You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

Do my numbers make sense?

- Thread starter Adim

- Start date

4) results since April 2 are:

average duration of a trade: 13.45 days

average winning trade: 3.3%

average losing trade: -0.53%

% winning trades: 93% (?!?!?!)

Sharpe Ratio seems to be something stupid like 16+.

This is very good and ok in the short-term, but I'm going to be very impressed if you can do even half that good in the long-term. All of my trading is automated, I have 15+ profitable strategies, everything is tested over 15-25 years, and I don't have anything that comes close to your results in the original post after enough trades and time. Half of that (e.g. 6->3 avg win/loss, 93%->46% win rate), would be more reasonable, but even a 16->8 sharpe sounds too high for a single strategy that holds for that long. You'd want multiple uncorrelated strategies, long and short, and shorter holds for something like that.

But hey if those results are live and you think you can keep it up, good for you, and you'll be a billionaire real quick.

Good morning

I would be very grateful to anyone of you who could help me evaluate my results below.

background: I am a veteran manual trader (28 years) -- but i am new to automated trading. I have spent last couple years trying to automate what I do, the last 7 months doing nothing else (all my trading in last 7 months has been through my programmed subroutines). I am producing promising results, but I don't know how to judge these results against industry standards. we all know what constitutes good trading results in bonds or stocks, but what constitutes good results in auto?

are my results good?

are they... too good? (maybe i need to look for an error?)

outline of project:

1) i trade only S+P 500- stocks. at the moment long only, though i hope to add a short element in the future.

2) at this point I initiate trade manually and the subroutines work the position and exit automatically on signal. it is perfectly possible to program the initiation so that it becomes 100% automated (runs itself) but doing this will require a lot of work from me (i am a beginner coder), so I would like to know whether I am not completely offbase here.

3) trade initiation is based on conditions which have been backtested on the 2010-2019 period.

4) results since April 2 are:

number trades: 240 (average of 32 trades per month)

average duration of a trade: 13.45 days

average number of open positions: 33

average return: 2.6%

average winning trade: 3.3%

average losing trade: -0.53%

% winning trades: 93% (?!?!?!)

portfolio return since April 2: 39.54% (! SPY 27.64%)

turnover: ~130% PER MONTH

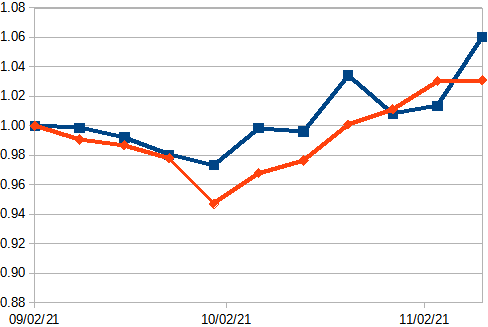

and now the killer: this is how my method worked during the September correction:

program SPY

09/02/21 1.0000 1.0000

09/09/21 0.9986 0.9907

09/16/21 0.9920 0.9867

09/23/21 0.9802 0.9779

09/30/21 0.9733 0.9469

10/07/21 0.9984 0.9679

10/14/21 0.9961 0.9764

10/21/21 1.0340 1.0009

10/28/21 1.0080 1.0113

11/04/21 1.0136 1.0303

11/11/21 1.0604 1.0311

and the chart (blue is method, orange is SPY):

By 9/30 SPY was down -5.3% and i was down -2.63%. Sharpe Ratio seems to be something stupid like 16+.

where am i going wrong?

Just noticed 240 trades, I trade as well S&P500 stocks, but 240 trades I would never trade such small sample size. I back test last 25-50 years of data on 500 dividend/optionable stocks, 50 optionable stocks, and approx 100 low cost stocks which have just started, under 5 bucks. By time I have done back tests of one signal, I will have well over 162,000 sample size, approx 70% of it are longs.

What something does in one small correction, you really have to tone down happiness. Systems I have designed that looked great one year, sometimes horrible next 10 years. As far as automation returns, I have had largest of 16 systems on automation and have cut 6 back in scalping cause Indexes too high in value, been 9 years doing automation.

Here is the thing, whether very long term stock, commodities & options through scalping, if there was a 75 of me, I can trade manually better than automation, but I can't trade 24 hours a day or watch several hundred stocks and commodities, so automation is set parameters with variances and will always make less compared to manually, but where it is awesome, it will select highest graded signals and make 3-20 times more than I could manually trading in a year.

Am very much like you where losing percentages stay low, when one stays in most fields of endeavor, you become good.

My 2 cents: I spend my days backesting my algos. I don't do any manual trading.

If you want to know if your algorithm is ready to be used on a live account fit it to trade against the trend. It is really easy to get a very high winning percentage of trades if you know the trend in advance. That's the most common mistake when we develop algorithms: overfitting.

Another one is assuming that we will have perfect executions. When we trade live there are many factors that we can't include in a backtest. Our connection to the broker, funds, infrastructure, withdrawals and risk management will never perform as well as they do in a simulation. Your performance on a real account will decrease a 50% at least.

