Didn't Global Alpha lose another couple of bil just the other day? I know, I know, it's only 1% of their portfolio, GS is the "best" blah, blah, blah.... but I say if these guys beat estimates there's some creative accounting going on. Not going long or short into earnings, however. Maybe some way OTM puts just for laughs.

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

08-11-2007: Time to buy Goldman?

- Thread starter polpolik

- Start date

Thanks for the heads up, earnings is Sept 20 before market opens and of course everybody is waiting for Bernanke on Sept 18, 2:15 EST. Those risk adversed should hedge appropriatedly or exit early. This is purely trading on technicals which hopefully will reflect fundamentals or expectation of such. Interestingly, BSC, GS up. LEH, MER, MS down currently. http://biz.yahoo.com/rb/070914/merrilllynch_credit.html?.v=3Quote from hbiawos:

Not going long or short into earnings, however. Maybe some way OTM puts just for laughs.

Although this trade was initiated on technicals (buying pressure, volume), there is usually a fundamental reason for the buying and this is provided by the recent view (see below) that the financials are over-shorted, under-owned and approaching good value. I don't believe sound financial companies such as GS need to beat Q3 earnings in order for the stock price to go up from here.Quote from hbiawos:

GS is the "best" blah, blah, blah.... but I say if these guys beat estimates there's some creative accounting going on.

Financials: Very Contrarian, Decent Value, But Risks Are High

September 05, 2007

By Ronan Carr, Teun Draaisma

Broadening our bets, reducing our Financials overweight. We are buyers of equities and see 13% upside to our 12-month index target. We have been underweight Financials all year until mid-August, when we started buying equities and went overweight Financials. Here we review the positives and negatives for Financials. We conclude that Financials are heavily oversold and underowned, attractively valued, and that central bank rate cuts would act as a positive trigger. Offsetting that, earnings downgrades are still to come, short-term money markets are still in turmoil, and the fundamental outlook is clouded, with debt risk appetite unlikely to return to previous levels. Thus, we think financials are due a potentially powerful bounce from extremely oversold levels, but the fundamental uncertainties may limit the upside on a 12-month view.

We broaden our exposure to stocks that will benefit from the increased risk appetite we expect. We remain overweight Financials but lower it from +3 to +1 percentage points, and we put the money in Alstom (â¬132.67). Today our four biggest overweights are Healthcare, Tech, Telcos, Financials, in that order, and our biggest underweights are Consumer-related sectors.

The contrarian's dream. The mantra of the market is to avoid Financials until more clarity emerges on the impact of the financial crisis, and at least until the investment banks report Q3 earnings in mid to late September. Investor sentiment on the banks is bombed out. In the Russell survey, Banks are 3.3 standard deviations underowned - unprecedented for any sector. In the US, financials are the market's favourite short. Short interest on the US Financials SPDR in mid-August exceeded (165%) the number of shares outstanding (this is possible as market makers are not required to source borrows, and multiple lending of shares is possible)! The exception in terms of sentiment is company management among financial stocks - press reports suggest insider buying has picked up notably in recent weeks.

Central bank action is a bullish trigger. The key bullish trigger now is changing central bank policy. The Fed seems likely to cut rates on September 18, while the ECB may well postpone further tightening. Historically the first rate cut from the Fed has been very bullish for financials: On average Banks outperform by 3% over the subsequent six months. A peak in the tightening cycle has also been associated with a bottom for banks share prices.

Can we believe the earnings? The great uncertainty is whether the denominator in current multiples is reliable. Arguably, much is in the price. A fair P/BV calculation (assuming 2% growth and 8.5% discount rate) suggests the sector is pricing in the long-run average ROE already. That implies a fall of 2.9% points in ROE from here. Given that credit quality in Europe remains high and we do not expect an imminent recession, that suggests we are approaching good value here.

