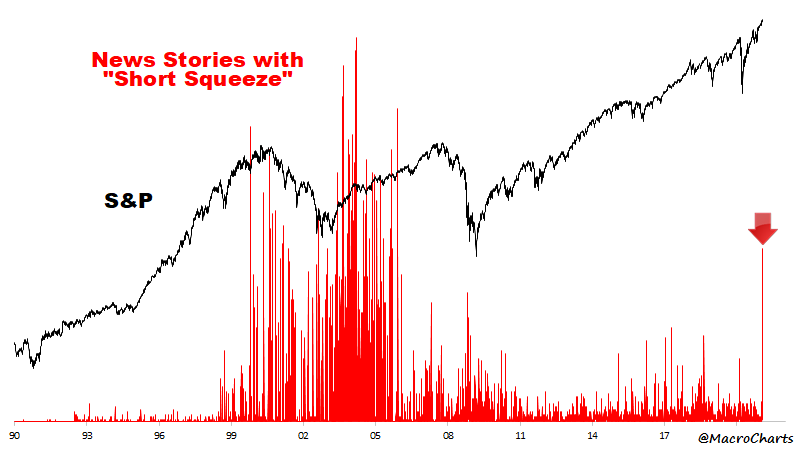

Mobs vs. Shorts

Good one from MacroCharts… In our view, mobs have been taking out shorts for decades, NOW they use tactical nuclear weapons (mob-induced option leverage), vs. more primitive methods in the 1990s.

Good one from MacroCharts… In our view, mobs have been taking out shorts for decades, NOW they use tactical nuclear weapons (mob-induced option leverage), vs. more primitive methods in the 1990s.

How Times Have Changed

The bailout of Long-Term Capital Management LTCM: $3.6 billion*

The bailout of someone short $GME: $2.75 billion

*Fourteen financial institutions recapitalized LTCM with $3.6B: Bankers Trust, Barclays, Chase Manhattan, Credit Agricole, CSFB, Deutsche, Goldman, JPM, Merrill, Morgan Stanley, Paribas, Salomon SB, SocGen, UBS.

JANUARY 27, 2021 NY TIMES BESTSELLING AUTHOR LAWRENCE MCDONALD LEAVE A COMMENT

*Our institutional client flatform includes; financial advisors, family offices, RIAs, CTAs, hedge funds, mutual funds, and pension funds.

Email tatiana@thebeartrapsreport.com to get on our live Bloomberg chat over the terminal, institutional investors only please, it’s a real value add.

Don’t miss our next trade idea. Get on the Bear Traps Report Today, click here

Companies Outed by Short Sellers

Enron

Wirecard

Sunbeam

Lehman

Worldcom

Madoff

Cendant

Tyco

*In a world of state-controlled central bank liquidity, message boards, and leverage; who are we actually protecting? How many Bernie Madoffs, how many Bernie Ebbers will be running around the Hamptons this Summer?

The Problem of 2021 – The Fed’s Macro Pru Risk Tools are designed for 2008, not 1999

Several Institutional Clients are talking up a Possible macro-pru Fed Adjustment, Central Bank Action, warning…

Bailout Alert: *CITADEL, POINT72 TO INVEST $2.75 BLN IN MELVIN CAPITAL

Comments from Our Live Institutional Chat on Bloomberg

The bailout of Long Term Capital Mgmt LTCM: $3.6 billion

The bailout of someone short $GME: $2.75 billion

*According to usinflationcalculator.com, that $3.6B bailout in 1998 is equivalent to $5.72B today. The bailout that saved the world was $5B now look at us.. $1 trillion “isn’t enough.”

CIO West Coast: “ I think mkt is really scary when a $13bn hf can be down 40%+ a month into the year and asking for bailouts.”

CIO East Coast: “ I don’t see anything systematic in a few short sellers getting chopped up. The fact the two deepest pockets in equities just rode in before the shxt had even made it to the fan says there isn’t a problem. Classic Fed, wrong macropru toolbox. What did citadel securities do in revenue? $6.7bn? I’ll bet 60% of that drops straight to the bottom line. We have an Option vol seller (Citadel) + buy-side (point 72) deploying a reddit fire hose, comedy”

CIO Hedge Fund NYC: “I remember 1999 well. I think this is now at least as crazy. The GME squeeze is quite a doozy. I think the short-selling community is pretty destroyed. “

What Triggered the Bailout? It’s similar to the SoftBank whale gamma squeeze.

A) Large herd of organized players buys large amounts of upside calls on stocks with the greatest % short interest.

B) Option traders getting lifted in SIZE, have (MUST) to buy stock to hedge all the incoming call buyers.

C) As option buyers buy the stocks GME, BB, BBBY etc, this triggers short squeeze as % of float available is very small. Compared to the 1990s, the options ease of use is 10x more accessible today, cheaper commissions (they are paying, just don’t see it) today as well. Message boards (Reddit), a social element similar to the 1990s. So the options angle triggers more of a gamma squeeze with a larger, more mobilized herd. Next, Elon Musk and VCs pile on the action.

Impact: Nasdaq has witnessed two inter-day bearish reversals of 2.7% and 1.8% this week. VIX touches 200d (27.45) first time since election day.

A Bull-Raid on Short Sellers

We are Looking at more Macro-pru fix Incentive Fuel for the Fed!!!

Market extremes always force a policy response, oftentimes in Bear markets with March 2020 the shock and awe moment of all time. But what about a colossal bull market perch… covered in froth?

WHAT ARE MACROPRUDENTIAL POLICIES? AND HOW DO THEY DIFFER FROM MICROPRUDENTIAL POLICIES?

With Lehman Brothers in mind, macroprudential policies are financial policies aimed at ensuring the stability of the financial system as a whole to prevent substantial disruptions in credit and other vital financial services necessary for stable economic growth. The stability of the financial system is at greater risk when financial vulnerabilities are high, such as when institutions and investors have high leverage and are overly reliant on uninsured short-term funding, and interconnections are complex and opaque.

For the first time in four years, we are looking at an FOMC without Trump constraints. More importantly, they’re wearing the inequality dunce cap sitting in the corner. After a decade of fueling gross inequality, central bankers are out to prove their innocence as newfound social justice warriors.

The problem, looking over the list of the Fed’s macro-prudential tools – most are bank balance sheet related, that’s not where the problem is. Over the last hundred years, after each financial crisis, there has been a unique metamorphosis, a transformation into another serpent, a far different beast. If the Fed has learned anything, this time the focus must be on stock market leverage, margin requirements, etc. It´s far more 1999 than 2008. If Alan Greenspan could go back in time, what macropru tools should he have used in the dotcom era?

Mobs vs. Shorts

How Times Have Changed

The bailout of Long-Term Capital Management LTCM: $3.6 billion*

The bailout of someone short $GME: $2.75 billion

*Fourteen financial institutions recapitalized LTCM with $3.6B: Bankers Trust, Barclays, Chase Manhattan, Credit Agricole, CSFB, Deutsche, Goldman, JPM, Merrill, Morgan Stanley, Paribas, Salomon SB, SocGen, UBS.