Using 20 years of data is another mistake. You can make any algorithm to work if you run it long enough. The more data you add to it the more chances you will get to see winning results. You need to backtest and forward test your algo. If it doesn't work with 6 months of data then it has to be tuned.

Another mistake is to not to breakdown results per year, month, week and days. You need to see how is your algo performing on different timeframes. Getting a 93% in your result might mean a couple of stunning trades over the data that could make up for a long lasting chain of loses. It might be hiding the real performance of the algo just because it did extremely well in certain moments.

If you have 20 years of data try to break it down in random timeframes, then feed those chunks into your algo.

If after doing a fine tuning you still get a 93% of winning trades do not even post your results. Hide in a cave a laugh at everyone.

If you want to know if your algorithm is ready to be used on a live account fit it to trade against the trend. It is really easy to get a very high winning percentage of trades if you know the trend in advance. That's the most common mistake when we develop algorithms: overfitting.

Another one is assuming that we will have perfect executions. When we trade live there are many factors that we can't include in a backtest. Our connection to the broker, funds, infrastructure, withdrawals and risk management will never perform as well as they do in a simulation. Your performance on a real account will decrease a 50% at least.

Using 20 years of data is another mistake. You can make any algorithm to work if you run it long enough. The more data you add to it the more chances you will get to see winning results. You need to backtest and forward test your algo. If it doesn't work with 6 months of data then it has to be tuned.

Another mistake is to not to breakdown results per year, month, week and days. You need to see how is your algo performing on different timeframes. Getting a 93% in your result might mean a couple of stunning trades over the data that could make up for a long lasting chain of loses. It might be hiding the real performance of the algo just because it did extremely well in certain moments.

If you have 20 years of data try to break it down in random timeframes, then feed those chunks into your algo.

If after doing a fine tuning you still get a 93% of winning trades do not even post your results. Hide in a cave a laugh at everyone.

Thing is, most people here have 20-30% returns as target because the big fund managers average about that.

Thank you, Mr Muppet. Thats one thing I wanted to know. If 20-30% is industry expectation then my current results, in the middle of a raging bull, are not necessarily some weird anomaly. I am a little less scared now.

It also makes me wonder: if 20-30% is a quant industry standard then what on earth are all those discretionary manual fund managers doing wasting everybody's time and opportunity? I have tried to bring this up with several (successful) manual traders and they just shut down. They dont want to talk about it. Several flat out told me they dont believe in computer trading. You know: John O'Connor defeats Model T-800 every time they see the film, we are more than mere machines, blah blah (feel the force!). Besides, how do you strut your cojones when your trading is done by your Atari machine, not you, yes?

Thank you for your other comments. Ill post them on the wall above my desk.

Last edited:

That's a lot of positions. How many trades per day or week. Are trading costs a factor?

yes, costs are a factor. if i could do this with bigger account, returns would improve for this reason alone, if nothing else.

its hard for me to answer "how many trades" because what happens is that I open a position manually and leave the computer to trade around it. Average position remains in the works ("Spinning"?) for 13.45 days. during that time there will be hundreds of trades. since the computer is trading all ~30 positions throughout the day, there are lots and lots and lots of transactions

yes, costs are a factor. if i could do this with bigger account, returns would improve for this reason alone, if nothing else.

its hard for me to answer "how many trades" because what happens is that I open a position manually and leave the computer to trade around it. Average position remains in the works ("Spinning"?) for 13.45 days. during that time there will be hundreds of trades. since the computer is trading all ~30 positions throughout the day, there are lots and lots and lots of transactions

There are several types of edge.Thank you, Mr Muppet. Thats one thing I wanted to know. If 20-30% is industry expectation then my current results, in the middle of a raging bull, are not necessarily some weird anomaly. I am a little less scared now.

It also makes me wonder: if 20-30% is a quant industry standard then what on earth are all those discretionary manual fund managers doing wasting everybody's time and opportunity? I have tried to bring this up with several (successful) manual traders and they just shut down. They dont want to talk about it. Several flat out told me they dont believe in computer trading. You know: John O'Connor defeats Model T-800 every time they see the film, we are more than mere machines, blah blah (feel the force!). Besides, how do you strut your cojones when your trading is done by your Atari machine, not you, yes?

Thank you for your other comments. Ill post them on the wall above my desk.

Manual fund managers usually hold weeks and months but they have better research than anybody else...They are smarter and that's how they compete. The best (Paul Tudor Jones et al. ) average double digit returns.

Proprietary trading firms usually operate in high turnover, tiny margin, low latency scenarios where tech is king. They are faster and that's how they compete. They average way higher returns than fund managers and they are very consistent. But there is a limit to how much money you can throw at these strategies so they kinda need these %returns

Retail is somewhere in the middle. Retail doesn't have the research power nor the tech to compete in investing or high frequency trading. But retail is nowhere near capital constraints and has the most opportunities. So they do have the highest annualized returns (the profitable ones of course)