Not a major banking crisis. The Fed's cut in the discount rate two weeks ago has not resolved the crisis in short-term funding markets, as we had expected. Interbank and commercial paper markets are still in turmoil. This adds to the already high risk of ratings downgrades or forced liquidations of structured products, leading to further investment losses and writedowns. And earnings estimates will inevitably be cut to reflect these and other trading losses. Taking (or having to keep) investments and lending commitments back on balance sheets would also reduce capacity for growth. In the near term, that is a key risk factor given revisions for European financials are high and have not yet deteriorated, much less turned negative. On the other hand, the current financial turmoil can be absorbed by the banking system as indicated recently by our US economists and banks analysts. According to Morgan Stanley banking analyst Betsy Graseck's analysis (see âBank Capital: Sufficient Capacity to Absorb Commitmentsâ), even under a worst-case scenario the US banking system has the ability to pull back onto balance sheet all outstanding supported ABCP, LBO commitments, and other unfunded commitments and remain âwell capitalizedâ under regulatory standards. So there does not appear to be any significant risk of a major banking crisis that could help drive the economy into recession.

GS def. going to 250 soon

I just posted this on another thread. Sticking to my guns on all this.

09-15-07 04:42 PM

"Indeed, Hecht expects third-quarter results from the top investment banks to be a "stabilizing" event and advised clients to invest in the stocks ahead of the reports."

Is that so. Well no long positions for me on these guys ahead of earnings...not until they've either:

1. Moved above their respective 200-day emas on decisive volume

2. Had an independent auditor crawl up their respective asses to decipher these "esoteric" holdings (liabilities) to the satisfaction of insitutional (volume) investors.

Look at their charts. All of them. They've *all* been under heavy distribution for months. These guys are hiding something, I don't care what anyone says.

GS was my favorite short for a long time. I don't buy the recent limp-wristed rally in that stock. If and when it gets to its 200-day and *if* it fails at that line of resistence following earnings, I'm ALL IN as a short. I will short that motherfker right into the ground and I will be ecstatic the whole ride down.

If, however, it does cross and close above the 200, I suppose I'll be a reluctant long since everyone (volume) seems to like that damn stock so much.

Something about shorting GS. It's a beautiful thing."

I know it was posted intially as a T/A observaton, and it was a good observation. Still can't quite commit capital to the long side on these guys just yet.

09-15-07 04:42 PM

"Indeed, Hecht expects third-quarter results from the top investment banks to be a "stabilizing" event and advised clients to invest in the stocks ahead of the reports."

Is that so. Well no long positions for me on these guys ahead of earnings...not until they've either:

1. Moved above their respective 200-day emas on decisive volume

2. Had an independent auditor crawl up their respective asses to decipher these "esoteric" holdings (liabilities) to the satisfaction of insitutional (volume) investors.

Look at their charts. All of them. They've *all* been under heavy distribution for months. These guys are hiding something, I don't care what anyone says.

GS was my favorite short for a long time. I don't buy the recent limp-wristed rally in that stock. If and when it gets to its 200-day and *if* it fails at that line of resistence following earnings, I'm ALL IN as a short. I will short that motherfker right into the ground and I will be ecstatic the whole ride down.

If, however, it does cross and close above the 200, I suppose I'll be a reluctant long since everyone (volume) seems to like that damn stock so much.

Something about shorting GS. It's a beautiful thing."

I know it was posted intially as a T/A observaton, and it was a good observation. Still can't quite commit capital to the long side on these guys just yet.

Quote from tmarket:

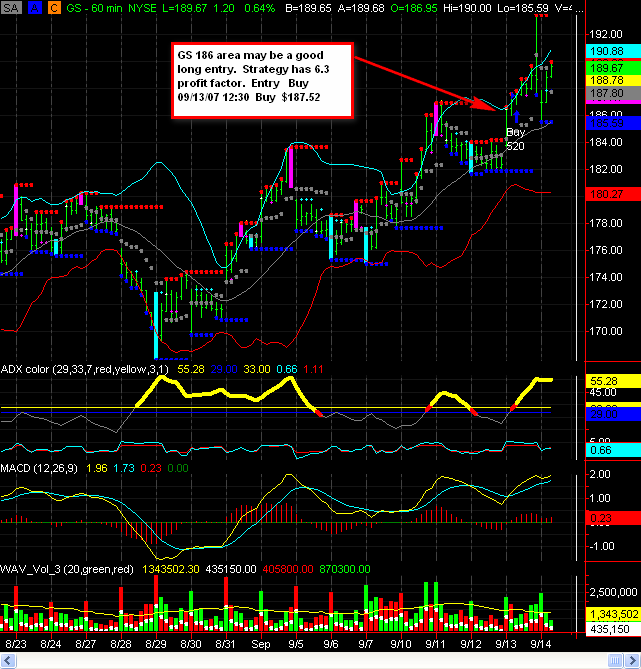

You may have been a little early and I may be a little late, but here goes. GS $186 area may be a good long entry. Strategy has 6.3 profit factor. Entry Buy 09/13/07 12:30 Buy $187.52

(own a few hundred shares from $186 from this AM, 09/14/07 sell off).

BTW tmarket: beautiful chart. Love that chart.

GS is part of the New World Order and for the past forty years the NWO has been gaining power at an increasing rate. Although I am opposed to the NWO that doesn't mean you can't profit off it.

Quote from stock_trad3r:

GS is part of the New World Order and for the past forty years the NWO has been gaining power at an increasing rate. Although I am opposed to the NWO that doesn't mean you can't profit off it.

Say what?? New World Order? Would that be the Woodrow Wilson New World Order? The Bush/Scowcroft New World Order?

The "Novus Ordo Mundi" overthrow-the-government NWO?

Pick yer NWO and explain yourself.

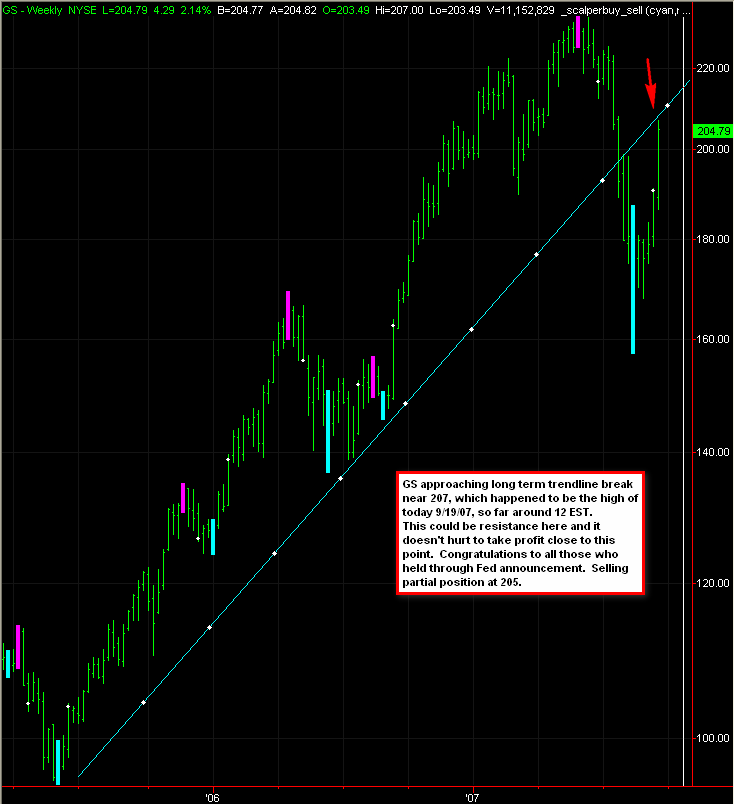

GS approaching it's long term broken trendline near $207, which happened to be the high of today 9/19/07, so far around 12 EST.

This could be resistance here and it doesn't hurt to take profit close to this point. Congratulations to all those who held through Fed announcement. Selling partial position at 205 with entry around 187. This is especially true to those who are risk adverse to holding through earnings, reporting by GS tomorrow morning 9/20/07. Good luck everybody.

This could be resistance here and it doesn't hurt to take profit close to this point. Congratulations to all those who held through Fed announcement. Selling partial position at 205 with entry around 187. This is especially true to those who are risk adverse to holding through earnings, reporting by GS tomorrow morning 9/20/07. Good luck everybody.